Bank of America 2008 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

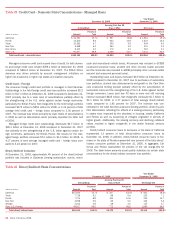

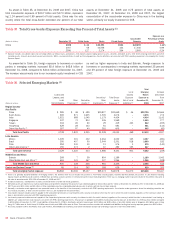

Table 32 Net Credit Default Protection by Credit Exposure Debt Rating (1)

(Dollars in millions) December 31

2008 2007

Ratings

(2)

Net Notional Percent Net Notional Percent

AAA

$30

(0.3)% $ (13) 0.2%

AA

(103)

1.1 (92) 1.3

A

(2,800)

29.0 (2,408) 33.7

BBB

(4,856)

50.2 (3,328) 46.6

BB

(1,948)

20.2 (1,524) 21.3

B

(579)

6.0 (180) 2.5

CCC and below

(278)

2.9 (75) 1.0

NR

(3)

880

(9.1) 474 (6.6)

Total net credit default protection

$(9,654)

100.0% $(7,146) 100.0%

(1) In order to mitigate the cost of purchasing credit protection, credit exposure can be added by selling credit protection. The distribution of debt rating for net notional credit default protection purchased is shown as a

negative and the net notional credit protection sold is shown as a positive amount.

(2) The Corporation considers ratings of BBB- or higher to meet the definition of investment grade.

(3) In addition to names which have not been rated, “NR” includes $948 million and $550 million in net credit default swaps index positions at December 31, 2008 and 2007. While index positions are principally

investment grade, credit default swaps indices include names in and across each of the ratings categories.

In addition to our net notional credit default protection purchased to

cover the funded and unfunded portion of certain credit exposures, credit

derivatives are used for market-making activities for clients and establish-

ing proprietary positions intended to profit from directional or relative

value changes. We execute the majority of our credit derivative positions

in the over-the-counter market with large, international financial

institutions, including broker/dealers and to a lesser degree with a variety

of other investors. Because these transactions are executed in the

over-the-counter market, we are subject to settlement risk. We are also

subject to credit risk in the event that these counterparties fail to perform

under the terms of these contracts. In most cases, credit derivative

transactions are executed on a daily margin basis. Therefore, events such

as a credit downgrade (depending on the ultimate rating level) or a breach

of credit covenants would typically require an increase in the amount of

collateral required of the counterparty (where applicable), and/or allow us

to take additional protective measures such as early termination of all

trades. Further, we enter into legally enforceable master netting agree-

ments which reduce risk by permitting the closeout and netting of trans-

actions with the same counterparty upon the occurrence of certain

events.

The notional amounts presented in Table 33 represent the total con-

tract/notional amount of credit derivatives outstanding and includes both

purchased and written protection. The credit risk amounts are measured

as the net replacement cost in the event the counterparties with con-

tracts in a gain position to us fail to perform under the terms of those

contracts. We use the current mark-to-market value to represent credit

exposure without giving consideration to future mark-to-market

changes. The credit risk amounts take into consideration the effects of

legally enforceable master netting agreements, and on an aggregate

basis have been reduced by cash collateral applied against derivative

assets. The significant increase in credit spreads across nearly all major

credit indices during 2008 drove the increase in counterparty credit risk

for purchased protection. The $1.0 trillion decrease in the contract/

notional value of credit derivatives was driven by our continued efforts to

reduce aggregate positions to minimize market and operational risk. For

information on the performance risk of our written protection credit

derivatives, see Note 4 – Derivatives to the Consolidated Financial

Statements.

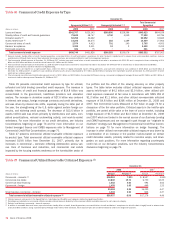

Table 33 Credit Derivatives

December 31

2008 2007

(Dollars in millions) Contract/Notional Credit Risk

(1)

Contract/Notional Credit Risk

(1)

Credit derivatives

Purchased protection:

Credit default swaps

$1,025,876

$11,772 $1,490,641 $6,822

Total return swaps

6,575

1,678 13,551 671

Total purchased protection

1,032,451

13,450 1,504,192 7,493

Written protection:

Credit default swaps

1,000,034

–1,517,305 –

Total return swaps

6,203

–24,884 –

Total written protection

1,006,237

–1,542,189 –

Total credit derivatives

$2,038,688

$13,450 $3,046,381 $7,493

(1) Does not reflect any potential benefit from offsetting exposure to non-credit derivative products with the same counterparties that may be netted upon the occurrence of certain events, thereby reducing the

Corporation’s overall exposure.

78

Bank of America 2008