Philips 2010 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

6 Sector performance 6.2.3 - 6.2.4

Annual Report 2010 91

• Domestic Appliances: kitchen appliances, beverages/

espresso, garment care, floor care, water, air

• Television

• Audio & Video Multimedia: home audio, home video,

home cinema sound, portable audio and video

• Accessories: on-the-go accessories, together@home

accessories, personal displays, speech processing

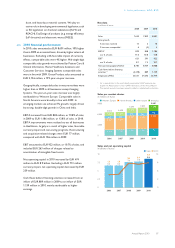

Total sales by business 2010

as a %

Health & Wellness

7

Television

36

Audio & Video Multimedia

13

Accessories

10

Other incl.

Licenses

4

Domestic

Appliances

17

Personal Care

13

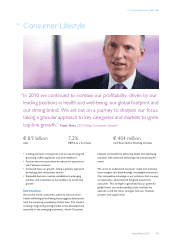

We also partner with leading companies from other fields,

such as Sara Lee/Douwe Egberts and Beiersdorf (NIVEA),

in order to deliver customer-focused appliance/

consumable combinations. Consumer Lifestyle continues

to focus on international key accounts, particularly in

emerging markets. We have pioneered innovative

approaches in online and social media to build our brand

and drive sales.

We offer a broad range of products from high to low

price/value quartiles, necessitating a diverse distribution

model. We are expanding our portfolio to increase its

accessibility, particularly for lower-tier cities in emerging

markets. We are also developing new retail channels, for

instance selling our innovative Intense Pulsed Light

depilation solution, Philips Lumea, in branches of Douglas,

the pan-European beauty retailer.

Under normal economic conditions, the Consumer

Lifestyle business experiences seasonality, with higher

sales in the fourth quarter resulting from the holiday sales.

Consumer Lifestyle employs approximately 17,700

people worldwide. Our global sales and service

organization covers more than 50 mature and emerging

markets. In addition, we operate manufacturing and

business creation organizations in the Netherlands,

France, Belgium, Austria, Hungary, Singapore, Argentina,

Brazil and China.

Consumer Lifestyle strives for full compliance with

relevant regulatory requirements.

With regard to sourcing, please refer to sub-section 5.3.3,

Supply management, of this Annual Report.

6.2.4 Progress against targets

The Annual Report 2009 set out a number of key targets

for Philips Consumer Lifestyle in 2010. The progress made

in addressing these targets is outlined below.

Drive performance

•Further increase cash flow by aggressively managing cash

targets: We strictly managed working capital, which has

been negative in many recent quarters. We effectively

managed our credit and risk, including significantly

reducing overdue customer payments. There was an

increase in the number of suppliers using supplier

finance, which reduced total cost in the supply chain. As

part of Philips’ drive to harmonize supplier terms, we

improved overall payment terms by 7 days.

•Continue to reduce fixed costs and improve the overall agility

of the cost base: We acted fast in the downturn and are

benefiting from improved gross margin and a lower cost

base, supporting year-on-year EBITA margin

improvement. We continued to manage costs via our

Earn 2 Invest Program, reinvesting savings to drive

growth.

•Strengthen excellence in execution and further develop

“sense and simplicity” as a competitive edge: We have

implemented an improved management decision

support system with granular insight into integral

performance per business, market and customer down

to product level. We are also striving to install a return

on investment (ROI) culture in order to drive, and

increase resources for, more effective advertising and

promotional campaigns.

Accelerate change

•Continually optimize the business portfolio, while prioritizing

profitable growth and success in selected new value spaces:

We have driven double-digit growth in our Health &

Wellness business and high single-digit growth in

Personal Care, as well as low single-digit growth in

Domestic Appliances. We have taken a granular

approach to ignite growth, focusing investments at a

category/country level.

•Nourish existing leadership positions, and increase

leadership positions in other categories by delighting

consumers and winning their preference: We have market

share leadership or co-leadership positions in 45% of

our businesses in emerging markets and 32% in mature

markets. We have Net Promoter Score leadership – a

key leading indicator for sales growth – in mother and

child care, power toothbrushes and male shaving and

grooming, as well as across a range of categories and

countries.