Philips 2010 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

President’s message

Annual Report 2010 7

energy efficiency of our product portfolio by 4% and

launched a series of programs to increase the recycled

content of our products. After achieving our EcoVision4

Green Product sales target of 30% last year, we achieved

our Green Innovation target in 2010, two years ahead of

schedule.

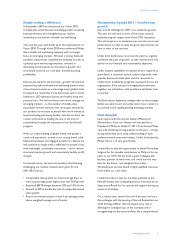

We are proposing to the upcoming General Meeting of

Shareholders to increase this year’s dividend to EUR 0.75

per common share, in cash or shares – resulting in a yield

(as of December 31, 2010) of 3.3% for shareholders.

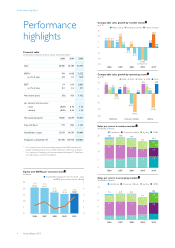

Dividend per common share

in euros

0.8

0.6

0.4

0.2

0

0.60

2007

0.70

2008

0.70

2009

0.70

2010

0.75

20111)

1) Subject to approval by the 2011 Annual General Meeting of Shareholders

How did we do against our Management

Agenda 2010?

Drive performance

Drive top-line growth and market share

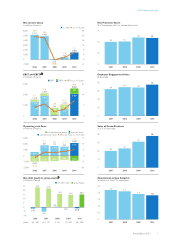

Sales amounted to EUR 25.4 billion, or 10% nominal

growth. Our 4.3% comparable sales growth was driven by

a strong 9% increase at Lighting and growth of 4% at

Healthcare, tempered by only 1% growth at Consumer

Lifestyle due to weak consumer confidence in developed

markets and ongoing portfolio pruning. Regionally, the US

and Europe continued to face very challenging market

conditions, though we were able to drive growth through

emerging markets, which accounted for 33% of revenues,

up from 30% in 2009. On average, market shares

remained steady.

Continue to reduce costs and improve cost agility

We have finalized most of our organization

transformation programs to optimize our industrial

footprint and organizational effectiveness. As a result,

productivity in 2010 improved by an impressive 20%. Our

fixed cost reduction, as well as our focus on managing

discretionary spend, contributed to our best EBITA

performance since 2000. At the same time, we have

continued to invest in Research and Development and

increased our Advertising and Promotion spend in

preparation for our Vision 2015 growth targets.

Further increase cash flow by managing cash aggressively

We generated EUR 470 million more free cash flow than

in 2009, an increase to 5.2% of sales, on the back of higher

cash earnings.

Accelerate change

Increase customer centricity by empowering local

markets and customer-facing staff

We realized that we cannot truly empower local markets

if our strategic and financial planning processes do not

allow for a voice from the market and a granular, fact-

based insight into the opportunities available in these

markets. We therefore decided to apply a simple three-

step approach where market opportunities precede

financial planning. This involves explicit dialog on growth

opportunities between market organizations and business

groups, allocating funds to priority opportunities, and

empowering market organizations to act within the

overall framework without complex decision procedures.

With this process in place, we should be better placed to

capture the opportunities for profitable growth in our

markets.

Increase number of businesses with NPS (co-) leadership

positions

Outstanding customer and consumer loyalty is critical to

achieving growth. In 2010, our Consumer Lifestyle

business increased its NPS leadership in a time of fragile

consumer confidence in many markets. Healthcare

maintained a strong position, and performed very well in

China. Lighting noted a slight decrease, yet remains a clear

leader in its industry, with 83% of leadership positions in

2010. The overall result is stable, with 59% of our

businesses currently holding industry leadership positions,

down one point from 2009. The result was negatively

impacted by supply chain constraints during the year, and

this will very much have our attention going forward. In

line with our Vision 2015 growth targets, in 2011 we will

continue to drive for further outright leadership in NPS in

key markets.