Bank of America 2008 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

Trading Risk and Return

Daily Trading-related Revenue and VAR

-300

-250

-200

-150

-100

-50

0

50

100

150

200

250

(Dollars in millions)

Daily

Trading-

related

Revenue

VAR

12/31/2007 3/31/2008 6/30/2008 9/30/2008 12/31/2008

Table 39 Trading Activities Market Risk VAR

12 Months Ended December 31

2008 2007

VAR VAR

(1)

(Dollars in millions) Average High

(2)

Low

(2)

Average High

(2)

Low

(2)

Foreign exchange

$ 7.7 $ 11.7 $ 5.0

$ 7.2 $25.3 $ 3.8

Interest rate

28.9 68.3 12.4

13.9 31.9 6.6

Credit

84.6 185.2 44.1

39.5 69.9 23.4

Real estate/mortgage

22.7 43.1 12.8

14.1 23.5 5.7

Equities

28.0 63.9 15.5

24.6 45.8 9.6

Commodities

8.2 17.7 2.4

7.2 10.7 3.7

Portfolio diversification

(69.4) – –

(53.9) – –

Total market-based trading portfolio (3)

$110.7 $255.7 $64.1

$ 52.6 $91.5 $32.9

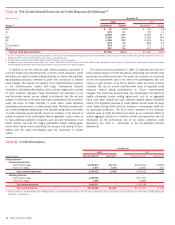

(1) Excludes our discrete writedowns on super senior CDO exposure.

(2) The high and low for the total portfolio may not equal the sum of the individual components as the highs or lows of the individual portfolios may have occurred on different trading days.

(3) The table above does not include credit protection purchased to manage our counterparty credit risk.

Table 39 presents average, high and low daily trading VAR for the 12

months ended December 31, 2008 and 2007.

The increases in average VAR during 2008 as compared to 2007 were

due to the rise in market volatility that started during the second half of

2007 and accelerated into the fourth quarter of 2008. As previously dis-

cussed, we updated our VAR model during the first quarter of 2008 and

as the increased market volatility was incorporated into the historical

price data, the level of VAR increased substantially.

Counterparty credit risk is an adjustment to the mark-to-market value

of our derivative exposures reflecting the impact of the credit quality of

counterparties on our derivative assets. Since counterparty credit

exposure is not included in the VAR component of the regulatory capital

allocation, we do not include it in our trading VAR, and it is therefore not

included in the daily trading-related revenue illustrated in our histogram

and used for backtesting. At December 31, 2008 and 2007, the VAR for

counterparty credit risk, together with associated hedges that are marked

to market, was $86 million and $13 million.

Stress Testing

Because the very nature of a VAR model suggests results can exceed our

estimates, we also “stress test” our portfolio. Stress testing estimates

the value change in our trading portfolio that may result from abnormal

market movements. Various types of stress tests are run regularly

against the overall trading portfolio and individual businesses. Historical

scenarios simulate the impact of price changes which occurred during a

set of extended historical market events. The results of these scenarios

are reported daily to management. During the 12 months ended

December 31, 2008, the largest daily losses among the historical scenar-

ios ranged from $21 million to $999 million. This can be compared with

losses from $9 million to $529 million for the historical scenarios during

the 12 months ended December 31, 2007. The increase in historical

stress values are primarily associated with the introduction of a new

scenario to reflect the ongoing credit crisis related to the credit market

disruptions that occurred during the past 12-15 months. Hypothetical

scenarios simulate the anticipated shocks from predefined market stress

events. These stress events include shocks to underlying market risk

variables which may be well beyond the shocks found in the historical

data used to calculate the VAR. In addition to the value afforded by the

results themselves this information provides senior management with a

clear picture of the trend of risk being taken given the relatively static

nature of the shocks applied. During the 12 months ended December 31,

2008, the largest losses among the hypothetical scenarios ranged from

Bank of America 2008

87