Philips 2010 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

2 Vision 2015 - our strategic focus 2 - 2

14 Annual Report 2010

Population growth, aging, higher healthcare aspirations and

lifestyle-related diseases mean that healthcare costs will

become unsustainable

Increased welfare and changing lifestyles will drive consumer

focus on health and well-being

The fundamental need to reduce our eco-footprint drives

demand for energy efficiency and sustainability

The lighting industry will face a massive shift from

conventional to digital, dynamic lighting and the entry of

new, non-traditional players

The relative importance of emerging markets in the world

economy continues to rise

Our opportunitiesGlobal trends

Portfolio leverages critical global trends

Fundamental growth trends

• Efficient health diagnostics

and treatment

• Home healthcare

• Healthy lifestyle and

preventive health

• Personal well-being

• Light for health

and well-being

• Energy-efficient lighting

• Emerging markets

• Sustainability

Strengthen existing leadership positions while

expanding promising businesses to become

leaders: In our three sectors, we aim to strengthen our

existing leadership positions while developing promising

businesses to become leaders. In 2015, we want to be the

market share leader in at least half of all our businesses. In

Healthcare, we will further differentiate our portfolio,

continue with our care-cycle approach and expand home

healthcare. In Lighting, we will further strengthen our

leading position in LED to capture the opportunities of a

fast-changing market. In Consumer Lifestyle, we will

continue to expand those businesses that provide higher

growth and profitability potential.

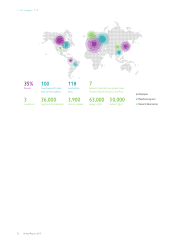

Continued focus on emerging markets: Emerging

markets are becoming more and more important to

Philips. As the number of middle-class households in these

markets grows, we expect demand for our products will

increase as people have more money to spend on feeling

and staying healthy. Therefore, we will continue to focus

on emerging markets by making sure we address local

needs effectively and continue to invest in having the right

capabilities in place to win in these fast-growing

economies. We aim to generate at least 40% of sales in

emerging markets by 2015.

We want to be seen as clear leaders in

sustainability: We are committed to being a leading

company in matters of sustainability. We look at

sustainability through the lenses of our sectors and define

specific ambitions for each of them: bring care to 500

million people; improve the energy efficiency of our

overall portfolio by 50%; double the amount of recycled

materials in our products as well as double the collection

and recycling of Philips products.

Our Vision 2015 aspirations

• Comparable sales growth on annual average basis at

least 2 percentage points higher than real GDP growth

• Reported EBITA margin between 10% and 13% of sales

• Growth of EPS at double the rate of comparable annual

sales growth

• Return on invested capital at least 4 percentage points

above weighted average cost of capital