Philips 2010 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

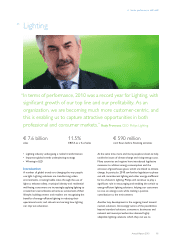

6 Sector performance 6.3.3 - 6.3.4

Annual Report 2010 97

Philips Lighting spans the entire lighting value chain – from

lighting sources, electronics and controls to full

applications and solutions – via the following businesses:

•Lamps: incandescent, halogen, (compact) fluorescent,

high-intensity discharge

• Consumer Luminaires: functional, decorative, lifestyle,

scene-setting

• Professional Luminaires: city beautification, road

lighting, sports lighting, office lighting, shop/hospitality

lighting, industry lighting

• Lighting Systems & Controls: electronic and

electromagnetic gear, controls, modules and drivers

• Automotive Lighting: car headlights, car signaling,

interior

• Packaged LEDs

• LED solutions: modules, LED replacement lamps

Total sales by business 2010

as a %

Lamps

40

Packaged LEDs/

LED solutions

7

Professional Luminaires

26

Consumer

Luminaires

6

Automotive

Lighting

8

Lighting Systems & Controls

13

The Lamps business conducts its sales and marketing

activities through the professional, OEM and consumer

channels, the latter also being used by our Consumer

Luminaires business. Professional Luminaires is organized

in a trade business (commodity products) and a project

solutions business (project luminaires, systems and

services). For the latter, the main focus is on specifiers,

lighting designers, architects and urban planners.

Automotive Lighting is organized in two businesses: OEM

and After-market. Lighting Systems & Controls, Special

Lighting Applications and Packaged LEDs/LED solutions

conduct their sales and marketing through both the OEM

and professional channels.

The conventional lamps industry is highly consolidated,

with GE and Siemens/Osram as key competitors. The LED

lamps and fluorescent retrofit industry is in its early days,

with a huge number of competitors entering the

marketplace. The luminaires industry is fragmented, with

our competition varying per region and per segment. Our

Lighting Systems & Controls and Automotive Lighting

businesses are again more consolidated. In the world of

digital lighting, a wide range of new entrants are active in

the transition to LED lighting as well as in the transition to

applications and solutions.

Philips Lighting has manufacturing facilities in some 25

countries in all regions of the world and sales

organizations in more than 60 countries. Commercial

activities in other countries are handled via dealers

working with our International Sales organization. Lighting

has approximately 53,000 employees worldwide.

Lighting strives for compliance with relevant regulatory

requirements, including the European Union’s Waste

from Electrical and Electronic Equipment (WEEE),

Restriction of Hazardous Substances (RoHS), Energy-

using Products (EuP) and Energy Performance of Buildings

(EPBD) directives.

With regard to sourcing, please refer to sub-section 5.3.3,

Supply management, of this Annual Report.

6.3.4 Progress against targets

The Annual Report 2009 set out a number of key targets

for Philips Lighting in 2010. The advances made in

addressing these are outlined below.

Drive performance

•Drive our performance through capturing growth while

managing cost and cash: Nominal sales grew by 15%,

delivering a significant improvement in profitability and

cash flow.

•Win with customers in key markets: Our market share

remained steady, and over two-thirds of our business/

market combinations have a leadership position in NPS.

•Improve our relative position in emerging markets, especially

China, India and Latin America: Comparable sales in

emerging markets grew from 34% to 38% of total sales,

driven by double-digit growth in China, India and Latin

America.

Accelerate change

•Further drive the transitions needed to retain the industry

lead in the LED era; optimize the lamps lifecycle, expand

share of leading LED solutions in professional and consumer

segments: Significant progress was made in growing LED

as a percentage of sales from 8% in 2009 to 13% in 2010.

We also undertook significant restructuring and

rightsizing efforts aimed at gearing up our organization

to take full advantage of the LED-driven future

opportunities in the lighting industry and adjusting our

cost structure to current market conditions. We added

a number of acquisitions to our portfolio to strengthen

our ability to offer LED solutions across segments.

These include Burton, a leading provider of specialized