Bank of America 2008 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

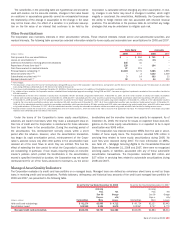

expects to absorb a majority of the variability created by changes in

market value of assets in the trusts and changes in market rates of inter-

est. The Corporation does not consolidate a trust if the customer holds

the residual interest and the Corporation is protected from loss in con-

nection with its liquidity obligations. For example, the Corporation may

have the ability to trigger the liquidation of a trust that is not a QSPE if

the market value of the bonds held in the trust declines below a specified

threshold which is designed to limit market losses to an amount that is

less than the customer’s residual interest, effectively preventing the

Corporation from absorbing the losses incurred on the assets held within

the trust.

The Corporation’s liquidity commitments to consolidated and uncon-

solidated trusts totaled $7.2 billion and $13.5 billion at December 31,

2008 and 2007. The decline is due principally to the liquidation of certain

consolidated trusts. Liquidity commitments to unconsolidated trusts of

$6.8 billion and $6.1 billion at December 31, 2008 and 2007 are

included in Note 13 – Commitments and Contingencies to the Con-

solidated Financial Statements.

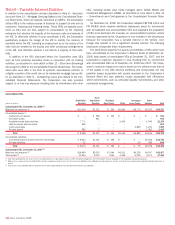

Collateralized Debt Obligation Vehicles

CDO vehicles hold diversified pools of fixed income securities. They issue

multiple tranches of debt securities, including commercial paper, and

equity securities. The Corporation receives fees for structuring CDOs and

providing liquidity support for super senior tranches of securities issued

by certain CDOs. No third parties provide a significant amount of similar

commitments to these CDOs.

The Corporation evaluates whether it must consolidate a CDO based

principally on a determination as to which party is expected to absorb a

majority of the credit risk created by the assets of the CDO. When the

Corporation structured certain CDOs, it acquired the super senior

tranches issued by the CDOs or provided commitments to support the

issuance of super senior commercial paper to third parties. When the

CDOs were first created, the Corporation did not expect its investments or

its liquidity commitments to absorb a significant amount of the variability

driven by the credit risk within the CDOs and did not consolidate the

CDOs. When the Corporation subsequently acquired commercial paper or

term securities issued by certain CDOs during 2008 and 2007, principally

as a result of our liquidity obligations, we performed updated con-

solidation analyses. Due to credit deterioration in the pools of securities

held by the CDOs, the updated analyses typically indicated that the

Corporation would now be expected to absorb a majority of the variability

and, accordingly, we consolidated these CDOs. Consolidation did not

have a significant impact on net income, as the Corporation’s invest-

ments and liquidity obligations were recorded at fair value prior to con-

solidation. The creditors of the consolidated CDOs have no recourse to

the general credit of the Corporation.

Liquidity commitments provided to CDOs include written put options

with a notional amount of $542 million and $10.0 billion at

December 31, 2008 and 2007. The written put options pertain to com-

mercial paper which is the most senior class of securities issued by the

CDOs and benefits from the subordination of all other securities issued

by the CDOs. The Corporation is obligated to provide funding to the CDOs

by purchasing the commercial paper at predetermined contractual yields

in the event of a severe disruption in the short-term funding market. The

decrease of $9.5 billion in the notional amount of written put options was

due primarily to the elimination of liquidity commitments to certain CDOs.

This amount includes $2.2 billion of put options related to two CDOs that

were consolidated by the Corporation due to a change in contractual

arrangements such as the conversion of commercial paper into term

notes and for which it now holds all of the remaining outstanding

commercial paper. It also includes $7.0 billion of put options that were

terminated due to liquidation of three CDOs.

At December 31, 2007, the Corporation also provided liquidity support

to a CDO conduit that held $2.3 billion of assets consisting of super

senior tranches of debt securities issued by other CDOs. The CDO con-

duit obtained funds by issuing commercial paper to third party investors.

During 2008, the Corporation purchased the assets and liquidated the

CDO conduit in accordance with our liquidity obligation due to a threat-

ened downgrade of the CDO conduit’s commercial paper. Four CDO

vehicles which issued securities formerly held in the CDO conduit are

consolidated on the Consolidated Balance Sheet of the Corporation at

December 31, 2008.

Leveraged Lease Trusts

The Corporation’s net involvement with consolidated leveraged lease

trusts totaled $5.8 billion and $6.2 billion at December 31, 2008 and

2007. The trusts hold long-lived equipment such as rail cars, power gen-

eration and distribution equipment, and commercial aircraft. The Corpo-

ration consolidates these trusts because it holds a residual interest

which is expected to absorb a majority of the variability driven by credit

risk of the lessee and, in some cases, by the residual risk of the leased

property. The net investment represents the Corporation’s maximum loss

exposure to the trusts in the unlikely event that the leveraged lease

investments become worthless. Debt issued by the leveraged lease

trusts is nonrecourse to the Corporation. The Corporation has no liquidity

exposure to these leveraged lease trusts.

Real Estate Investment Vehicles

The Corporation’s investment in real estate investment vehicles at

December 31, 2008 and 2007 consisted principally of limited partnership

investments in unconsolidated partnerships that finance the construction

and rehabilitation of affordable rental housing. The Corporation earns a

return primarily through the receipt of tax credits allocated to the afford-

able housing projects.

The Corporation determines whether it must consolidate these limited

partnerships based on a determination as to which party is expected to

absorb a majority of the risk created by the real estate held in the vehicle,

which may include construction, market and operating risk. Typically, the

general partner in a limited partnership will absorb a majority of this risk

due to the legal nature of the limited partnership structure. The Corpo-

ration’s risk of loss is mitigated by policies requiring that the project qual-

ify for the expected tax credits prior to making its investment. The

Corporation may from time to time be asked to invest additional amounts

to support a troubled project. Such additional investments have not been

and are not expected to be significant.

Customer Vehicles

Customer vehicles include credit-linked note vehicles and asset acquis-

ition vehicles, which are typically created on behalf of customers who

wish to obtain market or credit exposure to a specific company or finan-

cial instrument.

Credit-linked note vehicles issue notes linked to the credit risk of a

specified company or debt instrument, purchase high-grade assets as

collateral and enter into credit default swaps to synthetically create the

credit risk to pay the return on the notes. The Corporation is typically the

counterparty for some or all of the credit default swaps and, to a lesser

extent, it may invest in securities issued by the vehicles. The Corporation

does not consolidate the vehicles because the credit default swaps cre-

ate variability which is absorbed by the third party investors. The Corpo-

ration is exposed to loss if the collateral held by the vehicle declines in

Bank of America 2008

147