Bank of America 2008 Annual Report Download - page 178

Download and view the complete annual report

Please find page 178 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

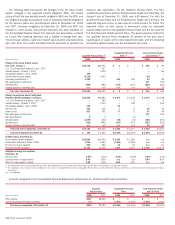

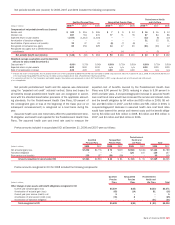

Structured Reverse Repurchase Agreements and Long-term

Deposits

The fair values of structured reverse repurchase agreements and long-

term deposits are determined using quantitative models, including dis-

counted cash flow models that require the use of multiple market inputs

including interest rates and spreads to generate continuous yield or pric-

ing curves and volatility factors. The majority of market inputs are actively

quoted and can be validated through external sources, including brokers,

market transactions and third-party pricing services. The Corporation does

incorporate, consistent with the requirements of SFAS 157, within its fair

value measurements of long-term deposits the net credit differential

between the counterparty credit risk and our own credit risk. The value of

the net credit differential is determined by reference to existing direct

market reference costs of credit, or where direct references are not avail-

able, a proxy is applied consistent with direct references for other

counterparties that are similar in credit risk.

Trading Account Assets and Liabilities and Available-for-Sale Debt

Securities

The fair values of trading account assets and liabilities are primarily

based on actively traded markets where prices are based on either direct

market quotes or observed transactions. The fair values of AFS debt

securities are generally based on quoted market prices or market prices

for similar assets. Liquidity is a significant factor in the determination of

the fair values of trading account assets or liabilities and AFS debt secu-

rities. Market price quotes may not be readily available for some posi-

tions, or positions within a market sector where trading activity has

slowed significantly or ceased such as certain CDO positions and other

ABS. Some of these instruments are valued using a net asset value

approach, which considers the value of the underlying securities. Under-

lying assets are valued using external pricing services, where available, or

matrix pricing based on the vintages and ratings. Situations of illiquidity

generally are triggered by the market’s perception of credit uncertainty

regarding a single company or a specific market sector. In these

instances, fair value is determined based on limited available market

information and other factors, principally from reviewing the issuer’s

financial statements and changes in credit ratings made by one or more

rating agencies.

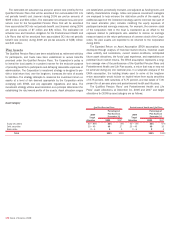

Derivative Assets and Liabilities

The fair values of derivative assets and liabilities traded in the

over-the-counter market are determined using quantitative models that

require the use of multiple market inputs including interest rates, prices,

and indices to generate continuous yield or pricing curves and volatility

factors, which are used to value the position. The majority of market

inputs are actively quoted and can be validated through external sources,

including brokers, market transactions and third-party pricing services.

Estimation risk is greater for derivative asset and liability positions that

are either option-based or have longer maturity dates where observable

market inputs are less readily available or are unobservable, in which

case, quantitative-based extrapolations of rate, price or index scenarios

are used in determining fair values. The fair values of derivative assets

and liabilities include adjustments for market liquidity, counterparty credit

quality and other deal specific factors, where appropriate. Consistent with

the way the Corporation fair values long-term deposits as previously dis-

cussed, the Corporation incorporates, within its fair value measurements

of over-the-counter derivatives, the net credit differential between the

counterparty credit risk and our own credit risk. An estimate of severity of

loss is also used in the determination of fair value, primarily based

on historical experience, adjusted for recent name specific expectations.

Mortgage Servicing Rights

The fair values of MSRs are determined using models which depend on

estimates of prepayment rates, the resultant weighted average lives of

the MSRs and the OAS levels. For more information on MSRs, see Note

21 – Mortgage Servicing Rights to the Consolidated Financial Statements.

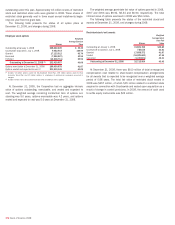

Loans Held-for-Sale

The fair values of LHFS are based on quoted market prices, where avail-

able, or are determined by discounting estimated cash flows using inter-

est rates approximating the Corporation’s current origination rates for

similar loans adjusted to reflect the inherent credit risk.

Other Assets

The Corporation fair values certain other assets including AFS equity

securities and certain retained residual interests in securitization

vehicles. The fair values of AFS equity securities are generally based on

quoted market prices or market prices for similar assets. However,

non-public investments are initially valued at transaction price and sub-

sequently adjusted when evidence is available to support such adjust-

ments. Retained residual interests in securitization vehicles are based on

certain observable inputs such as interest rates and credit spreads, as

well as unobservable inputs such as estimated net charge-off and pay-

ment rates.

Asset-backed Secured Financings

The fair values of asset-backed secured financings are based on external

broker bids, where available, or are determined by discounting estimated

cash flows using interest rates approximating the Corporation’s current

origination rates for similar loans adjusted to reflect the inherent credit

risk.

176

Bank of America 2008