Bank of America 2008 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

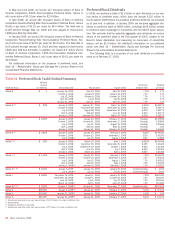

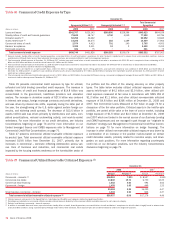

Table 18 Home Equity State Concentrations

December 31, 2008

Year Ended

December 31, 2008

Outstandings Nonperforming Net Charge-offs

(Dollars in millions) Amount

Percent of

Total Amount

Percent of

Total Amount

Percent of

Total

California $ 38,015 27.5% $ 857 32.1% $1,464 41.9%

Florida 17,893 12.9 597 22.4 788 22.6

New Jersey 8,929 6.5 126 4.7 96 2.7

New York 8,602 6.2 176 6.6 96 2.7

Massachusetts 6,008 4.3 48 1.8 56 1.6

Other U.S./Foreign 58,937 42.6 866 32.4 996 28.5

Total home equity loans (excluding SOP 03-3 loans)

$138,384 100.0% $2,670 100.0% $3,496 100.0%

Total SOP 03-3 home equity loans (1)

14,163

Total home equity loans

$152,547

(1) Represents acquired loans from Countrywide that were considered impaired and written down to fair value at the acquisition date in accordance with SOP 03-3. See the SOP 03-3 Portfolio section below for the

discussion of the characteristics of the SOP 03-3 loans.

Excluding the SOP 03-3 portfolio, our home equity loan portfolio in the

states of California and Florida represented in aggregate 40 percent and

39 percent of outstanding home equity loans at December 31, 2008 and

2007. These states accounted for $1.5 billion, or 55 percent, of non-

performing home equity loans at December 31, 2008. In addition, these

states represented 65 percent of the home equity net charge-offs for

2008. In the New York area, the New York-Northern New Jersey-Long

Island MSA made up 11 percent of outstanding home equity loans at

December 31, 2008 but comprised only five percent of net charge offs for

2008. The Los Angeles-Long Beach-Santa Ana MSA within California

made up 11 percent of outstanding home equity loans at December 31,

2008 and 11 percent of net charge-offs for 2008. The table above pres-

ents outstandings, nonperforming loans and net charge-offs by certain

state concentrations for the home equity portfolio.

Discontinued Real Estate

The discontinued real estate portfolio, totaling $20.0 billion at

December 31, 2008, consisted of pay-option and subprime loans

obtained in connection with the acquisition of Countrywide. At acquisition,

the majority of the discontinued real estate portfolio was considered

impaired and, in accordance with SOP 03-3, written down to fair value. At

December 31, 2008 the SOP 03-3 portfolio comprised $18.1 billion of

the $20.0 billion discontinued real estate portfolio. This portfolio is

included in All Other and is managed as part of our overall ALM activities.

See the SOP 03-3 portfolio discussion to follow for more information on

the discontinued real estate portfolio.

At December 31, 2008, the non SOP 03-3 discontinued real estate

portfolio was $1.9 billion. Loans with greater than 90 percent refreshed

LTVs and CLTVs comprised 13 percent of this portfolio and those with

refreshed FICO scores lower than 620 represented 17 percent of the

portfolio. California represented 31 percent of the portfolio and 22 per-

cent of the nonperforming loans while Florida represented 10 percent of

the portfolio and 17 percent of the nonperforming loans at December 31,

2008. The Los Angeles-Long Beach-Santa Ana MSA within California

made up 14 percent of outstanding discontinued real estate loans at

December 31, 2008.

SOP 03-3 Portfolio

Loans acquired with evidence of credit quality deterioration since origi-

nation and for which it is probable at purchase that we will be unable to

collect all contractually required payments are accounted for under SOP

03-3. Evidence of credit quality deterioration as of the purchase date may

include statistics such as past due status, refreshed borrower credit

scores, and refreshed LTVs, some of which were not immediately avail-

able as of the purchase date. SOP 03-3 addresses accounting for differ-

ences between contractual and expected cash flows to be collected from

the Corporation’s initial investment in loans if those differences are

attributable, at least in part, to credit quality. SOP 03-3 requires that

acquired impaired loans be recorded at fair value and prohibits “carrying

over” or the creation of valuation allowances in the initial accounting for

loans acquired that are within the scope of this SOP. The SOP 03-3

portfolio associated with the acquisition of LaSalle did not materially

impact results during 2008 and is excluded from the following dis-

cussion.

In accordance with SOP 03-3, certain acquired loans of Countrywide

that were considered impaired were written down to fair value at the

acquisition date. As a result, there were no reported net charge-offs in

2008 on these loans as the initial fair value at acquisition date would

have already considered the estimated credit losses on these loans. As

of December 31, 2008, the carrying value was $42.2 billion, excluding

the $750 million in incremental allowance, and the unpaid principal bal-

ance of these loans was $55.4 billion. SOP 03-3 does not apply to loans

Countrywide previously securitized as they are not held on the Corpo-

ration’s Balance Sheet. During 2008, had the acquired portfolios not

been subject to SOP 03-3, we would have recorded additional net charge-

offs of $3.6 billion, of which approximately 13 percent would have been

due to conforming accounting adjustments. Subsequent to the July 1,

2008 acquisition of Countrywide, the SOP 03-3 portfolio experienced fur-

ther credit deterioration due to weakness in the housing markets and the

impacts of a slowing economy. As such, we established a $750 million

allowance for loan loss through a charge to the provision for credit losses

comprised of $584 million for discontinued real estate loans and $166

million for home equity loans. For further information regarding loans

accounted for in accordance with SOP 03-3, see Note 6 – Outstanding

Loans and Leases to the Consolidated Financial Statements.

In the following paragraphs we provide additional information on the

residential mortgage, home equity and discontinued real estate loans that

were accounted for under SOP 03-3. Since these loans were written down

to fair value upon acquisition, we are reporting this information sepa-

rately. In certain cases, we supplement the reported statistics on these

SOP 03-3 portfolios with information that is presented as if the acquired

loans had not been subject to SOP 03-3.

Bank of America 2008

65