Bank of America 2008 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

One ratio that can be used to monitor the stability of our funding

composition and takes into account our deposit balances is the “loan to

domestic deposit” ratio. This ratio reflects the percent of loans and

leases that are funded by domestic core deposits, a relatively stable

funding source. A ratio below 100 percent indicates that our loan portfolio

is completely funded by domestic core deposits. The ratio was 118 per-

cent at December 31, 2008 compared to 127 percent at December 31,

2007.

ALCO determines prudent parameters for wholesale market-based

borrowing and regularly reviews the funding plan for the bank subsidiaries

to ensure compliance with these parameters. The contingency funding

plan for the banking subsidiaries evaluates liquidity over a 12-month

period in a variety of business environment scenarios assuming different

levels of earnings performance and credit ratings as well as public and

investor relations factors. Funding exposure related to our role as liquidity

provider to certain off-balance sheet financing entities is also measured

under a stress scenario. In this analysis, ratings are downgraded such

that the off-balance sheet financing entities are not able to issue

commercial paper and backup facilities that we provide are drawn upon.

In addition, potential draws on credit facilities to issuers with ratings

below a certain level are analyzed to assess potential funding exposure.

The financial market disruptions that began in 2007 continued to

impact the economy and financial services sector during 2008. The

unsecured funding markets remained stressed and experienced short-

term periods of illiquidity during the second half of the year as prime

money market fund managers remained focused on redemptions and

increased their portfolio composition to shorter and more liquid

government-sponsored assets. As a result of the disruptions, the Corpo-

ration shifted to issuing FDIC guaranteed TLGP debt in the fourth quarter

to generate material funding in the capital markets.

Our primary banking subsidiary, Bank of America, N.A., is maintaining

historically high levels of cash with the Federal Reserve each day as well

as ensuring an unused portion of high quality collateral is available to

generate cash at all times. Further, Bank of America, N.A. maintains addi-

tional collateral that could utilize the Federal Reserve’s balance sheet

through the Discount Window in the event of a deep and prolonged shock

to funding markets.

The Corporation also utilizes overnight repo markets. During the most

severe liquidity disruptions in the overnight repo markets we did not expe-

rience liquidity issues. Nonetheless, we have recently reduced overnight

funding exposure at both the parent and banking subsidiary levels.

In addition, liquidity for ABS disappeared and issuance spreads rose

to historic highs, negatively impacting our credit card securitization pro-

grams. If these conditions persist it could adversely affect our ability to

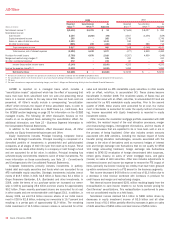

access these markets at favorable terms in the future. Approximately

$20.7 billion of debt issued through our U.S. credit card securitizations

trust will mature in the upcoming 12 months. The U.S. credit card

securitization trust had approximately $88.6 billion and $84.8 billion in

outstanding securitized loans at December 31, 2008 and 2007 and the

trust excess spread was 5.64 percent and 6.64 percent. If the 3-month

average excess spread declines below 4.50 percent, the residual excess

cash flows that are typically returned to the Corporation will be held by a

trustee up to certain levels as additional credit enhancements to the

investors. If the excess spread were to decline to zero percent, the trust

would enter into early amortization, repayment of the debt issued through

our credit card securitizations would be accelerated and the Corporation

will have to fund all future credit card loan advances on-balance sheet.

This could adversely impact the Corporation’s liquidity and capital.

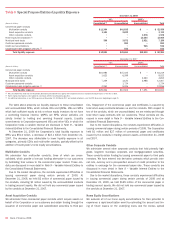

As specifically permitted by the terms of the transaction documents,

and in an effort to address the recent decline in the excess spread due to

the performance of the underlying credit card receivables in the U.S.

credit card securitization trust, an additional subordinated security total-

ing approximately $8.0 billion will be issued by the trust to the Corpo-

ration in the first quarter of 2009. This security will provide additional

credit enhancement to the trust and its investors. In addition, upon com-

pletion of requirements set forth in transaction documents, we plan to

allocate a percentage of new receivables into the trust that, when col-

lected, will be applied to finance charges, which is expected to increase

the yield in the trust. These actions are not expected to have a significant

impact on the Corporation’s results of operations. If these actions had

occurred on December 31, 2008, the impact would have increased our

Tier 1 risk-weighted assets by approximately $75 billion or six percent.

While market conditions have been challenging, we experienced a

significant increase in deposits as we benefited from a consumer and

business flight-to-safety in the second half of 2008. We have also taken

direct actions to enhance our liquidity position during 2008 including

receiving cash proceeds of $34.7 billion on the issuance of preferred

stock, $9.9 billion of common stock, net of underwriting expenses, $8.5

billion of senior notes, $1.0 billion of Eurodollar floating rate notes and

$15.6 billion of debt issued under the TLGP by the parent company.

Included in the $34.7 billion of cash proceeds on the issuance of pre-

ferred stock is $15.0 billion related to the Series N Preferred Stock that

was issued in connection with the TARP Capital Purchase Program, which

is discussed further below. Furthermore, in January 2009, the Corporation

issued Series Q Preferred Stock for an additional $10.0 billion of cash

proceeds in connection with the TARP Capital Purchase Program.

In addition, in January 2009, the U.S. government agreed to assist in

the Merrill Lynch acquisition by making a further investment in the Corpo-

ration of $20.0 billion in preferred stock. Further, the U.S. government

has agreed in principle to provide protection against the possibility of

unusually large losses on $118.0 billion in selected capital markets

exposure, primarily from the former Merrill Lynch portfolio. As a fee for

this arrangement, we expect to issue to the U.S. Treasury and FDIC a

total of $4.0 billion of a new class of preferred stock and to issue war-

rants to acquire 30.1 million shares of Bank of America common stock.

For more information, see the Recent Events section on page 22.

Lastly, Bank of America, N.A. issued $10.0 billion of senior unsecured

bank notes, of which $6.0 billion included an extendible feature, $4.3 bil-

lion of debt under the TLGP, and $43.1 billion in short term bank notes.

Also, several funding programs have been made available through the

Federal Reserve which are more fully described in Regulatory Initiatives

on page 20.

A majority of the long-term liquidity obtained by the Corporation under

the TLGP since the announcement of the Merrill Lynch acquisition was

completed in preparation for the funding needs of the combined orga-

nizations. We will continue to manage the liquidity position of the com-

bined company through our ALM activities. Merrill Lynch had long-term

debt outstanding with a fair value of $189.4 billion at acquisition. As the

organizations integrate, the Corporation intends to utilize the capital

markets to maintain its “Time to Required Funding” within the approved

ALCO guidelines.

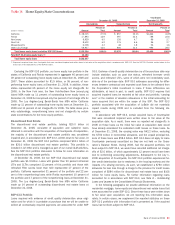

Regulatory Capital

At December 31, 2008, the Corporation operated its banking activities

primarily under three charters: Bank of America, N.A., FIA Card Services,

N.A., and Countrywide Bank, FSB. Effective October 17, 2008, LaSalle

Bank, N.A. merged with and into Bank of America, N.A., with Bank of

America, N.A. as the surviving entity. As a regulated financial services

company, we are governed by certain regulatory capital requirements. At

December 31, 2008 and 2007, the Corporation, Bank of America, N.A.,

and FIA Card Services, N.A., were classified as “well-capitalized” for regu-

latory purposes, the highest classification. Effective July 1, 2008, we

Bank of America 2008

57