Bank of America 2008 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

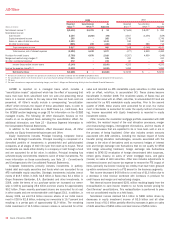

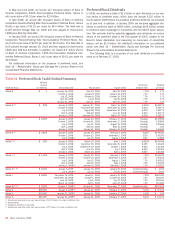

available to cover such losses and by evaluating any estimated shortfalls

in relation to contractually defined triggers. As of December 31, 2008,

$13.1 billion of outstanding principal balances of our home equity

securitization transactions were in rapid amortization. Another $2.8 billion

of outstanding principal balances in our home equity securitization trans-

actions are expected to enter rapid amortization.

The Corporation is responsible for funding additional borrower draws

on home equity lines of credit underlying our securitization transactions.

When transactions enter rapid amortization, principal collections on

underlying loans are used to pay investor interests. This has the effect of

extending the time period for which the Corporation’s advances are out-

standing and we may not receive reimbursement for all of the funds

advanced to borrowers, as senior bondholders and monoline insurers

have priority for repayment. While the available credit line for home equity

securitization transactions in or expected to be in rapid amortization was

approximately $1.0 billion at December 31, 2008, a maximum funding

obligation attributable to rapid amortization cannot be calculated as the

borrower has the ability to pay down and redraw balances. The amount in

Table 8 equals the principal balance of the outstanding trust certificates

that are subject to rapid amortization or $13.1 billion at December 31,

2008. This amount is significantly higher than the amount we expect to

fund. The charges we will ultimately record as a result of the rapid amor-

tization events are dependent on the performance of the loans, the

amount of subsequent draws, and the timing of related cash flows. At

December 31, 2008, the reserve for losses on expected future draw obli-

gations on the home equity securitizations in or expected to be in rapid

amortization was $345 million. For additional information on home equity

securitizations, see Note 8 – Securitizations to the Consolidated Financial

Statements.

Municipal Bond Trusts

We administer municipal bond trusts that hold highly rated, long-term,

fixed-rate municipal bonds. The trusts obtain financing by issuing floating-

rate trust certificates that reprice on a weekly basis to third party invest-

ors. We serve as remarketing agent and liquidity provider for the trusts.

These trusts are discussed in more detail in Note 9 – Variable Interest

Entities to the Consolidated Financial Statements.

At December 31, 2008 and 2007, we held $688 million and $125

million of floating rate certificates issued by unconsolidated municipal

bond trusts in trading account assets. This increase is attributable to illi-

quidity in the marketplace that occurred during the second half of 2008.

Customer-Sponsored Conduits

We provide liquidity facilities to conduits that are sponsored by our cus-

tomers and which provide them with direct access to the commercial

paper market. We are typically one of several liquidity providers for a

customer’s conduit. We do not provide SBLCs or other forms of credit

enhancement to these conduits. Assets of these conduits consist primar-

ily of auto loans, student loans and credit card receivables. The liquidity

commitments benefit from structural protections which vary depending

upon the program, but given these protections, the exposures are viewed

to be of investment grade quality.

These commitments are included in Note 13 – Commitments and

Contingencies to the Consolidated Financial Statements. As we typically

provide less than 20 percent of the total liquidity commitments to these

conduits and do not provide other forms of support, we have concluded

that we do not hold a significant variable interest in the conduits and they

are not included in our discussion of VIEs in Note 9 – Variable Interest

Entities to the Consolidated Financial Statements.

Credit Card Securitizations

During the second half of 2008, we entered into a liquidity support agree-

ment related to our commercial paper program that obtains financing by

issuing tranches of commercial paper backed by credit card receivables

to third party investors from a trust sponsored by the Corporation. If cer-

tain criteria are met, such as not being able to reissue the commercial

paper due to market illiquidity, the commercial paper maturity dates can

be extended to 390 days from the original issuance date. This extension

would cause the outstanding commercial paper to convert to an interest

bearing note and subsequent credit card receivable collections would be

applied to the outstanding note balance. If any of the investor notes are

still outstanding at the end of the extended maturity period, our liquidity

commitment obligates us to purchase maturity notes in order to retire the

investor notes. As a maturity note holder, we would be entitled to the

remaining cash flows from the collateralizing credit card receivables. At

December 31, 2008 there were no maturity notes outstanding and we

held $5.0 billion of investment grade securities in AFS debt securities

issued by the trust due to illiquidity in the marketplace. For more

information on how our credit card securitizations impact our liquidity, see

the Liquidity Risk and Capital Management discussion on page 55.

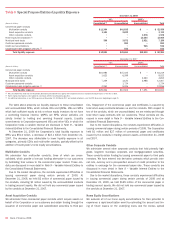

Collateralized Debt Obligation Vehicles

CDO vehicles hold diversified pools of fixed income securities which they

fund by issuing multiple tranches of debt securities, including commercial

paper, and equity securities. We provided liquidity support in the form of

written put options to several CDOs totaling $542 million and $10.0 bil-

lion at December 31, 2008 and 2007. In addition, we provided other liq-

uidity support to a CDO conduit of $2.3 billion at December 31, 2007.

These CDOs are discussed in more detail in Note 9 – Variable Interest

Entities to the Consolidated Financial Statements.

The decrease in liquidity support was primarily due to the termination

of $7.0 billion of put options for three CDOs and the termination of a

$2.3 billion liquidity commitment to the CDO conduit, all of which were

liquidated during 2008. Additionally, our liquidity support was reduced by

$2.2 billion as put options related to two CDOs were consolidated on our

balance sheet following a change in contractual arrangements and for

which we now hold all of the remaining outstanding commercial paper. At

December 31, 2008, we have effectively eliminated our liquidity support

for these CDOs.

At December 31, 2008, we held commercial paper of $323 million on

the balance sheet that was issued by one unconsolidated CDO. At

December 31, 2007, we held commercial paper of $6.6 billion that was

issued by unconsolidated CDOs and the CDO conduit.

For more information on our super senior CDO exposure and related

writedowns, see our CDO exposure discussion beginning on page 41. As

noted in the Super Senior Collateralized Debt Obligation Exposure, on

page 42, we had net liquidity exposure of $476 million at December 31,

2008, which is net of cumulative writedowns of $66 million. At

December 31, 2007, we had net liquidity exposure of $7.8 billion. This

amount reflects gross exposure of $12.3 billion less insurance of $1.8

billion and cumulative writedowns of $2.7 billion.

Obligations and Commitments

We have contractual obligations to make future payments on debt and

lease agreements. Additionally, in the normal course of business, we

enter into contractual arrangements whereby we commit to future pur-

chases of products or services from unaffiliated parties. Obligations that

are legally binding agreements whereby we agree to purchase products or

services with a specific minimum quantity defined at a fixed, minimum or

variable price over a specified period of time are defined as purchase

obligations. Included in purchase obligations in Table 9 are vendor con-

Bank of America 2008

51