Bank of America 2008 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

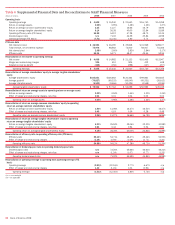

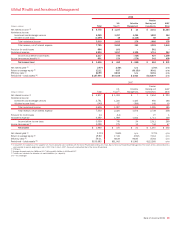

Production income increased $1.4 billion in 2008 compared to 2007.

This increase was driven by the Countrywide acquisition which resulted in

higher volumes, and an improvement in margins.

Net servicing income increased $1.7 billion in 2008 compared to

2007 due primarily to increases in the value of the MSR economic hedge

instruments of $8.6 billion partially offset by changes in the fair value of

MSRs of $6.7 billion. Generally, when mortgage interest rates decline, as

occurred during the second half of 2008, there is an increase in the value

of instruments used to economically hedge MSRs and a corresponding

decrease in the value of MSRs. The decrease in the value of MSRs during

the second half of 2008 was tempered by the expectation that weakness

in the housing market would decrease the impact of market interest rates

on expected future prepayments. For further discussion on MSRs and the

related hedge instruments, see Mortgage Banking Risk Management on

page 92.

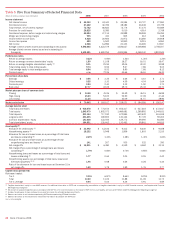

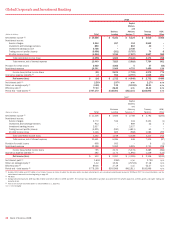

The following table presents select key indicators for MHEIS.

Mortgage, Home Equity and Insurance Services Key Statistics

(Dollars in millions, except as noted) 2008 2007

Loan production:

First mortgage

$128,945

$93,304

Home equity

31,998

69,226

Period end

Mortgage servicing portfolio (in billions)

(1)

2,057

517

Mortgage loans serviced for investors (in

billions)

1,654

259

Mortgage servicing rights:

Balance

12,733

3,053

Capitalized mortgage servicing rights (%

of loans serviced)

77bps

118bps

(1) Servicing of residential mortgage loans, home equity lines of credit, home equity loans and discontinued

real estate mortgage loans.

First mortgage and home equity production were $128.9 billion and

$32.0 billion in 2008 compared to $93.3 billion and $69.2 billion in

2007. The increase of $35.6 billion in first mortgage production was due

to the acquisition of Countrywide partially offset by decreased activity in

the mortgage market. The decrease of $37.2 billion in home equity pro-

duction was primarily due to more stringent underwriting guidelines for

home equity lines of credit and loans, and lower consumer demand.

The servicing portfolio at December 31, 2008 was $2.1 trillion, $1.5

trillion higher than at December 31, 2007, driven by the acquisition of

Countrywide. Included in this amount was $1.7 trillion of residential first

mortgage, home equity lines of credit and home equity loans serviced for

others.

At December 31, 2008, the consumer MSR balance was $12.7 bil-

lion, which represented 77 bps of the related unpaid principal balance as

compared to $3.1 billion, or 118 bps of the related principal balance at

December 31, 2007. The increase in the consumer MSR balance was

driven by $17.2 billion of MSRs that we acquired from Countrywide which

was partially offset by the impact of mortgage rates falling substantially

during the fourth quarter of 2008. As a result of the decline in rates, the

value of the MSRs decreased driven by a significant increase in expected

prepayments which reduced the expected life of the consumer MSRs.

This resulted in the 41 bps decrease in the capitalized MSRs as a per-

centage of loans serviced. MSR economic hedge results were more than

sufficient to offset this decrease.

Bank of America 2008

37