Bank of America 2008 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

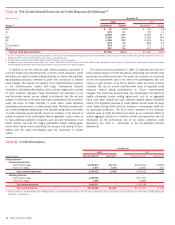

$47 million to $1.1 billion. This is down from $459 million to $1.5 billion

for the hypothetical scenarios for the 12 months ended December 31,

2007. The results of these stress tests point to a decrease in risk taken

during the 12 months ended December 31, 2008.

The acquisition of Merrill Lynch on January 1, 2009 increased our

trading-related activities and exposure. As such, during 2009 we will con-

tinue to refine the VAR calculations and develop a set of stress scenarios

that will be regularly produced across the combined company for pur-

poses of managing our overall risk profile. As of January 1, 2009, we

estimate that the VAR of the combined organizations would have been

$274 million as compared to $138 million for the Corporation. The

combination of VAR measurements is not additive as there are both corre-

lation and diversification effects that impact the results. For stress test-

ing, Merrill Lynch used similar shocks for hypothetical scenarios and as

of January 1, 2009, we estimate that the combined largest loss among

the hypothetical scenarios would have been $774 million. Among the

historical scenarios, comparable shocks were used to reflect the ongoing

credit crisis related to the credit market disruptions, which had previously

exhibited the largest loss among all historical scenarios at

the Corporation. As of January 1, 2009, we estimate that the combined

loss from the historical credit crisis scenario would have been $1.1 bil-

lion. For the Corporation, the loss from the historical credit crisis scenario

would have been $579 million.

Interest Rate Risk Management for Nontrading

Activities

Interest rate risk represents the most significant market risk exposure to

our nontrading exposures. Our overall goal is to manage interest rate risk

so that movements in interest rates do not adversely affect core net

interest income – managed basis. Interest rate risk is measured as the

potential volatility in our core net interest income – managed basis

caused by changes in market interest rates. Client facing activities, pri-

marily lending and deposit-taking, create interest rate sensitive positions

on our balance sheet. Interest rate risk from these activities, as well as

the impact of changing market conditions, is managed through our ALM

activities.

Simulations are used to estimate the impact on core net interest

income – managed basis using numerous interest rate scenarios, bal-

ance sheet trends and strategies. These simulations evaluate how these

scenarios impact core net interest income – managed basis on short-term

financial instruments, debt securities, loans, deposits, borrowings, and

derivative instruments. In addition, these simulations incorporate

assumptions about balance sheet dynamics such as loan and deposit

growth and pricing, changes in funding mix, and asset and liability repric-

ing and maturity characteristics. These simulations do not include the

impact of hedge ineffectiveness.

Management analyzes core net interest income – managed basis

forecasts utilizing different rate scenarios, with the base case utilizing the

forward interest rates. Management frequently updates the core net inter-

est income – managed basis forecast for changing assumptions and dif-

fering outlooks based on economic trends and market conditions. Thus,

we continually monitor our balance sheet position in an effort to maintain

an acceptable level of exposure to interest rate changes.

We prepare forward-looking forecasts of core net interest income –

managed basis. These baseline forecasts take into consideration

expected future business growth, ALM positioning, and the direction of

interest rate movements as implied by forward interest rates. We then

measure and evaluate the impact that alternative interest rate scenarios

have to these static baseline forecasts in order to assess interest rate

sensitivity under varied conditions. The spot and 12-month forward

monthly rates used in our respective baseline forecasts at December 31,

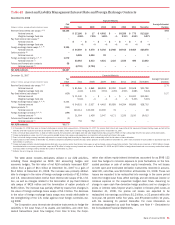

2008 and 2007 are shown in Table 40.

At December 31, 2008, the spread between the three-month LIBOR

rate and the Federal Funds target rate had significantly widened since

December 31, 2007. We are typically asset sensitive to Federal Funds

and Prime rates, and liability sensitive to LIBOR. As the Federal Funds

and LIBOR dislocation widens, the benefit to net interest income from

lower rates is limited. Subsequent to December 31, 2008, the spread

between the three-month LIBOR rate and the Federal Funds target rate

has narrowed.

Table 40 Forward Rates

December 31

2008 2007

Federal

Funds

Three-Month

LIBOR

10-Year

Swap

Federal

Funds

Three-Month

LIBOR

10-Year

Swap

Spot rates

0.25% 1.43% 2.56%

4.25% 4.70% 4.67%

12-month forward rates

0.75

1.41 2.80 3.13 3.36 4.79

88

Bank of America 2008