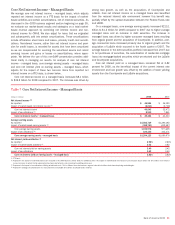

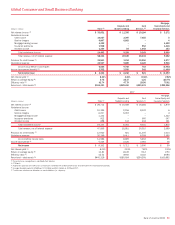

Bank of America 2008 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

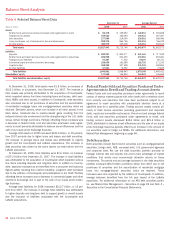

Loans and Leases, Net of Allowance for Loan and

Lease Losses

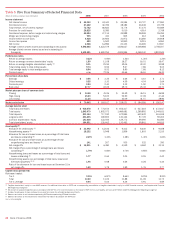

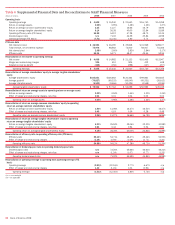

Period end and average loans and leases, net of allowance for loan and

lease losses increased $43.6 billion to $908.4 billion and $127.0 billion

to $893.4 billion in 2008 compared to 2007 due to consumer and

commercial organic growth and the addition of Countrywide. The average

consumer loan and lease portfolio increased $64.2 billion primarily due

to organic growth and the addition of Countrywide. The average commer-

cial loan and lease portfolio increased $70.5 billion primarily due to

organic growth and the acquisition of LaSalle which occurred in the fourth

quarter of 2007. For a more detailed discussion of the loan portfolio and

the allowance for credit losses, see Credit Risk Management beginning

on page 61, Note 6 – Outstanding Loans and Leases and Note 7 – Allow-

ance for Credit Losses to the Consolidated Financial Statements.

All Other Assets

Period end all other assets increased $44.7 billion at December 31,

2008, an increase of 13 percent from December 31, 2007, driven primar-

ily by the acquisition of Countrywide, which impacted various line items,

including MSRs and LHFS. In addition, the increase was driven by higher

derivative assets due to mark-to-market gains resulting from the reduced

interest rate environment and the strengthening of the U.S. dollar versus

certain foreign currencies.

Deposits

Period end and average deposits increased $77.8 billion to $883.0 bil-

lion and $114.0 billion to $831.1 billion in 2008 compared to 2007. The

average increase was due to a $95.3 billion increase in average domestic

interest-bearing deposits and a $19.4 billion increase in average

noninterest-bearing deposits. We categorize our deposits as core or

market-based deposits. Core deposits are generally customer-based and

represent a stable, low-cost funding source that usually reacts more

slowly to interest rate changes than market-based deposits. Core depos-

its include savings, NOW and money market accounts, consumer CDs

and IRAs, and noninterest-bearing deposits. Core deposits exclude nego-

tiable CDs, public funds, other domestic time deposits and foreign

interest-bearing deposits. Average core deposits increased $103.0 billion

to $696.9 billion in 2008, a 17 percent increase from the prior year. The

increase was attributable to growth in our average NOW and money mar-

ket accounts, average consumer CDs and IRAs and noninterest-bearing

deposits due to the addition of Countrywide and the benefit we received

from a consumer and business flight-to-safety resulting from market

instability. Average market-based deposit funding increased $11.0 billion

to $134.3 billion in 2008 compared to 2007 due to an increase in nego-

tiable CDs, public funds and other time deposits related to the funding of

growth in core and market-based assets. The increase in average depos-

its was also impacted by the assumption of deposits, primarily money

market, consumer CDs, and other domestic time deposits associated

with the LaSalle merger.

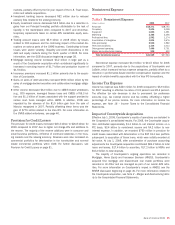

Federal Funds Purchased and Securities Sold Under

Agreements to Repurchase and Trading Account

Liabilities

Federal funds purchased and securities sold under agreements to

repurchase consist of deposits borrowed from other banks with a rela-

tively short-term maturity and securities that have been sold subject to an

agreement to repurchase securities with substantially identical terms at a

specified date for a specified price. Trading account liabilities consist

primarily of short positions in fixed income securities (including govern-

ment and corporate debt), equity and convertible instruments. Period end

federal funds purchased and securities sold under agreements to

repurchase, and trading account liabilities decreased $34.9 billion primar-

ily due to the rebalancing of hedges for market movements and lower

customer demand, and by the sale of our equity prime brokerage busi-

ness. Average federal funds purchased and securities sold under agree-

ments to repurchase, and trading account liabilities increased $12.0

billion primarily due to the relative low cost and availability of short-term

funding.

Commercial Paper and Other Short-term Borrowings

Commercial paper and other short-term borrowings provide a funding

source to supplement deposits in our ALM strategy. Period end commer-

cial paper and other short-term borrowings decreased $33.0 billion to

$158.1 billion in 2008 compared to 2007 due in part to the sale of our

equity prime brokerage business. Average commercial paper and other

short-term borrowings increased $11.4 billion to $182.7 billion in 2008

due to an increase in short-term funding given the change in market con-

ditions, partially offset by the sale of our equity prime brokerage busi-

ness.

Long-term Debt

Period end and average long-term debt increased $70.8 billion to $268.3

billion and $61.4 billion to $231.2 billion in 2008 compared to 2007.

The increases were attributable to issuances to support growth in overall

assets and enhance our liquidity, and the inclusion of long-term debt

associated with the Countrywide acquisition. Period end balances also

benefited from our participation in the TLGP and average balances bene-

fited from the LaSalle acquisition. For additional information on the TLGP,

see Regulatory Initiatives on page 20. For additional information on long-

term debt, see Note 12 – Short-term Borrowings and Long-term Debt to

the Consolidated Financial Statements.

Shareholders’ Equity

Period end shareholders’ equity increased $30.2 billion due to the issu-

ance of preferred stock including $15.0 billion to the U.S. Treasury in

connection with the TARP Capital Purchase Program, a common stock

offering of $9.9 billion, $4.2 billion of common stock issued in con-

nection with the Countrywide acquisition, and net income. These

increases were partially offset by a decrease in accumulated OCI and

higher preferred dividend payments. The decrease in accumulated OCI

was due to unrealized losses incurred on our debt and marketable equity

securities and the adverse impact of employee benefit plan adjustments

driven by the difference between the assumed and actual rate of return

on benefit plan assets during the year. For additional information on our

employee benefit plans, see Note 16 – Employee Benefit Plans to the

Consolidated Financial Statements. Average shareholders’ equity

increased $28.2 billion due to the same period end factors discussed

above, except accumulated OCI benefited from the fair value adjustment

related to our investment in China Construction Bank (CCB) which we

began to fair value in the fourth quarter of 2007.

Bank of America 2008

27