Bank of America 2008 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

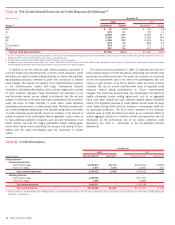

Mortgage Risk

Mortgage risk represents exposures to changes in the value of mortgage-

related instruments. The values of these instruments are sensitive to

prepayment rates, mortgage rates, agency debt ratings, default, market

liquidity, other interest rates and interest rate volatility. Our exposure to

these instruments takes several forms. First, we trade and engage in

market-making activities in a variety of mortgage securities including

whole loans, pass-through certificates, commercial mortgages, and

collateralized mortgage obligations including CDOs using mortgages as

underlying collateral. Second, we originate a variety of mortgage-backed

securities which involves the accumulation of mortgage-related loans in

anticipation of eventual securitization. Third, we may hold positions in

mortgage securities and residential mortgage loans as part of the ALM

portfolio. Fourth, we create MSRs as part of our mortgage origination

activities. See Note 1 – Summary of Significant Accounting Principles and

Note 21 – Mortgage Servicing Rights to the Consolidated Financial

Statements for additional information on MSRs. Hedging instruments

used to mitigate this risk include options, futures, forwards, swaps,

swaptions and securities.

Equity Market Risk

Equity market risk represents exposures to securities that represent an

ownership interest in a corporation in the form of domestic and foreign

common stock or other equity-linked instruments. Instruments that would

lead to this exposure include, but are not limited to, the following: com-

mon stock, exchange traded funds, American Depositary Receipts (ADRs),

convertible bonds, listed equity options (puts and calls), over-the-counter

equity options, equity total return swaps, equity index futures and other

equity derivative products. Hedging instruments used to mitigate this risk

include options, futures, swaps, convertible bonds and cash positions.

Commodity Risk

Commodity risk represents exposures to instruments traded in the petro-

leum, natural gas, power, and metals markets. These instruments consist

primarily of futures, forwards, swaps and options. Hedging instruments

used to mitigate this risk include options, futures and swaps in the same

or similar commodity product, as well as cash positions.

Issuer Credit Risk

Issuer credit risk represents exposures to changes in the creditworthi-

ness of individual issuers or groups of issuers. Our portfolio is exposed to

issuer credit risk where the value of an asset may be adversely impacted

by changes in the levels of credit spreads, by credit migration, or by

defaults. Hedging instruments used to mitigate this risk include bonds,

CDS and other credit fixed income instruments.

Market Liquidity Risk

Market liquidity risk represents the risk that expected market activity

changes dramatically and in certain cases may even cease to exist. This

exposes us to the risk that we will not be able to transact in an orderly

manner and may impact our results. This impact could further be

exacerbated if expected hedging or pricing correlations are impacted by

the disproportionate demand or lack of demand for certain instruments.

We utilize various risk mitigating techniques as discussed in more detail

in Trading Risk Management.

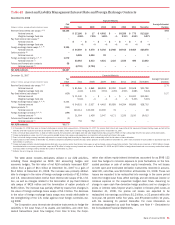

Trading Risk Management

Trading-related revenues represent the amount earned from trading posi-

tions, including market-based net interest income, which are taken in a

diverse range of financial instruments and markets. Trading account

assets and liabilities and derivative positions are reported at fair value.

For more information on fair value, see Note 19 – Fair Value Disclosures

to the Consolidated Financial Statements and Complex Accounting Esti-

mates beginning on page 93. Trading-related revenues can be volatile and

are largely driven by general market conditions and customer demand.

Trading-related revenues are dependent on the volume and type of trans-

actions, the level of risk assumed, and the volatility of price and rate

movements at any given time within the ever-changing market environ-

ment.

The GRC, chaired by the Global Markets Risk Executive, has been

designated by ALCO as the primary governance authority for Global Mar-

kets Risk Management including trading risk management. The GRC’s

focus is to take a forward-looking view of the primary credit and market

risks impacting CMAS and prioritize those that need a proactive risk miti-

gation strategy.

At the GRC meetings, the committee considers significant daily rev-

enues and losses by business along with an explanation of the primary

driver of the revenue or loss. Thresholds are established for each of our

businesses in order to determine if the revenue or loss is considered to

be significant for that business. If any of the thresholds are exceeded, an

explanation of the variance is made to the GRC. The thresholds are

developed in coordination with the respective risk managers to highlight

those revenues or losses which exceed what is considered to be normal

daily income statement volatility.

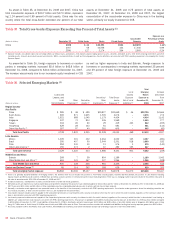

The following histogram is a graphic depiction of trading volatility and

illustrates the daily level of trading-related revenue for the 12 months

ended December 31, 2008 as compared with the 12 months ended

December 31, 2007. During the 12 months ended December 31, 2008,

positive trading-related revenue was recorded for 66 percent of the trad-

ing days of which 17 percent were daily trading gains of over $50 million,

25 percent of the trading days had losses greater than $10 million, and

the largest loss was $173 million. This can be compared to the 12

months ended December 31, 2007, where excluding any discrete write-

downs on CDOs positive trading-related revenue was recorded for 71

percent of the trading days of which five percent were daily trading gains

of over $50 million, 21 percent of the trading days had losses greater

than $10 million, and the largest loss was $159 million. The increase in

daily trading gains of over $50 million and losses of over $10 million in

2008 compared to 2007 was driven by the increased volatility that was

experienced in the markets during the full year of 2008 while 2007

experienced increased volatility only during the second half of the year.

Bank of America 2008

85