Bank of America 2008 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

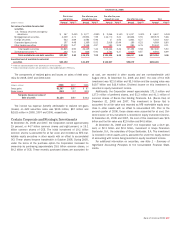

|

|

under the long-term contracts are received. Approximately 74 percent of

this exposure is insured. At December 31, 2008, the weighted average

life of assets in the consolidated conduit was estimated to be 3.1 years

and the weighted average maturity of commercial paper issued by this

conduit was 33 days. Assets of the Corporation are not available to pay

creditors of the consolidated conduit except to the extent the Corporation

may be obligated to perform under the liquidity commitments and SBLCs.

Assets of the consolidated conduit are not available to pay creditors of

the Corporation.

At December 31, 2008, the Corporation’s liquidity commitments to

the unconsolidated conduits were mainly collateralized by credit card

loans (23 percent), student loans (17 percent), auto loans (14 percent),

trade receivables (10 percent), and equipment loans (seven percent). In

addition, 23 percent of the Corporation’s commitments were collateral-

ized by the conduits’ short-term lending arrangements with investment

funds, primarily real estate funds, which, as previously mentioned,

incorporate features that provide credit support. Amounts advanced under

these arrangements are secured by a diverse group of high quality equity

investors. Outstanding advances under these facilities will be repaid

when the investment funds issue capital calls. At December 31, 2008,

the weighted average life of assets in the unconsolidated conduits was

estimated to be 3.6 years and the weighted average maturity of commer-

cial paper issued by these conduits was 37 days.

The Corporation’s liquidity, SBLCs and similar loss protection commit-

ments obligate us to purchase assets from the conduits at the conduits’

cost. Subsequent realized losses on assets purchased from the uncon-

solidated conduits would be reimbursed from restricted cash accounts

that were funded by the issuance of capital notes and equity interests to

third party investors. The Corporation would absorb losses in excess of

such amounts. If a conduit is unable to re-issue commercial paper due to

illiquidity in the commercial paper markets or deterioration in the asset

portfolio, the Corporation is obligated to provide funding subject to the

following limitations. The Corporation’s obligation to purchase assets

under the SBLCs and similar loss protection commitments are subject to

a maximum commitment amount which is typically set at eight to 10

percent of total outstanding commercial paper. The Corporation’s obliga-

tion to purchase assets under the liquidity agreements, which comprise

the remainder of our exposure, is generally limited to the amount of

non-defaulted assets. Although the SBLCs are unconditional, we are not

obligated to fund under other liquidity or loss protection commitments if

the conduit is the subject of a voluntary or involuntary bankruptcy

proceeding.

One of the unconsolidated conduits holds CDO investments with an

aggregate outstanding par value of $388 million. The underlying collateral

includes middle market loans held in an insured CDO (65 percent) and

subprime residential mortgages (12 percent), with the remainder of the

collateral consisting primarily of investment grade securities. During

2008, these investments were downgraded or threatened with a down-

grade by the rating agencies. In accordance with the terms of our existing

liquidity obligations, the Corporation funded these investments in a trans-

action that was accounted for as a secured borrowing, and the invest-

ments no longer serve as collateral for commercial paper issuances. The

Corporation will be reimbursed for any realized losses on these invest-

ments up to the amount of capital notes issued by the conduit. There

were no other significant downgrades nor were any losses recorded in

earnings from writedowns of assets held by any of the conduits during

this period.

The liquidity commitments and SBLCs provided to unconsolidated

conduits are included in Note 13 – Commitments and Contingencies to

the Consolidated Financial Statements.

Asset Acquisition Conduits

The Corporation administers three asset acquisition conduits which

acquire assets on behalf of the Corporation or our customers. Two of the

conduits, which are unconsolidated, acquire assets at the request of

customers who wish to benefit from the economic returns of the specified

assets, which consist principally of liquid exchange-traded equity secu-

rities and some leveraged loans, on a leveraged basis. The consolidated

conduit holds subordinated debt securities for the Corporation’s benefit.

The conduits obtain funding by issuing commercial paper and sub-

ordinated certificates to third party investors. Repayment of the commer-

cial paper and certificates is assured by total return swap contracts

between the Corporation and the conduits and, for unconsolidated con-

duits, the Corporation is reimbursed through total return swap contracts

with its customers. The weighted average maturity of commercial paper

issued by the conduits at December 31, 2008 was 54 days. The Corpo-

ration receives fees for serving as commercial paper placement agent

and for providing administrative services to the conduits.

The Corporation determines whether it must consolidate an asset

acquisition conduit based on the design of the conduit and whether the

third party investors are exposed to the Corporation’s credit risk or the

market risk of the assets. Interest rate risk is not included in the cash

flow analysis because the conduits are not designed to absorb and pass

along interest rate risk to investors, who receive current rates of interest

that are appropriate for the tenor and relative risk of their invest-

ments. When a conduit acquires assets for the benefit of the Corpo-

ration’s customers, the Corporation enters into back-to-back total return

swaps with the conduit and the customer such that the economic returns

of the assets are passed through to the customer. The Corporation’s

performance under the derivatives is collateralized by the underlying

assets and, as such, the third party investors are exposed primarily to

credit risk of the Corporation. The Corporation’s exposure to the counter-

party credit risk of its customers is mitigated by the aforementioned

collateral arrangements and the ability to liquidate an asset held in the

conduit if the customer defaults on its obligation. When a conduit

acquires assets on the Corporation’s behalf and the Corporation absorbs

the market risk of the assets, it consolidates the conduit.

Derivative activity related to unconsolidated conduits is carried at fair

value with changes in fair value recorded in trading account profits

(losses).

Municipal Bond Trusts

The Corporation administers municipal bond trusts that hold highly-rated,

long-term, fixed-rate municipal bonds, some of which are callable prior to

maturity. The majority of the bonds are rated AAA or AA and some of the

bonds benefit from insurance provided by monolines. The trusts obtain

financing by issuing floating-rate trust certificates that reprice on a weekly

basis to third party investors. The floating-rate investors have the right to

tender the certificates at any time upon seven days notice. The Corpo-

ration serves as remarketing agent and liquidity provider for the trusts.

Should the Corporation be unable to remarket the tendered certificates, it

is generally obligated to purchase them at par. The Corporation is not

obligated to purchase the certificate if a bond’s credit rating declines

below investment grade or in the event of certain defaults or bankruptcy

of the issuer and insurer. The weighted average remaining life of bonds

held in the trusts at December 31, 2008 was 11.8 years. There were no

material writedowns or downgrades of assets or issuers during 2008.

Some of these trusts are QSPEs and, as such, are not subject to

consolidation by the Corporation. The Corporation consolidates those

trusts that are not QSPEs if it holds the residual interests or otherwise

146

Bank of America 2008