Bank of America 2008 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

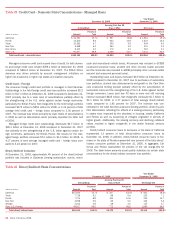

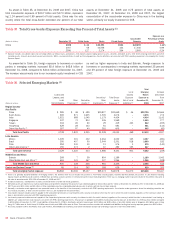

Industry Concentrations

Table 30 presents commercial committed and commercial utilized credit

exposure by industry and the total net credit default protection purchased

to cover the funded and the unfunded portion of certain credit exposure.

Our commercial credit exposure is diversified across a broad range of

industries.

Industry limits are used internally to manage industry concentrations

and are based on committed exposure and capital usage that are allo-

cated on an industry-by-industry basis. A risk management framework is

in place to set and approve industry limits, as well as to provide ongoing

monitoring. The CRC oversees industry limits governance.

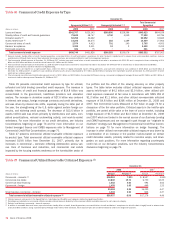

Total commercial committed credit exposure increased by $18.3 billion,

or two percent, at December 31, 2008 compared to 2007 largely driven by

diversified financials partially offset by a decline in commercial real estate.

Total commercial utilized credit exposure increased by $46.8 billion, or 10

percent, at December 31, 2008 compared to 2007. The overall commercial

credit utilization rate increased year over year, increasing from 57 percent to

62 percent due to increases in diversified financials, government and public

education, and healthcare and equipment services.

Real estate remains our largest industry concentration, accounting for

13 percent of total commercial committed exposure, of which 15 percent

is homebuilder exposure. A decrease of $7.9 billion, or seven percent,

was driven primarily by a decline in CMBS assets held-for-sale as a result

of sales and distributions, completed securitizations and writedowns.

Diversified financials grew by $17.2 billion, or 20 percent reflecting

increases in capital markets exposure and consumer finance commit-

ments. Part of the increase was driven by a $3.7 billion fully committed

secured credit facility as well as a $4.0 billion FDIC guaranteed facility,

both of which were with Merrill Lynch. These facilities were terminated

following the completion of the acquisition. The increase in consumer

finance commitments was driven primarily by liquidity support associated

with the financing of credit card and auto finance related assets within

the Corporation’s multi-seller unconsolidated asset backed commercial

paper conduits.

Healthcare equipment and services increased $5.8 billion or 14 per-

cent due to loan growth primarily to not-for-profit healthcare providers.

This was driven primarily by increased demand for liquidity and credit

instruments to support variable rate demand notes (VRDNs) caused by

dislocations in the ARS markets. Consumer services increased $5.3 bil-

lion, or 14 percent driven primarily by growth in the education (private

colleges and universities) sector also resulting from the ARS dislocation.

Food, beverage and tobacco increased $2.8 billion, or 11 percent due to

growth in food products and a large underwritten transaction. Banks

decreased by $8.8 billion or 25 percent, reflecting the termination of a

$5.0 billion commitment to Countrywide.

Government and public education utilizations increased $7.6 billion

due to new refinancings of ARS into letter-of-credit backed VRDNs and the

restructuring of monoline insured VRDNs into uninsured VRDNs. Total

committed exposure increased by $1.2 billion, as the increases in the

utilized balance were partially offset by a reduction in certain unutilized

credit lines.

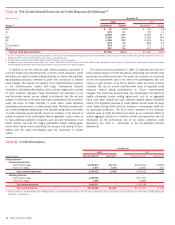

Monoline exposure is reported in the insurance industry and managed

under insurance portfolio industry limits. Direct loan exposure to mono-

lines consisted of revolvers in the amount of $126 million at

December 31, 2008 and $203 million at December 31, 2007.

Mark-to-market counterparty derivative credit exposure was $2.6 billion at

December 31, 2008 compared to $420 million at December 31, 2007.

The increase in the mark-to-market exposure was due to credit deterio-

ration related to underlying counterparties and spread widening in both

wrapped CDO and structured finance related exposures. At December 31,

2008, the counterparty credit valuation adjustment related to monoline

derivative exposure was $1.0 billion, which reduced our net

mark-to-market exposure to $1.6 billion. We do not hold collateral against

these derivative exposures. During the first quarter of 2009, one mono-

line counterparty restructured its business and had its credit rating down-

graded. We are currently evaluating the impact this restructuring and

downgrade will have on Merrill Lynch as well as our related counterparty

credit valuation adjustment and the combined company’s 2009 financial

results.

We have indirect exposure to monolines primarily in the form of guar-

antees supporting our loans, investment portfolios, securitizations, credit

enhanced securities as part of our public finance business and other

selected products. Such indirect exposure exists when we purchase

credit protection from monolines to hedge all or a portion of the credit

risk on certain credit exposures including loans and CDOs. We underwrite

our public finance exposure by evaluating the underlying securities. In the

case of default we first look to the underlying securities and then to

recovery on the purchased insurance. See page 41 for discussion on our

CDO exposure and related credit protection.

We also have indirect exposure as we invest in securities where the

issuers have purchased wraps (i.e., insurance). For example, municipal-

ities and corporations purchase protection in order to enhance their pric-

ing power which has the effect of reducing their cost of borrowings. If the

rating agencies downgrade the monolines, the credit rating of the bond

may fall and may have an adverse impact on the market value of the

security.

We have further monoline related exposure in our public finance busi-

ness where we are the lead manager or remarketing agent for trans-

actions that are wrapped including ARS (healthcare providers and

consumer services), tender option municipal bonds (TOBs), and VRDNs.

Continuing concerns about monoline downgrades or insolvency have

caused disruptions in each of these markets as investor concerns have

impacted overall market liquidity and bond prices. For more information

on ARS, see Recent Events beginning on page 22. We no longer serve as

the lead manager on municipal or student loan ARS where a high

percentage of the programs are wrapped by either monolines or other

financial guarantors. We are the remarketing agent on TOBs and VRDN

transactions and also provide commitments on approximately $13.6 bil-

lion of VRDNs, which increased approximately $2.2 billion during the year,

driven by the conversion by clients of ARS to VRDN structures, including

those issued by municipalities and other organizations. These commit-

ments obligate us to purchase the VRDNs in the event that they can not

be remarketed or otherwise provide funding to the issuer, and are primar-

ily held and reported in government and education related industry portfo-

lios and managed under respective industry limits.

In addition, at December 31, 2008, we also held approximately $1.3

billion in ARS, $1.5 billion in VRDNs and $3.0 billion in TOBs acquired in

connection with these activities which are included in trading account

assets. During 2008, we recorded losses of $1.1 billion on the ARS,

primarily related to student loan-backed securities, including our commit-

ment to repurchase ARS from certain clients as part of a settlement

agreement with regulatory agencies. We did not record any losses on the

VRDNs and only minimal losses on the TOBs during the year. We continue

to have liquidity exposure to these markets and instruments. As market

conditions continue to evolve, these conditions may impact our results.

For additional information on our liquidity exposure to TOBs, see the

Municipal Bond Trusts discussion within the Off- and On-Balance Sheet

Arrangements discussion beginning on page 49 and Note 9 – Variable

Interest Entities to the Consolidated Financial Statements.

76

Bank of America 2008