Bank of America 2008 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

not believe that the AFS debt and marketable equity securities that are in

an unrealized loss position at December 31, 2008 are other-than-

temporarily impaired.

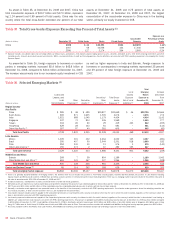

Residential Mortgage Portfolio

At December 31, 2008, residential mortgages were $248.0 billion com-

pared to $274.9 billion at December 31, 2007. This decrease was attrib-

utable to the repositioning of our ALM portfolio, driven by market liquidity,

as we increased the level of mortgage-backed securities relative to loans,

partially offset by the acquisition of Countrywide which added $26.8 bil-

lion of residential mortgages. We securitized $26.1 billion and $5.5 bil-

lion of residential mortgage loans into mortgage-backed securities which

we retained during 2008 and 2007. During 2008, we purchased $405

million of residential mortgages related to ALM activities compared to

purchases of $22.5 billion during 2007. We also added $27.3 billion and

$66.3 billion of originated residential mortgages and we sold $30.7 bil-

lion and $34.0 billion of residential mortgages during 2008 and 2007. Of

these sales, $22.9 billion and $23.7 billion were originated residential

mortgages, resulting in gains of $392 million and $187 million. The

remaining $7.8 billion and $10.4 billion were related to service by others

loan sales, resulting in gains of $104 million and $84 million. We

received paydowns of $26.3 billion and $28.2 billion in 2008 and 2007.

In addition to the residential mortgage portfolio we incorporated the

discontinued real estate portfolio that was acquired in connection with

the Countrywide acquisition into our ALM activities. This portfolio’s bal-

ance was $20.0 billion at December 31, 2008.

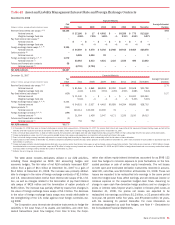

Interest Rate and Foreign Exchange Derivative

Contracts

Interest rate and foreign exchange derivative contracts are utilized in our

ALM activities and serve as an efficient tool to mitigate our interest rate

and foreign exchange risk. We use derivatives to hedge the variability in

cash flows or changes in fair value on our balance sheet due to interest

rate and foreign exchange components. For additional information on our

hedging activities, see Note 4 – Derivatives to the Consolidated Financial

Statements.

Our interest rate contracts are generally non-leveraged generic interest

rate and foreign exchange basis swaps, options, futures and forwards. In

addition, we use foreign exchange contracts, including cross-currency

interest rate swaps and foreign currency forward contracts, to mitigate the

foreign exchange risk associated with foreign currency-denominated

assets and liabilities. Table 42 reflects the notional amounts, fair value,

weighted average receive fixed and pay fixed rates, expected maturity,

and estimated duration of our open ALM derivatives at December 31,

2008 and 2007. These amounts do not include our derivative hedges on

our net investments in consolidated foreign operations.

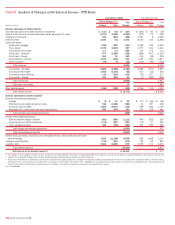

Changes to the composition of our derivatives portfolio during 2008

reflect actions taken for interest rate and foreign exchange rate risk

management. The decisions to reposition our derivative portfolio are

based upon the current assessment of economic and financial conditions

including the interest rate environment, balance sheet composition and

trends, and the relative mix of our cash and derivative positions. The

notional amount of our option positions decreased from $140.1 billion at

December 31, 2007 to $5.0 billion at December 31, 2008. Changes in

the levels of the option positions was driven by maturities of $115.1 bil-

lion in purchased caps along with the termination of $20.0 billion in sold

floors. Our interest rate swap positions (including foreign exchange con-

tracts) were a net receive fixed position of $50.3 billion at December 31,

2008 compared to a net receive fixed position of $101.9 billion on

December 31, 2007. Changes in the notional levels of our interest rate

swap position were driven by the net termination and maturity of $54.8

billion in U.S. dollar-denominated receive fixed swaps, the termination of

$11.3 billion in pay fixed swaps, and the net termination of $8.1 billion in

foreign denominated receive fixed swaps. The notional amount of our

foreign exchange basis swaps was $54.6 billion and $54.5 billion at

December 31, 2008 and 2007.

90

Bank of America 2008