Bank of America 2008 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

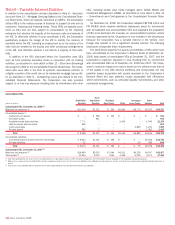

value and is insufficient to cover the vehicle’s obligation to the Corpo-

ration under the credit default swaps.

Asset acquisition vehicles acquire financial instruments, typically

loans, at the direction of a single customer and obtain funding through

the issuance of structured notes to the Corporation. At the time the

vehicle acquires an asset, the Corporation enters into a total return swap

with the customer such that the economic returns of the asset are

passed through to the customer. As a result, the Corporation does not

consolidate the vehicles. The Corporation is exposed to counterparty

credit risk if the asset declines in value and the customer defaults on its

obligation to the Corporation under the total return swap. The Corpo-

ration’s risk may be mitigated by collateral or other arrangements.

Other Vehicles

Other vehicles include loan and other investment vehicles as well as

other corporate conduits that were established on behalf of the Corpo-

ration or customers who wish to obtain market or credit exposure to a

specific company or financial instrument.

Loan and other investment vehicles at December 31, 2008 and 2007

consisted primarily of securitization vehicles, including term securitization

vehicles that did not meet QSPE status, as well as managed investment

vehicles that invest in financial assets, primarily debt securities and

loans. The Corporation determines whether it is the primary beneficiary of

and must consolidate a loan or other investment vehicle based principally

on a determination as to which party is expected to absorb a majority of

the credit risk or market risk created by the assets of the vehicle. Typi-

cally, the party holding subordinated or residual interests in a vehicle will

absorb a majority of the risk. Investors in consolidated loan and other

investment vehicles have no recourse to the general credit of the Corpo-

ration as their investments are repaid solely from the assets of the

vehicle.

Other corporate conduits at December 31, 2008 and 2007 are

commercial paper conduits, which hold primarily high-grade, long-term

municipal, corporate and mortgage-backed securities. The assets held by

these other conduits have a weighted average remaining life of approx-

imately 2.5 years at December 31, 2008. Substantially all of the secu-

rities are rated AAA or AA and some of the bonds benefit from insurance

provided by monolines. The conduits obtain funding by issuing commer-

cial paper to third party investors. At December 31, 2008, the weighted

average maturity of the commercial paper was 15 days. We have entered

into derivative contracts which provide interest rate, currency and a

pre-specified amount of credit protection to the conduits in exchange for

the commercial paper rate. In addition, the Corporation may be obligated

to purchase assets from the conduits if the assets or insurers are down-

graded. If an asset’s rating declines below a certain investment quality as

evidenced by its credit rating or defaults, the Corporation is no longer

exposed to the risk of loss.

During 2008, three monoline insurers were downgraded by the rating

agencies which resulted in the mandatory sale of $1.5 billion of insured

assets out of the conduits. Due to illiquidity in the financial markets at

the time of the sales, the Corporation purchased a majority of these

assets. After subsequent sales to third parties, $1.1 billion of these

assets remain on the Consolidated Balance Sheet and are recorded

within trading account assets at December 31, 2008. The conduits are

QSPEs and, as such, are not subject to consolidation by the Corporation.

In the event that the Corporation is unable to remarket the conduits’

commercial paper such that they no longer qualify as QSPEs, the Corpo-

ration would consolidate the conduits which may have an adverse impact

on the fair value of the related derivative contracts. Derivative activity

related to the other corporate conduits is carried at fair value with

changes in fair value recorded in trading account profits (losses).

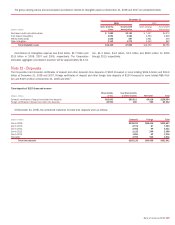

Note 10 – Goodwill and Intangible Assets

The following table presents goodwill at December 31, 2008 and 2007,

which includes approximately $4.4 billion of goodwill related to the

acquisition of Countrywide. For more information on the Countrywide

acquisition, see Note 2 – Merger and Restructuring Activities to the

Consolidated Financial Statements.

December 31

(Dollars in millions) 2008 2007

Global Consumer and Small Business Banking

$44,873

$40,340

Global Corporate and Investment Banking

29,570

29,648

Global Wealth and Investment Management

6,503

6,451

All Other

988

1,091

Total goodwill

$81,934

$77,530

The Corporation performed its annual goodwill impairment test as of

June 30, 2008 which indicated some stress in certain reporting units. As

a result of this test and considering the overall market displacement, an

additional impairment analysis was completed at year-end. The Corpo-

ration evaluated the fair value of its reporting units using a combination

of the market and income approach, using a range of valuations to

determine the fair value of each reporting unit. In performing the updated

goodwill impairment analysis the Mortgage, Home Equity and Insurance

Services business failed the first step analysis (i.e., carrying value

exceeded its fair value) and therefore the second step analysis was per-

formed (i.e., comparing the implied fair value of the reporting unit’s

goodwill with the carrying amount of that goodwill). In addition, although

not required, to further substantiate the value of the Corporation’s good-

will balance the second step analysis described above was performed for

the Card Services business as well. As a result of the tests, no goodwill

losses were recognized for 2008. For more information on goodwill

impairment testing, see the Goodwill and Intangible Assets section of

Note 1 – Summary of Significant Accounting Principles to the Con-

solidated Financial Statements.

148

Bank of America 2008