Bank of America 2008 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

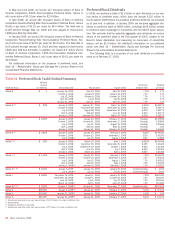

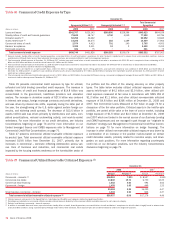

Commercial Portfolio Credit Risk Management

Credit risk management for the commercial portfolio begins with an

assessment of the credit risk profile of the borrower or counterparty

based on an analysis of their financial position. As part of the overall

credit risk assessment of a borrower or counterparty, most of our

commercial credit exposures are assigned a risk rating and are subject to

approval based on defined credit approval standards. Subsequent to loan

origination, risk ratings are monitored on an ongoing basis. If necessary,

risk ratings are adjusted to reflect changes in the financial condition,

cash flow or financial situation of a borrower or counterparty. We use risk

rating aggregations to measure and evaluate concentrations within portfo-

lios. Risk ratings are a factor in determining the level of assigned

economic capital and the allowance for credit losses. In making credit

decisions, we consider risk rating, collateral, country, industry and single

name concentration limits while also balancing the total borrower or coun-

terparty relationship. Our lines of business and risk management person-

nel use a variety of tools to continuously monitor the ability of a borrower

or counterparty to perform under its obligations.

For information on our accounting policies regarding delinquencies,

nonperforming status and charge-offs for the commercial portfolio, see

Note 1 – Summary of Significant Accounting Principles to the Con-

solidated Financial Statements.

Management of Commercial Credit Risk

Concentrations

Commercial credit risk is evaluated and managed with a goal that concen-

trations of credit exposure do not result in undesirable levels of risk. We

review, measure, and manage concentrations of credit exposure by

industry, product, geography and customer relationship. Distribution of

loans and leases by loan size is an additional measure of portfolio risk

diversification. We also review, measure, and manage commercial real

estate loans by geographic location and property type. In addition, within

our international portfolio, we evaluate borrowings by region and by coun-

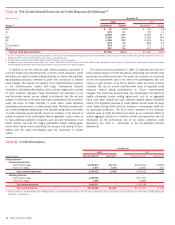

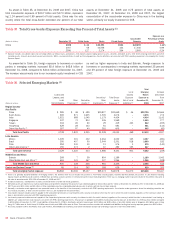

try. Tables 28, 30, 34, 35 and 36 summarize our concentrations. Addi-

tionally, we utilize syndication of exposure to third parties, loan sales,

hedging and other risk mitigation techniques to manage the size and risk

profile of the loan portfolio.

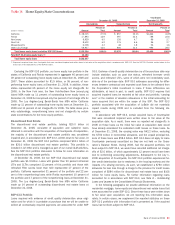

From the perspective of portfolio risk management, customer concen-

tration management is most relevant in GCIB. Within that segment’s

Business Lending and CMAS businesses, we facilitate bridge financing

(high grade debt, high yield debt, CMBS and equity) to fund acquisitions,

recapitalizations and other short-term needs as well as provide syndi-

cated financing for our clients. These concentrations are managed in part

through our established “originate to distribute” strategy. These client

transactions are sometimes large and leveraged. They can also have a

higher degree of risk as we are providing offers or commitments for vari-

ous components of the clients’ capital structures, including lower rated

unsecured and subordinated debt tranches and/or equity. In normal

markets, many of these offers to finance will not be accepted, and if

accepted, these conditional commitments are often retired prior to or

shortly following funding via the placement of securities, syndication or

the client’s decision to terminate. However, as we began to experience in

the latter half of 2007, where we have a binding commitment and there is

a market disruption or other unexpected event, these commitments are

more likely to be funded and are more difficult to distribute. As a con-

sequence there is heightened exposure in the portfolios and a higher

potential for writedown or loss. For more information regarding the Corpo-

ration’s leveraged finance and CMBS exposures, see the CMAS dis-

cussion beginning on page 40.

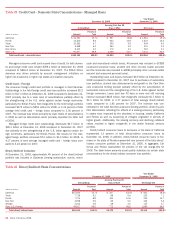

We account for certain large corporate loans and loan commitments

(including issued but unfunded letters of credit which are considered uti-

lized for credit risk management purposes), which exceed our single

name credit risk concentration guidelines at fair value in accordance with

SFAS 159. Any fair value adjustment upon origination and subsequent

changes in the fair value of these loans and unfunded commitments are

recorded in other income. By including the credit risk of the borrower in

the fair value adjustments, any credit deterioration or improvement is

recorded immediately as part of the fair value adjustment. As a result, the

allowance for loan and lease losses and the reserve for unfunded lending

commitments are not used to capture credit losses inherent in these

nonperforming or impaired loans and unfunded commitments. The

Commercial Credit Portfolio tables exclude loans and unfunded commit-

ments that are carried at fair value to adjust related ratios. See the

Commercial Loans Measured at Fair Value section on page 74 for more

information on the performance of these loans and loan commitments

and see Note 19 – Fair Value Disclosures to the Consolidated Financial

Statements for additional information on our SFAS 159 elections.

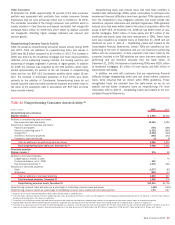

The merger with Merrill Lynch will increase our concentrations to cer-

tain industries, countries and customers. These increases are primarily

with diversified financial institutions active in the capital markets. There

are also increased concentrations within the high-grade commercial

portfolio, monoline insurers, certain leveraged finance exposures, and

several large CMBS positions.

70

Bank of America 2008