Bank of America 2008 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

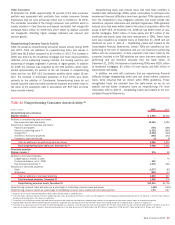

Counterparty Credit Risk Valuation Adjustments

We record a counterparty credit risk valuation adjustment on our expected

exposure related to derivative assets and liabilities, including our credit

default protection purchased, in order to properly reflect the credit quality

of the counterparty in accordance with SFAS 157. In determining the

expected exposure, we consider collateral held and legally enforceable

master netting agreements that mitigate our credit exposure to each

counterparty. The amount of counterparty credit risk valuation adjust-

ments at any point of time is dependent on the value of the derivative

contract, collateral, and credit worthiness of the counterparty.

During 2008, valuation adjustments related to derivative assets of

$3.2 billion were recognized as trading account losses for counterparty

credit risk, including $1.1 billion of losses related to insured super senior

CDOs and $537 million of losses related to our structured credit trading

business. The losses were driven by increases in the value of the

derivative contracts resulting primarily from spread widening, market vola-

tility and credit deterioration related to the underlying counterparties. At

December 31, 2008, the cumulative counterparty credit risk valuation

adjustment that was netted against the derivative asset balance was

$4.0 billion. For information on our monoline counterparty credit risk see

the discussion on page 76, CDO-related counterparty credit risk see the

CMAS discussion on page 40 and for more information on the VAR

related to our counterparty credit risk see the Trading Risk Management

discussion on page 85.

In addition, the fair value of our derivative liabilities is adjusted to

reflect the impact of the Corporation’s credit quality. During 2008, valu-

ation adjustments of $364 million were recognized as trading account

profits for changes in the Corporation’s credit risk driven by credit spread

widening. At December 31, 2008, the Corporation’s cumulative credit risk

valuation adjustment that was netted against the derivative liabilities

balance was $573 million.

In light of recent market events, banking regulators have been working

with the industry to organize a central clearinghouse for credit derivative

trading, similar to existing clearinghouses for interest rate derivatives. It

is expected that a central clearinghouse for credit derivatives would

reduce the risk of counterparty default, similar to the reduction achieved

through the interest rate derivative clearinghouse, primarily through the

guaranteeing of trades in the event that a member fails. We continue to

participate in these industry initiatives.

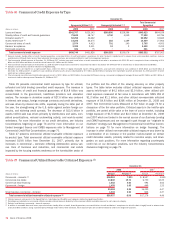

Foreign Portfolio

Our foreign credit and trading portfolio is subject to country risk. We

define country risk as the risk of loss from unfavorable economic and

political conditions, currency fluctuations, social instability and changes

in government policies. A risk management framework is in place to

measure, monitor and manage foreign risk and exposures. Management

oversight of country risk including cross-border risk is provided by the

Country Risk Committee, a subcommittee of the CRC.

Table 34 sets forth total foreign exposure broken out by region at

December 31, 2008 and 2007. Foreign exposure includes credit

exposure net of local liabilities, securities, and other investments domi-

ciled in countries other than the U.S. Total foreign exposure can be

adjusted for externally guaranteed outstandings and certain collateral

types. Exposures which are assigned external guarantees are reported

under the country of the guarantor. Exposures with tangible collateral are

reflected in the country where the collateral is held. For securities

received, other than cross-border resale agreements, outstandings are

assigned to the domicile of the issuer of the securities. Resale agree-

ments are generally presented based on the domicile of the counterparty

consistent with FFIEC reporting requirements.

Our total foreign exposure was $131.1 billion at December 31, 2008,

a decrease of $7.0 billion from December 31, 2007. Our foreign

exposure remained concentrated in Europe, which accounted for $66.5

billion, or 51 percent, of total foreign exposure. The European exposure

was mostly in Western Europe and was distributed across a variety of

industries with approximately 58 percent concentrated in the commercial

sector and approximately 17 percent in the banking sector. The decline of

$8.3 billion in Europe was driven by lower cross-border derivatives

assets, and securities and other investment exposures.

Asia Pacific was our second largest foreign exposure at $39.8 billion,

or 30 percent. The decline in Asia Pacific was primarily driven by lower

cross-border exposures in Japan and Australia offset in part by the net

$3.3 billion increased equity investment in CCB and higher exposure in

India. Latin America accounted for $11.4 billion, or nine percent, of total

foreign exposure. For more information on our Asia Pacific and Latin

America exposures, see the discussion on the foreign exposure to

selected countries defined as emerging markets on page 80.

Table 34 Regional Foreign Exposure (1, 2, 3)

December 31

(Dollars in millions) 2008 2007

Europe

$ 66,472

$ 74,725

Asia Pacific

39,774

42,081

Latin America

11,378

10,944

Middle East and Africa

2,456

1,951

Other

10,988

8,361

Total regional foreign exposure

$131,068

$138,062

(1) The balances above exclude local funding or liabilities which are subtracted from local exposures as allowed by the FFIEC.

(2) Exposures have been reduced by $19.6 billion and $6.3 billion at December 31, 2008 and 2007. Such amounts represent the cash applied as collateral to derivative assets.

(3) Generally, resale agreements are presented based on the domicile of the counterparty consistent with FFIEC reporting requirements. Cross-border resale agreements where the underlying securities are U.S. Treasury

securities, in which case the domicile is the U.S., are excluded from this presentation.

Bank of America 2008

79