Bank of America 2008 Annual Report Download - page 176

Download and view the complete annual report

Please find page 176 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

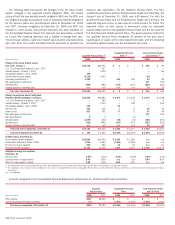

As of December 31, 2008 and 2007, the balance of the Corporation’s

UTBs which would, if recognized, affect the Corporation’s effective tax

rate was $2.6 billion (reflective of the January 1, 2009 adoption of SFAS

141R) and $1.8 billion. Included in the UTB balance are some items the

recognition of which would not affect the effective tax rate, such as the

tax effect of certain temporary differences, the portion of gross state

UTBs that would be offset by the tax benefit of the associated federal

deduction and UTBs related to acquired entities that may impact goodwill

if recognized during the initial measurement period for the acquisition. As

of December 31, 2008 and 2007, the portion of the UTB balance that

could impact goodwill if recognized in the future was $117 million and

$577 million.

The table below summarizes the status of significant U.S. federal

examinations for the Corporation and various acquired subsidiaries as of

December 31, 2008:

Company Years under examination

Status at

December 31, 2008

Bank of America Corporation 2000-2002 In Appeals process

Bank of America Corporation 2003-2005 Field examination

FleetBoston 1997-2000 In Appeals process

FleetBoston 2001-2004 Field examination

LaSalle 2003-2005 In Appeals process

Countrywide 2005-2006 Field examination

Countrywide 2007 Field examination

With the exception of the examinations of the 2003 through 2005 tax

years for the Corporation and the 2007 tax year for Countrywide, and

except as noted below, it is reasonably possible that all above examina-

tions will be concluded during 2009.

During 2008, the Internal Revenue Service (IRS) announced a settle-

ment initiative related to lease-in, lease-out (LILO) and sale-in, lease-out

(SILO) leveraged lease transactions. Pursuant to the settlement initiative,

the Corporation received offers to settle its LILOs and SILOs and

accepted these offers, which impact the years in Appeals and under

examination for the Corporation and FleetBoston. According to the terms

of the settlement initiative, an acceptance will not be binding until a clos-

ing agreement is executed by both parties, which is expected during

2009. The Corporation revised the assumptions used in accounting for

the projected cash flows of the relevant leases to reflect its expectation

of receiving the tax treatment proposed in the leasing settlement ini-

tiative. As a result of prior remittances, the Corporation does not expect

to pay any additional tax and interest related to the settlement initiative.

Upon the execution of a closing agreement for the settlement ini-

tiative, the Corporation’s remaining unagreed proposed adjustment for

the 2000 through 2002 tax years is the disallowance of foreign tax cred-

its related to certain structured investment transactions. The Corporation

continues to believe the crediting of these foreign taxes against U.S.

income taxes was appropriate. Except with respect to the foreign tax

credit issue, management believes it is reasonably possible that the

2000 through 2002 examinations can be concluded within the next

twelve months.

Considering all federal examinations, it is reasonably possible that the

UTB balance will decrease by as much as $650 million during the next

twelve months, since resolved items would be removed from the balance

whether their resolution resulted in payment or recognition.

All tax years subsequent to the above years remain open to examina-

tion.

The Corporation files income tax returns in more than 100 state and

foreign jurisdictions each year and is under continuous examination by

various state and foreign taxing authorities. While many of these examina-

tions are resolved every year, the Corporation does not anticipate that

resolutions occurring within the next twelve months would result in a

material change to the Corporation’s financial position.

During 2008 and 2007, the Corporation recognized within income tax

expense, $147 million and $161 million of interest and penalties, net of

tax. As of December 31, 2008 and 2007, the Corporation’s accrual for

interest and penalties that related to income taxes, net of taxes and

remittances, including applicable interest on certain leveraged lease posi-

tions, was $677 million and $573 million.

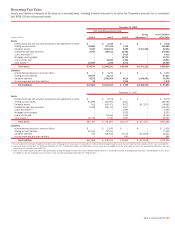

Significant components of the Corporation’s net deferred tax assets

and liabilities at December 31, 2008 and 2007 are presented in the fol-

lowing table.

December 31

(Dollars in millions) 2008 2007

Deferred tax assets

Allowance for credit losses

$ 8,042

$ 4,056

Security and loan valuations

5,590

3,673

Employee compensation and retirement

benefits

2,409

1,541

Accrued expenses

2,271

1,307

Net operating loss carryforwards

1,263

–

Available-for-sale securities

1,149

–

State income taxes

279

–

Other

1,987

73

Gross deferred tax assets

22,990

10,650

Valuation allowance

(1)

(272)

(148)

Total deferred tax assets, net of valuation

allowance

22,718

10,502

Deferred tax liabilities

Equipment lease financing

5,720

6,875

Mortgage servicing rights

3,404

859

Intangibles

1,712

2,015

Fee income

1,637

1,445

Available-for-sale securities

–

3,836

State income taxes

–

347

Other

1,549

1,667

Gross deferred liabilities

14,022

17,044

Net deferred tax assets (liabilities) (2)

$ 8,696

$ (6,542)

(1) At December 31, 2008 $115 million of the valuation allowance related to gross deferred tax assets was

attributable to the Countrywide merger. In accordance with SFAS 141R, tax attributes associated with

these gross deferred tax assets could result in tax benefits to reduce goodwill during a portion of 2009.

(2) The Corporation’s net deferred tax assets (liabilities) were adjusted during 2008 and 2007 to include

$3.5 billion of net deferred tax assets and $226 million of net deferred tax liabilities related to business

combinations.

The valuation allowance at December 31, 2008 and 2007 is attribut-

able to deferred tax assets generated in certain state and foreign juris-

dictions for which management believes it is more likely than not that

realization of these assets will not occur. The change in the valuation

allowance primarily resulted from certain state deferred tax assets

acquired in the Countrywide merger.

At December 31, 2008 and 2007, federal income taxes had not been

provided on $6.5 billion and $5.8 billion of undistributed earnings of for-

eign subsidiaries, earned prior to 1987 and after 1997 that have been

reinvested for an indefinite period of time. If the earnings were dis-

tributed, an additional $1.1 billion and $925 million of tax expense, net

of credits for foreign taxes paid on such earnings and for the related for-

eign withholding taxes, would have resulted as of December 31, 2008

and 2007.

174

Bank of America 2008