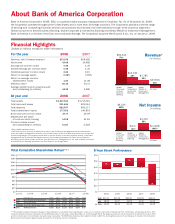

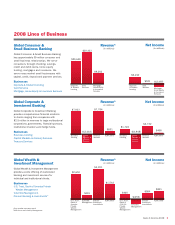

Bank of America 2008 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

of rising credit costs. The opportunity

we have in 2009 is to increase cus-

tomer loyalty for the future as we help

customers work through hard economic

times. In 2008, we modified nearly

850,000 credit card loans, whether

by lowering interest rates, reducing

monthly payments or eliminating fees.

We also continue to refer customers

to debt management programs. We

believe our approach to helping our

customers manage through hard times

will pay off in retention and growth

when the economy improves.

Last year, I wrote here for the first

time about our $20 billion environ-

mental initiative. We believe there

is tremendous growth potential for

companies that stake out a leadership

position in alternative energy produc-

tion and conservation. To that point,

we signed an agreement with a green-

technology company that is helping us

reduce our energy consumption in all

our banking centers across the country

by as much as 50 percent. And we’re

supporting ventures that we believe will

lead to abundant and renewable energy

sources in the future. For example,

we co-led an initial public offering for

Ocean Power Technologies, a company

that is engineering new technologies

that will enable utilities to harvest and

transport energy from ocean waves.

We also are continuing to support our

local communities through both commu-

nity development lending and investing,

and philanthropic programs like our

Neighborhood Excellence Initiative (NEI).

Through NEI, now in its sixth year, we

have provided support to hundreds of

neighborhood nonprofits, anchor institu-

tions and community leaders through

unrestricted operating grants and lead-

ership development programs.

Given the economic environment

and the impact that the recession is

having in neighborhoods across the

country, we are working more closely

than ever with community leaders to

identify the most critical needs and

gaps in local assistance programs and

ensure that resources are flowing to

individuals and families that have been

especially hard-hit. For example, in

2008 we announced a Neighborhood

Preservation Initiative offering grants

and low-interest loans to nonprofit

community organizations that will help

borrowers stay in their homes through

financial education programs and other

outreach activities.

Most important, we are not backing

down from the goals we put in place last

year to lend and invest $1.5 trillion over

10 years in low- and moderate-income

and minority neighborhoods, and to give

at least $2 billion over 10 years through

the Bank of America Charitable Founda-

tion. We believe it is critically important

Many paths to growth

One of the most important ideas on

which we’ve built this company is that

diversity creates strength. Diversity of

businesses, revenue streams, risks,

ideas, perspectives and people brings

strength to an organization that is hard

to come by any other way. The same is

true about growth opportunities. The

more paths to growth we can pursue

simultaneously and in coordination with

one another, the more likely we’ll be to

reach our goals.

Earlier, I discussed our prospects

in home lending, wealth management

and corporate and investment banking.

We also are well-positioned to generate

growth in our other two main business

lines, Deposits & Student Lending and

Card Services.

We already serve half of all Ameri-

can households, and we’re benefitting

from a flight to safety, a powerful brand

and rising customer satisfaction. In

2008, average retail core deposits

(excluding Countrywide) grew by nearly

$54 billion or 11.2 percent. Custom-

ers opened nearly 5 million net new

checking and savings accounts. For

the year, average balances in CDs and

IRAs were up nearly 16 percent, and

balances in money market savings

accounts were up more than 18 percent.

In Card Services, we are facing

incredibly stiff headwinds in the form

We are well-capitalized, deposit-funded

and extremely liquid. We have one of the largest,

broadest customer bases in the industry.

Bank of America 2008 7