Bank of America 2008 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

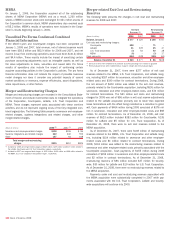

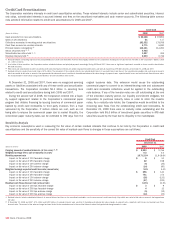

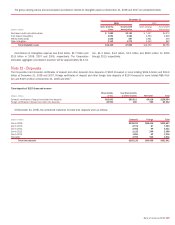

Credit Card Securitizations

The Corporation maintains interests in credit card securitization vehicles. These retained interests include senior and subordinated securities, interest-

only strips, subordinated interests in accrued interest and fees on the securitized receivables and cash reserve accounts. The following table summa-

rizes selected information related to credit card securitizations for 2008 and 2007.

Credit Card

(Dollars in millions) 2008 2007

Cash proceeds from new securitizations

$ 20,148

$ 19,851

Gains on securitizations

81

117

Collections reinvested in revolving period securitizations

162,332

178,556

Cash flows received on residual interests

5,771

6,590

Principal balance outstanding

(1)

114,141

114,450

Senior securities held

(2, 3)

4,965

–

Subordinated securities held

(2, 3)

1,837

424

Residual interests held

(4)

2,233

2,766

(1) Principal balance outstanding represents the principal balance of credit card receivables that have been legally isolated from the Corporation including those loans that are still held on the Corporation’s balance sheet

(i.e., seller’s interest).

(2) As a holder of these securities, the Corporation receives scheduled interest and principal payments accordingly. During 2008 and 2007, there were no significant impairments recorded on those securities classified as

AFS debt securities.

(3) Held senior and subordinated securities issued by credit card securitization vehicles are valued using quoted market prices and were all classified as AFS debt securities at December 31, 2008 and 2007.

(4) Residual interests include interest-only strips of $74 million. The remainder of the residual interests are subordinated interests in accrued interest and fees on the securitized receivables and cash reserve accounts

which are carried at fair value or amounts that approximate fair value and are not sensitive to favorable and adverse fair value changes in payment rates, expected credit losses and residual cash flows discount rates.

The residual interests were valued using model valuations and are classified in other assets.

At December 31, 2008 and 2007, there were no recognized servicing

assets or liabilities associated with any of these credit card securitization

transactions. The Corporation recorded $2.1 billion in servicing fees

related to credit card securitizations during both 2008 and 2007.

During the second half of 2008, the Corporation entered into a liquid-

ity support agreement related to the Corporation’s commercial paper

program that obtains financing by issuing tranches of commercial paper

backed by credit card receivables to third party investors from a trust

sponsored by the Corporation. If certain criteria are met, such as not

being able to reissue the commercial paper due to market illiquidity, the

commercial paper maturity dates can be extended to 390 days from the

original issuance date. This extension would cause the outstanding

commercial paper to convert to an interest-bearing note and subsequent

credit card receivable collections would be applied to the outstanding

note balance. If any of the investor notes are still outstanding at the end

of the extended maturity period, our liquidity commitment obligates the

Corporation to purchase maturity notes in order to retire the investor

notes. As a maturity note holder, the Corporation would be entitled to the

remaining cash flows from the collateralizing credit card receivables. At

December 31, 2008 there were no maturity notes outstanding and the

Corporation held $5.0 billion of investment grade securities in AFS debt

securities issued by the trust due to illiquidity in the marketplace.

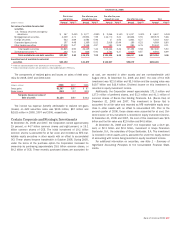

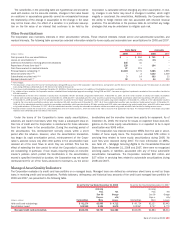

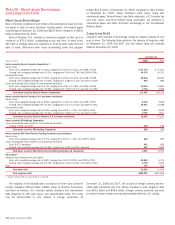

Sensitivity Analysis

Key economic assumptions used in measuring the fair value of certain residual interests that continue to be held by the Corporation in credit card

securitizations and the sensitivity of the current fair value of residual cash flows to changes in those assumptions are as follows:

Credit Card

December 31

(Dollars in millions) 2008 2007

Carrying amount of residual interests (at fair value) (1, 2)

$ 2,233

$ 2,766

Weighted average life to call or maturity (in years)

0.3

0.3

Monthly payment rate

10.7-13.9%

11.6-16.6%

Impact on fair value of 10% favorable change

$8

$51

Impact on fair value of 25% favorable change

22

158

Impact on fair value of 10% adverse change

(6)

(35)

Impact on fair value of 25% adverse change

(14)

(80)

Weighted average expected credit loss rate (annual rate)

9.0%

5.3%

Impact on fair value of 10% favorable change

$ 296

$ 141

Impact on fair value of 25% favorable change

741

374

Impact on fair value of 10% adverse change

(26)

(133)

Impact on fair value of 25% adverse change

(57)

(333)

Residual cash flows discount rate (annual rate)

13.5%

11.5%

Impact on fair value of 100 bps favorable change

$3

$9

Impact on fair value of 200 bps favorable change

4

13

Impact on fair value of 100 bps adverse change

(5)

(12)

Impact on fair value of 200 bps adverse change

(10)

(23)

(1) Residual interests include subordinated interests in accrued interest and fees on the securitized receivables, cash reserve accounts and interest-only strips which are carried at fair value or amounts that approximate

fair value.

(2) At December 31, 2008 and 2007, $74 million and $400 million of residual interests were sensitive to favorable and adverse fair value changes in payment rates, expected credit losses and residual cash flows

discount rates. The amount of the adverse change has been limited to the recorded amount of the residual interests where the hypothetical change exceeds its value.

142

Bank of America 2008