Philips 2010 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

13 Group financial statements 13.10 - 13.10

Annual Report 2010 155

Translation differences on non-monetary financial assets and liabilities

such as equities held at fair value through profit or loss are recognized in

the Statement of income as part of the fair value gain or loss. Translation

differences on non-monetary financial assets, such as equities classified

as available for sale, are included in other comprehensive income.

Foreign operations

The assets and liabilities of foreign operations, including goodwill and

fair value adjustments arising on acquisition, are translated to euro at

exchange rates at the reporting date. The income and expenses of

foreign operations, are translated to euro at exchange rates at the dates

of the transactions.

Foreign currency differences arising on translation of foreign operations

into the group’s presentation currency are recognized in other

comprehensive income, and presented in the foreign currency

translation reserve (translation reserve) in equity. However, if the

operation is a non-wholly owned subsidiary, then the relevant

proportionate share of the translation difference is allocated to the

non-controlling interests. When a foreign operation is disposed of such

that control, significant influence or joint control is lost, the cumulative

amount is the translation reserve related to the foreign operation is

reclassified to the Statements of income as part of the gain or loss on

disposal. When the Company disposes of only part of its interest in a

subsidiary that includes a foreign operation while retaining control, the

relevant proportion of the cumulative amount is reattributed to non-

controlling interests. When the Company disposes of only part of its

investment in an associate or joint venture that includes a foreign

operation while retaining significant influence or joint control, the

relevant proportion of the cumulative amount is reclassified to the

Statements of income.

Discontinued operations and non-current assets held for sale

Non-current assets (disposal groups comprising assets and liabilities)

that are expected to be recovered primarily through sale rather than

through continuing use are classified as held for sale.

A discontinued operation is a component of an entity that either has

been disposed of, or that is classified as held for sale, and (a) represents

a separate major line of business or geographical area of operations; and

(b) is a part of a single coordinated plan to dispose of a separate major

line of business or geographical area of operations; or (c) is a subsidiary

acquired exclusively with a view to resale.

Non-current assets held for sale and discontinued operations are

carried at the lower of carrying amount or fair value less costs to sell.

Any gain or loss from disposal of a business, together with the results of

these operations until the date of disposal, is reported separately as

discontinued operations. The financial information of discontinued

operations is excluded from the respective captions in the

Consolidated financial statements and related notes for all years

presented.

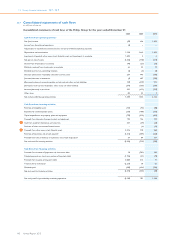

Cash flow statements

Cash flow statements are prepared using the indirect method. Cash

flows in foreign currencies have been translated into euros using the

weighted average rates of exchange for the periods involved. Cash

flows from derivative instruments that are accounted for as fair value

hedges or cash flow hedges are classified in the same category as the

cash flows from the hedged items. Cash flows from other derivative

instruments are classified consistent with the nature of the instrument.

Segments

Operating segments are components of the Company’s business

activities about which separate financial information is available that is

evaluated regularly by the chief operating decision maker (the Board of

Management of the Company). The Board of Management decides how

to allocate resources and assesses performance. Reportable segments

comprise the operating sectors: Healthcare, Consumer Lifestyle,

Lighting, and the business Television which is part of Consumer

Lifestyle. Segment accounting policies are the same as the accounting

policies as applied to the Group.

Earnings per share

The Company presents basic and diluted earnings per share (EPS) data

for its common shares. Basic EPS is calculated by dividing the net income

attributable to shareholders of the Company by the weighted average

number of common shares outstanding during the period, adjusted for

own shares held. Diluted EPS is determined by adjusting the profit or

loss attributable to shareholders and the weighted average number of

common shares outstanding, adjusted for own shares held, for the

effects of all dilutive potential common shares, which comprise

convertible personnel debentures, restricted shares and share options

granted to employees.

Revenue recognition

Revenue from the sale of goods in the course of the ordinary activities is

measured at the fair value of the consideration received or receivable,

net of returns, trade discounts and volume rebates. Revenue for sale of

goods is recognized when the significant risks and rewards of

ownership have been transferred to the buyer, recovery of the

consideration is probable, the associated costs and possible return of

the goods can be estimated reliably, there is no continuing involvement

with goods, and the amount of revenue can be measured reliably. If it is

probable that discounts will be granted and the amount can be

measured reliably, then the discount is recognized as a reduction of

revenue as the sales are recognized.

Transfer of risks and rewards varies depending on the individual terms

of the contract of sale. For consumer-type products in the Sectors

Lighting and Consumer Lifestyle, these criteria are met at the time the

product is shipped and delivered to the customer and, depending on the

delivery conditions, title and risk have passed to the customer and

acceptance of the product, when contractually required, has been

obtained, or, in cases where such acceptance is not contractually

required, when management has established that all aforementioned

conditions for revenue recognition have been met. Examples of the

above-mentioned delivery conditions are ‘Free on Board point of

delivery’ and ‘Costs, Insurance Paid point of delivery’, where the point

of delivery may be the shipping warehouse or any other point of

destination as agreed in the contract with the customer and where title

and risk in the goods pass to the customer.

Revenues of transactions that have separately identifiable components

are recognized based on their relative fair values. These transactions

mainly occur in the Healthcare sector and include arrangements that

require subsequent installation and training activities in order to

become operable for the customer. However, since payment for the

equipment is contingent upon the completion of the installation

process, revenue recognition is generally deferred until the installation

has been completed and the product is ready to be used by the

customer in the way contractually agreed.

Revenues are recorded net of sales taxes, customer discounts, rebates

and similar charges. For products for which a right of return exists

during a defined period, revenue recognition is determined based on

the historical pattern of actual returns, or in cases where such

information is not available, revenue recognition is postponed until the

return period has lapsed. Return policies are typically based on

customary return arrangements in local markets.

For products for which a residual value guarantee has been granted or a

buy-back arrangement has been concluded, revenue recognition takes

place when significant risks and rewards of ownership are transferred

to the customer. The following are the principal factors that the

Company considers in determining that the Company has transferred

significant risks and rewards:

• The period from the sale to the repurchase represents the major

(normally at least 75%) part of the economic life of the asset;

• The difference between the proceeds received on the initial transfer

and the amount of any residual value or repurchase price, measured

on a present value basis, amounts to substantially all (normally at

least 90%) of the fair value of the asset at the sale date;

• Insurance risk is borne by the customer; however, if the customer

bears the insurance risk but the Company bears the remaining risks,

then risks and rewards have not been transferred to the customer;

and

• The repurchase price is equal to the market value at the time of the

buy-back.

In case of loss under a sales agreement, the loss is recognized

immediately.

Shipping and handling costs billed to customers are recognized as

revenues. Expenses incurred for shipping and handling costs of internal

movements of goods are recorded as cost of sales. Shipping and

handling costs related to sales to third parties are recorded as selling

expenses and disclosed separately. Service revenue related to repair

and maintenance activities for goods sold is recognized ratably over the

service period or as services are rendered.