Bank of America 2008 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

very low prior year levels and higher net charge-offs and reserve increases

in the retail dealer-related loan portfolios due to deterioration and season-

ing of the portfolio reflective of growth.

Noninterest expense decreased $196 million, or nine percent, primar-

ily due to decreased incentive compensation partially offset by the

LaSalle merger.

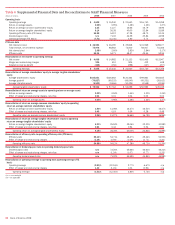

Capital Markets and Advisory Services

CMAS provides financial products, advisory services and financing glob-

ally to our institutional investor clients in support of their investing and

trading activities. We also work with our commercial and corporate issuer

clients to provide debt and equity underwriting and distribution capa-

bilities, merger-related advisory services and risk management products

using interest rate, equity, credit, currency and commodity derivatives,

foreign exchange, fixed income and mortgage-related products. The busi-

ness may take positions in these products and participate in market-

making activities dealing in government securities, equity and equity-

linked securities, high-grade and high-yield corporate debt securities,

commercial paper, mortgage-backed securities and ABS. Underwriting

debt and equity, securities research and certain market-based activities

are executed through Banc of America Securities, LLC which is our pri-

mary dealer.

CMAS recognized a net loss of $4.9 billion in 2008 compared to a net

loss of $3.4 billion in 2007. Market-based revenue was a net loss of

$3.1 billion as compared to net revenue of $479 million. These

decreases were driven by losses related to CDO exposure and the

continuing impact of the market disruptions on various parts of our busi-

ness including the severe volatility, illiquidity and credit dislocations that

were experienced in the debt and equity markets in the fourth quarter of

2008. Partially offsetting these declines were favorable results in our liq-

uid products and equity underwriting businesses. In addition, noninterest

expense declined $1.2 billion primarily due to lower performance-based

incentive compensation. For more information relating to our market-

based revenue, see the discussion below.

Market-based Revenue

CMAS evaluates its results using market-based revenue that is comprised

of net interest income and noninterest income. The following table pres-

ents further detail regarding market-based revenue. Sales and trading

revenue is segregated into fixed income from liquid products (primarily

interest rate and commodity derivatives and foreign exchange contracts),

credit products (primarily investment and noninvestment grade corporate

debt obligations, credit derivatives and public finance), structured prod-

ucts (primarily CMBS, residential mortgage-backed securities, structured

credit trading and CDOs), and equity income from equity-linked derivatives

and cash equity activity.

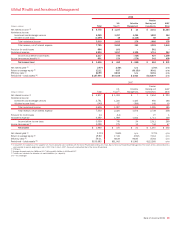

(Dollars in millions) 2008 2007

Investment banking income

Advisory fees

$ 287

$ 443

Debt underwriting

1,797

1,775

Equity underwriting

624

319

Total investment banking income

2,708

2,537

Sales and trading revenue

Fixed income:

Liquid products

3,608

2,155

Credit products

(2,273)

(212)

Structured products

(7,987)

(5,326)

Total fixed income

(6,652)

(3,383)

Equity income

813

1,325

Total sales and trading revenue

(5,839)

(2,058)

Total Capital Markets and Advisory Services

market-based revenue (1)

$(3,131)

$ 479

(1) Excludes $113 million and $70 million for 2008 and 2007 of net interest income on loans for which the

fair value option has been elected and is not considered market-based income.

Investment banking income increased $171 million to $2.7 billion as

compared to 2007 driven by increased equity underwriting fees partially

offset by lower advisory fees. Advisory fees were adversely impacted by

reduced activity due to the slowing economy. Equity underwriting income

was driven by fees earned on the Corporation’s stock issuances during

2008 for which CMAS was compensated on a management accounting

basis with a corresponding offset in All Other.

Sales and trading revenue declined $3.8 billion to a loss of $5.8 bil-

lion in 2008 compared to 2007. While structured products and credit

products reported losses for 2008, liquid products increased and equities

compared reasonably well with 2007 despite the continuing disruptive

market conditions.

ŠLiquid products sales and trading revenue increased $1.5 billion in

2008 compared to 2007 as CMAS took advantage of trending volatility

in interest rate and foreign exchange markets which also drove favor-

able client flows.

ŠCredit products sales and trading revenue declined $2.1 billion to a

loss of $2.3 billion in 2008 compared to 2007. During 2008, we

incurred losses of $1.1 billion, net of $286 million of fees, on lever-

aged loans and the forward leveraged finance commitments as investor

confidence faded and liquidity became largely non-existent. The few

institutions that were in a position to acquire additional loans, required

discount equivalent yields in excess of one-month LIBOR plus 1,000

bps in some instances, thus applying downward pressure to pricing

mechanisms, especially during the fourth quarter of 2008. Losses

incurred on our leveraged exposure were not concentrated in any one

type (senior secured or subordinated/senior unsecured) and were

generally due to wider new issuance credit spreads as compared to the

negotiated spreads. Credit products also incurred losses on ARS of

$898 million which included $312 million representing CMAS’s portion

of losses on the buyback from our customers. A significant portion of

these losses (i.e., $750 million) were concentrated in student loan

ARS. For further discussion on our ARS exposure, see Industry Concen-

trations beginning on page 76 and for a discussion on GWIM’s portion

of ARS losses on the buyback from our customers see page 45.

40

Bank of America 2008