Bank of America 2008 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

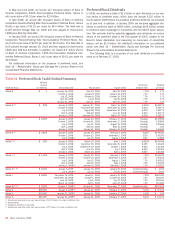

On January 1, 2009, the Corporation acquired Merrill Lynch which

contributed to both our consumer and commercial loans and commit-

ments. Acquired consumer loans consist of residential mortgages, home

equity loans and lines of credit and direct/indirect and other loans.

Commercial loans were comprised of both investment and non-investment

grade loans and include exposures to CMBS, monolines and leveraged

finance. Consistent with other acquisitions, we will incorporate the

acquired assets into our overall credit risk management processes and

enhance disclosures where appropriate.

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with initial

underwriting and continues throughout a borrower’s credit cycle. Stat-

istical techniques in conjunction with experiential judgment are used in all

aspects of portfolio management including underwriting, product pricing,

risk appetite, setting credit limits, operating processes and metrics to

quantify and balance risks and returns. Statistical models are built using

detailed behavioral information from external sources such as credit

bureaus and/or internal historical experience. These models are a

component of our consumer credit risk management process and are

used in part to help determine both new and existing credit decisions,

portfolio management strategies including authorizations and line man-

agement, collection practices and strategies, determination of the allow-

ance for loan and lease losses, and economic capital allocations for

credit risk.

For information on our accounting policies regarding delinquencies,

nonperforming status and charge-offs for the consumer portfolio, see

Note 1 – Summary of Significant Accounting Principles to the Con-

solidated Financial Statements.

Management of Consumer Credit Risk

Concentrations

Consumer credit risk is evaluated and managed with a goal that credit

concentrations do not result in undesirable levels of risk. We review,

measure and manage credit exposure in numerous ways such as by

product and geography in order to achieve the desired mix. Additionally,

credit protection is purchased on certain portions of our portfolio to

enhance our overall risk management position.

The merger with Merrill Lynch will increase our concentrations to cer-

tain products and loan types. These increases are primarily in the resi-

dential mortgage, home equity and direct/indirect portfolios.

Consumer Credit Portfolio

Overall, consumer credit quality indicators deteriorated during 2008 as

our customers were negatively impacted by the slowing economy. Con-

tinued weakness in the housing markets, rising unemployment and

underemployment, and tighter credit conditions resulted in rising credit

risk across all our consumer portfolios. The deterioration in the consumer

credit quality indicators accelerated during the fourth quarter.

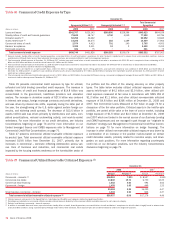

Table 15 presents our consumer loans and leases and our managed

credit card portfolio, and related credit quality information. Loans that

were acquired from Countrywide that were considered impaired were writ-

ten down to fair value at acquisition in accordance with SOP 03-3. Refer

to the SOP 03-3 discussion beginning on page 65 for more information. In

addition to being included in the “Outstandings” column below, these

loans are also shown separately, net of purchase accounting adjust-

ments, for increased transparency in the “SOP 03-3 Portfolio” column.

Table 15 Consumer Loans and Leases

December 31

Outstandings Nonperforming

(1, 2, 3)

Accruing Past Due 90

Days or More

(3, 4)

SOP 03-3

Portfolio

(5)

(Dollars in millions) 2008 2007 2008 2007 2008 2007 2008

Held basis

Residential mortgage

$247,999

$274,949 $7,044 $1,999 $ 372 $ 237 $ 9,949

Home equity

152,547

114,820 2,670 1,340 ––14,163

Discontinued real estate

(6)

19,981

n/a 77 n/a –n/a 18,097

Credit card – domestic

64,128

65,774 n/a n/a 2,197 1,855 n/a

Credit card – foreign

17,146

14,950 n/a n/a 368 272 n/a

Direct/Indirect consumer

(7)

83,436

76,538 26 81,370 745 n/a

Other consumer

(8)

3,442

4,170 91 95 44n/a

Total held

$588,679

$551,201 $9,908 $3,442 $4,311 $3,113 $42,209

Supplemental managed basis data

Credit card – domestic

$154,151

$151,862 n/a n/a $5,033 $4,170 n/a

Credit card – foreign

28,083

31,829 n/a n/a 717 714 n/a

Total credit card – managed

$182,234

$183,691 n/a n/a $5,750 $4,884 n/a

(1) The definition of nonperforming does not include consumer credit card and consumer non-real estate loans and leases. These loans are charged off no later than the end of the month in which the account becomes

180 days past due.

(2) Nonperforming held consumer loans and leases as a percentage of outstanding consumer loans and leases were 1.68 percent (1.81 percent excluding the SOP 03-3 portfolio) and 0.62 percent at December 31, 2008

and 2007.

(3) Balances do not include loans accounted for in accordance with SOP 03-3 even though the customer may be contractually past due. Loans accounted for in accordance with SOP 03-3 were written down to fair value

upon acquisition and accrete interest income over the remaining life of the loan.

(4) Accruing held consumer loans and leases past due 90 days or more as a percentage of outstanding consumer loans and leases were 0.73 percent (0.79 percent excluding the SOP 03-3 portfolio) and 0.57 percent at

December 31, 2008 and 2007.

(5) Represents acquired loans from Countrywide that were considered impaired and written down to fair value at the acquisition date in accordance with SOP 03-3. These amounts are included in the Outstandings column

in this table.

(6) Discontinued real estate includes pay option loans and subprime loans obtained in connection with the acquisition of Countrywide. The Corporation no longer originates these products.

(7) Outstandings include foreign consumer loans of $1.8 billion and $3.4 billion at December 31, 2008 and 2007.

(8) Outstandings include consumer finance loans of $2.6 billion and $3.0 billion, and other foreign consumer loans of $618 million and $829 million at and December 31, 2008 and 2007.

n/a = not applicable

62

Bank of America 2008