Bank of America 2008 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

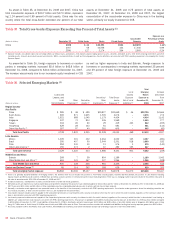

Table 41 Estimated Core Net Interest Income – Managed Basis at Risk

(Dollars in millions) December 31

Curve Change Short Rate (bps) Long Rate (bps) 2008 2007

+100 bps Parallel shift +100 +100

$ 144

$ (952)

-100 bps Parallel shift -100 -100

(186)

865

Flatteners

Short end +100 –

(545)

(1,127)

Long end – -100

(638)

(386)

Steepeners

Short end -100 –

453

1,255

Long end – +100

698

181

The table above reflects the pre-tax dollar impact to forecasted core

net interest income – managed basis over the next 12 months from

December 31, 2008 and 2007, resulting from a 100 bp gradual parallel

increase, a 100 bp gradual parallel decrease, a 100 bp gradual curve

flattening (increase in short-term rates or decrease in long-term rates)

and a 100 bp gradual curve steepening (decrease in short-term rates or

increase in long-term rates) from the forward market curve. For further

discussion of core net interest income – managed basis see page 31.

The sensitivity analysis above assumes that we take no action in

response to these rate shifts over the indicated years. The estimated

exposure is reported on a managed basis and reflects impacts that may

be realized primarily in net interest income and card income on the Con-

solidated Statement of Income. This sensitivity analysis excludes any

impact that could occur in the valuation of retained interests in the Corpo-

ration’s securitizations due to changes in interest rate levels. For addi-

tional information on securitizations, see Note 8 – Securitizations to the

Consolidated Financial Statements.

Our core net interest income – managed basis was asset sensitive at

December 31, 2008 and liability sensitive at December 31, 2007, with

the shift being driven by the lower level of rates. Over a 12-month horizon,

we would benefit from rising rates or a steepening of the yield curve

beyond what is already implied in the forward market curve.

As part of our ALM activities, we use securities, residential mort-

gages, and interest rate and foreign exchange derivatives in managing

interest rate sensitivity.

The acquisition of Merrill Lynch on January 1, 2009 made our core net

interest income – managed basis more asset sensitive to a parallel move

in interest rates. In addition, at January 1, 2009 we estimate that we

would continue to benefit from rising rates or a steepening of the yield

curve over a 12-month horizon, beyond what is already implied in the

forward market curve.

Securities

The securities portfolio is an integral part of our ALM position and is

primarily comprised of debt securities and includes mortgage-backed

securities and to a lesser extent corporate, municipal and other invest-

ment grade debt securities. At December 31, 2008, AFS debt securities

were $276.9 billion compared to $213.3 billion at December 31, 2007.

This increase was due to the repositioning of our ALM portfolio due to

market liquidity and funding conditions as we increased the level of

mortgage-backed securities relative to loans and the acquisition of Coun-

trywide. During 2008 and 2007, we purchased AFS debt securities of

$184.2 billion and $28.0 billion, sold $119.8 billion and $27.9 billion,

and had maturities and received paydowns of $26.1 billion and $19.2

billion. We realized $1.1 billion and $180 million in gains on sales of

debt securities during 2008 and 2007. In addition, we securitized $26.1

billion and $5.5 billion of residential mortgage loans into mortgage-

backed securities which we retained during 2008 and 2007. We also

converted $4.9 billion of automobile loans into ABS which we retained

during 2008.

The amount of pre-tax accumulated OCI loss related to AFS debt secu-

rities increased by $6.4 billion during 2008 to $9.3 billion, driven by a

decrease in value of certain mortgage-backed securities attributable to

changes in market yields. For those securities that are in an unrealized

loss position, we have the intent and ability to hold these securities to

recovery.

Accumulated OCI includes $2.0 billion in after-tax losses at

December 31, 2008, including $5.9 billion of net unrealized losses

related to AFS debt securities and $3.9 billion of net unrealized gains

related to AFS marketable equity securities. Total market value of the AFS

debt securities was $276.9 billion at December 31, 2008 with a

weighted average duration of 2.7 years and primarily relates to our

mortgage-backed securities portfolio.

Prospective changes to the accumulated OCI amounts for the AFS

securities portfolio will be driven by further interest rate, credit or price

fluctuations (including market value fluctuations associated with our CCB

and Banco Itaú investments), the collection of cash flows including pre-

payment and maturity activity, and the passage of time. A portion of the

Corporation’s strategic investment in CCB and all of its investment in

Banco Itaú are carried at fair value. The carrying values of CCB and Banco

Itaú were $19.7 billion and $2.5 billion at December 31, 2008. Unreal-

ized gains (losses) on these investments of $4.8 billion and $(77) mil-

lion, net-of-tax, are subject to currency and price fluctuations, and are

recorded in accumulated OCI. During 2008, under the terms of our pur-

chase option, we increased our ownership to approximately 19 percent by

purchasing approximately $9.2 billion of the common shares of CCB.

These shares are restricted through August 2011 and are carried at cost.

In January 2009, we sold 5.6 billion common shares of our initial invest-

ment in CCB for approximately $2.8 billion resulting in a pre-tax gain of

approximately $1.9 billion and our ownership was reduced to 16.7 per-

cent.

We recognized $3.5 billion of other-than-temporary impairment losses

on AFS debt securities during 2008. These losses were primarily com-

prised of $3.2 billion of CDO-related writedowns. We also recognized

$661 million of other-than-temporary impairment losses on AFS market-

able equity securities during 2008. No such losses were recognized on

AFS marketable equity securities during 2007.

The impairment of AFS debt and marketable equity securities is based

on a variety of factors, including the length of time and extent to which

the market value has been less than cost; the financial condition of the

issuer of the security and its ability to recover market value; and the

Corporation’s intent and ability to hold the security to recovery. Based on

the Corporation’s evaluation of the above and other relevant factors, and

after consideration of the losses described in the paragraph above, we do

Bank of America 2008

89