Bank of America 2008 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

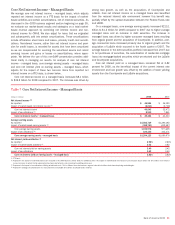

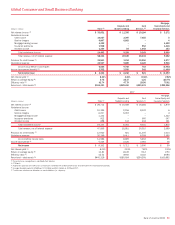

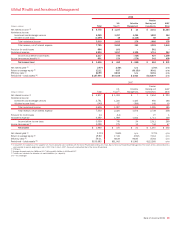

|

|

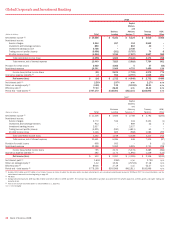

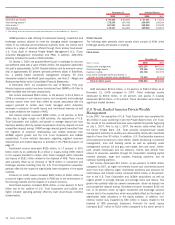

At December 31, 2008, we had no forward leveraged finance com-

mitments and the carrying value of our leveraged funded positions held

for distribution was $2.8 billion. At December 31, 2007, the carrying

value of the Corporation’s forward leveraged finance commitments and

leveraged funded positions held for distribution were $11.9 billion and

$5.9 billion. The elimination of our forward leveraged finance commit-

ments was due to the funding of previously outstanding commitments,

approximately 66 percent of which were distributed through syndi-

cation, and client-terminated commitments. Pre-market disruption

exposure originated prior to September 30, 2007 had a carrying value

of $1.5 billion at December 31, 2008 as compared to $5.9 billion at

December 31, 2007. At December 31, 2008, 66 percent of the lever-

aged funded positions held for distribution were senior secured with an

approximate carrying value of $1.9 billion of which $1.4 billion were

originated prior to September 30, 2007.

ŠStructured products sales and trading revenue was a loss of $8.0 bil-

lion, which represented a decline in revenue of $2.7 billion compared

to the prior year. The decrease was driven by $4.8 billion of losses

resulting from our CDO exposure, which includes our super senior,

warehouse, and sales and trading positions, and our hedging activities

including counterparty credit risk valuations. See the detailed CDO

exposure discussion to follow. Also, structured products was adversely

impacted by $944 million of losses (net of hedges) on CMBS funded

debt and the forward finance commitments for 2008, and $545 million

in losses associated with equity investments we made in acquisition-

related financing transactions. In addition, 2008 included losses

related to other structured products including $738 million of losses

for counterparty credit risk valuations related to our structured credit

trading business. Other structured products, including residential

mortgage-backed securities as well as other residual structured credit

positions were negatively impacted by spread widening and extreme

dislocations in basis correlations in both domestic and foreign markets

that occurred in the fourth quarter of 2008. The results of 2007 were

adversely impacted by the market disruptions that began during the

third quarter of 2007.

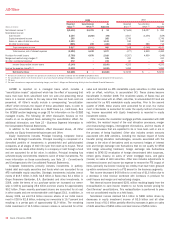

At December 31, 2008 and 2007, we held $6.9 billion and $13.6

billion of funded CMBS debt of which $6.0 billion and $8.9 billion were

primarily floating-rate acquisition-related financings to major, well-

known operating companies. In addition, at December 31, 2008 and

2007, we had forward finance commitments of $700 million and $2.2

billion. The decrease in funded CMBS debt was driven by securitiza-

tions and loan sales, while the decrease in forward finance commit-

ments was driven by the funding of outstanding commitments and the

business decision not to enter into any new floating-rate acquisition-

related financings. Forward finance commitments at December 31,

2008 were comprised primarily of fixed-rate conduit product financings.

The $944 million of losses recorded during 2008 associated with our

CMBS exposure were concentrated in the more difficult to hedge

floating-rate debt.

ŠEquity products sales and trading revenue decreased $512 million to

$813 million in 2008 compared to 2007 primarily due to lower trading

results in the institutional derivatives businesses and the sale of our

equity prime brokerage business that occurred in the third quarter of

2008.

Collateralized Debt Obligation Exposure at December 31, 2008

CDO vehicles hold diversified pools of fixed income securities. CDO

vehicles issue multiple tranches of debt securities, including commercial

paper, mezzanine and equity securities.

Our CDO exposure can be divided into funded and unfunded super

senior liquidity commitment exposure, other super senior exposure (i.e.,

cash positions and derivative contracts), warehouse, and sales and trad-

ing positions. For more information on our CDO liquidity commitments,

refer to Collateralized Debt Obligation Vehicles as part of Off- and

On-Balance Sheet Arrangements beginning on page 49. Super senior

exposure represents the most senior class of commercial paper or notes

that are issued by the CDO vehicles. These financial instruments benefit

from the subordination of all other securities issued by the CDO vehicles.

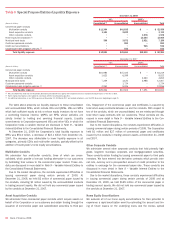

During 2008, we recorded CDO-related losses of $4.8 billion com-

pared to $5.6 billion in 2007 including losses on super senior exposure

of $3.6 billion and $4.0 billion. Also included in CDO-related losses in

2008 were $707 million of losses on purchased securities from liqui-

dated CDO vehicles. These securities were purchased from the vehicles

at auction and the losses were recorded subsequent to their purchase.

CDO-related losses reduced trading account profits (losses) by $1.6 bil-

lion and other income by $3.2 billion. Also included during 2008 were net

gains of $893 million related to our hedging activity, $315 million of

losses related to subprime sales and trading and CDO warehouse posi-

tions, and $1.1 billion of losses to cover counterparty risk on our CDO

and subprime-related exposure. The losses recorded in other income

noted above were other-than-temporary impairment charges related to

CDOs and purchased securities classified as AFS debt securities at

December 31, 2008. Also we had unrealized losses on uninsured other

super senior cash positions and purchased securities from liquidated

CDOs of $422 million (pre-tax) in accumulated OCI at December 31,

2008.

The CDO and related markets continued to deteriorate during 2008,

experiencing significant illiquidity impacting the availability and reliability

of transparent pricing. At December 31, 2008, we valued these CDO

structures consistent with how we valued them at December 31, 2007.

We assumed the CDO structures would terminate and looked through the

structures to the underlying net asset values of the securities. We were

able to obtain security values using either external pricing services or

offsetting trades for approximately 94 percent of the CDO exposure for

which we used the average of all prices obtained by security. The majority

of the remaining positions where no pricing quotes were available were

valued using matrix pricing by aligning the value to securities that had

similar vintage of underlying assets and ratings, using the lowest rating

between the rating services. The remaining securities were valued as

interest-only strips, based on estimated average life, exposure type and

vintage of the underlying assets. We assigned a zero value to the CDO

positions for which an event of default has been triggered and liquidation

notice has been issued. The value of cash held by the trustee for all CDO

structures was also incorporated into the resulting net asset value. In

addition, we were able to obtain security values using the same method-

ology as the CDO exposure for approximately 65 percent of the purchased

securities from liquidated CDOs. Similarly, the majority of the remaining

positions where no pricing quotes were available were valued using matrix

pricing and projected cash flows.

Bank of America 2008

41