Bank of America 2008 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

Other Consumer

At December 31, 2008, approximately 76 percent of the other consumer

portfolio was associated with portfolios from certain consumer finance

businesses that we have previously exited and is included in All Other.

The remainder consisted of the foreign consumer loan portfolio which is

mostly included in Card Services and deposit overdrafts. Net charge-offs

increased $121 million for 2008 from 2007 driven by deposit overdraft

net charge-offs reflecting higher average balances per account and

account growth.

Nonperforming Consumer Assets Activity

Table 24 presents nonperforming consumer assets activity during 2008

and 2007. Total net additions to nonperforming loans and leases in

2008 were $6.5 billion compared to $2.4 billion in 2007. The increase in

2008 was driven by the residential mortgage and home equity portfolios

reflective of the weakening housing markets, the slowing economy and

seasoning of vintages originated in periods of higher growth. In addition

for 2008 the increase was impacted by the CRA portfolio, which repre-

sented approximately 19 percent of the net increase in nonperforming

loans and the non SOP 03-3 Countrywide portfolio which added 15 per-

cent. The increase in foreclosed properties of $1.2 billion was driven

primarily by the addition of Countrywide. Nonperforming loans do not

include acquired loans that were considered impaired and written down to

fair value at the acquisition date in accordance with SOP 03-3 as these

loans accrete interest.

Nonperforming loans also include loans that have been modified in

troubled debt restructurings (TDRs) where concessions to borrowers who

experienced financial difficulties have been granted. TDRs typically result

from the Corporation’s loss mitigation activities and could include rate

reductions, payment extensions and principal forgiveness. TDRs generally

exclude loans that were written down to fair value at acquisition within the

scope of SOP 03-3. At December 31, 2008 we had $529 million of resi-

dential mortgages, $303 million of home equity and $71 million of dis-

continued real estate loans that were restructured in TDRs. These loans

were also classified as impaired loans at December 31, 2008 and are

disclosed as such in Note 6 – Outstanding Loans and Leases to the

Consolidated Financial Statements. Certain TDRs are classified as non-

performing at the time of restructure and are not returned to performing

status until six consecutive, on-time payments have been made by the

customer. Included in the TDR balances are loans that were classified as

performing and are therefore excluded from the table below. At

December 31, 2008, the balances of performing TDRs were $320 million

of residential mortgages, $1 million of home equity, and $66 million of

discontinued real estate.

In addition, we work with customers that are experiencing financial

difficulty through renegotiating credit card and direct/indirect consumer

loans, while ensuring that we remain within FFIEC guidelines. These

renegotiated loans are excluded from the table below as we do not

classify non-real estate unsecured loans as nonperforming. For more

information refer to Note 6 – Outstanding Loans and Leases to the Con-

solidated Financial Statements.

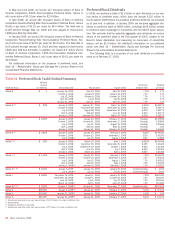

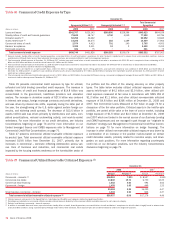

Table 24 Nonperforming Consumer Assets Activity (1)

(Dollars in millions) 2008 2007

Nonperforming loans and leases

Balance, January 1

$ 3,442

$1,030

Additions to nonperforming loans and leases:

New nonaccrual loans and leases

13,625

4,093

Reductions in nonperforming loans and leases:

Paydowns and payoffs

(704)

(366)

Returns to performing status

(2)

(1,522)

(855)

Charge-offs

(3)

(4,032)

(300)

Transfers to foreclosed properties

(895)

(152)

Transfers to loans held-for-sale

(6)

(8)

Total net additions to nonperforming loans and leases

6,466

2,412

Total nonperforming loans and leases, December 31 (4)

9,908

3,442

Foreclosed properties

Balance, January 1

276

59

Additions to foreclosed properties:

LaSalle balance, October 1, 2007

–

70

Countrywide balance, July 1, 2008

952

–

New foreclosed properties

(5)

1,578

246

Reductions in foreclosed properties:

Sales

(1,077)

(82)

Writedowns

(223)

(17)

Total net additions to foreclosed properties

1,230

217

Total foreclosed properties, December 31

1,506

276

Nonperforming consumer assets, December 31

$11,414

$3,718

Nonperforming consumer loans and leases as a percentage of outstanding consumer loans and leases

1.68%

0.62%

Nonperforming consumer assets as a percentage of outstanding consumer loans, leases and foreclosed properties

1.93

0.67

(1) Balances do not include nonperforming LHFS of $436 million and $95 million in 2008 and 2007.

(2) Consumer loans and leases may be restored to performing status when all principal and interest is current and full repayment of the remaining contractual principal and interest is expected, or when the loan otherwise

becomes well-secured and is in the process of collection.

(3) Our policy is not to classify consumer credit card and consumer non-real estate loans and leases as nonperforming; therefore, the charge-offs on these loans have no impact on nonperforming activity.

(4) Approximately half of the 2008 nonperforming loans and leases are greater than 180 days past due and have been written down through charge-offs to approximately 71 percent of original cost.

(5) Our policy is to record any losses in the value of foreclosed properties as a reduction in the allowance for credit losses during the first 90 days after transfer of a loan into foreclosed properties. Thereafter, all losses in

value are recorded as noninterest expense. New foreclosed properties in the table above are net of $436 million and $75 million of charge-offs in 2008 and 2007 taken during the first 90 days after transfer.

Bank of America 2008

69