Philips 2010 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

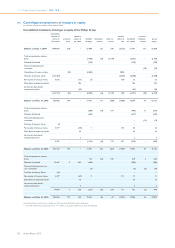

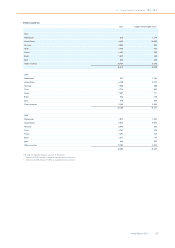

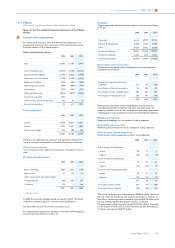

13 Group financial statements 13.10 - 13.10

Annual Report 2010 159

and measured by a comparison of the carrying amount of an asset with

the greater of its value in use and its fair value less cost to sell. Value in

use is measured as the present value of future cash flows expected to be

generated by the asset. If the carrying amount of an asset is deemed not

recoverable, an impairment charge is recognized in the amount by

which the carrying amount of the asset exceeds the recoverable

amount. The review for impairment is carried out at the level where

discrete cash flows occur that are independent of other cash flows.

Impairment losses recognized in prior periods are assessed at each

reporting date for any indications that the loss has decreased or no

longer exists. An impairment loss is reversed if and to the extent there

has been a change in the estimates used to determine the recoverable

amount. The loss is reversed only to the extent that the asset’s carrying

amount does not exceed the carrying amount that would have been

determined, net of depreciation or amortization, if no impairment loss

had been recognized. Reversals of impairment are recognized in the

Statements of income.

Goodwill

Measurement of goodwill at initial recognition is described under ‘Basis

of consolidation’. Goodwill is subsequently measured at cost less

accumulated impairment losses. In respect of investment in associates,

the carrying amount of goodwill is included in the carrying amount of

investment, and an impairment loss on such investment is not allocated

to any asset, including goodwill, that forms part of the carrying amount

of investment in associates.

Impairment of goodwill

Goodwill is not amortized but tested for impairment annually and

whenever impairment indicators require. In most cases the Company

identified its cash generating units as one level below that of an

operating segment. Cash flows at this level are substantially

independent from other cash flows and this is the lowest level at which

goodwill is monitored by the Board of Management. The Company

performed and completed annual impairment tests in the same quarter

of all years presented in the Consolidated Statements of income. A

goodwill impairment loss is recognized in the Statement of income

whenever and to the extent that the carrying amount of a cash-

generating unit exceeds the recoverable amount of that unit. An

impairment loss on an investment in associates is not allocated to any

asset, including goodwill, that forms part of the carrying amount of the

investment in associates.

Share capital

Common shares are classified as equity. Incremental costs directly

attributable to the issuance of shares are recognized as a deduction

from equity. Where the Company purchases the Company’s equity

share capital (treasury shares), the consideration paid, including any

directly attributable incremental costs (net of income taxes) is

deducted from equity attributable to the company’s equity holders until

the shares are cancelled or reissued. Where such ordinary shares are

subsequently reissued, any consideration received, net of any directly

attributable incremental transaction costs and the related income tax

effects, is included in equity attributable to the company’s equity

holders.

Debt and other liabilities

Debt and liabilities other than provisions are stated at amortized cost.

However, loans that are hedged under a fair value hedge are

remeasured for the changes in the fair value that are attributable to the

risk that is being hedged.

Provisions

Provisions are recognized if, as a result of a past event, the Company has

a present legal or constructive obligation that can be estimated reliably,

and it is probable that an outflow of economic benefits will be required

to settle the obligation. Provisions are measured at the present value of

the expenditures expected to be required to settle the obligation using

a pre-tax discount rate that reflects current market assessments of the

time value of money and the risks specific to the obligation. The

increase in the provision due to passage of time is recognized as interest

expense.

A provision for warranties is recognized when the underlying products

or services are sold. The provision is based on historical warranty data

and a weighing of possible outcomes against their associated

probabilities.

The Company accrues for losses associated with environmental

obligations when such losses are probable and can be estimated reliably.

Measurement of liabilities is based on current legal and constructive

requirements. Liabilities and expected insurance recoveries, if any, are

recorded separately. The carrying amount of liabilities is regularly

reviewed and adjusted for new facts and changes in law.

The provision for restructuring relates to the estimated costs of

initiated reorganizations that have been approved by the Board of

Management, and which involve the realignment of certain parts of the

industrial and commercial organization. When such reorganizations

require discontinuance and/or closure of lines of activities, the

anticipated costs of closure or discontinuance are included in

restructuring provisions. A liability is recognized for those costs only

when the Company has a detailed formal plan for the restructuring and

has raised a valid expectation with those affected that it will carry out

the restructuring by starting to implement that plan or announcing its

main features to those affected by it.

Guarantees

The Company recognizes a liability at the fair value of the obligation at

the inception of a financial guarantee contract. The guarantee is

subsequently measured at the higher of the best estimate of the

obligation or the amount initially recognized.

Accounting changes

In the absence of explicit transition requirements for new accounting

pronouncements, the Company accounts for any change in accounting

principle retrospectively.

Reclassifications

Certain items previously reported under specific financial statement

captions have been reclassified to conform to the current year

presentation.

IFRS accounting standards adopted as from 2010

The accounting policies set out above have been applied consistently to

all periods presented in these Consolidated financial statements except

as explained below which addresses changes in accounting policies.

The Company has adopted the following new and amended IFRSs as of

January 1, 2010.

Revision to IAS 27 ‘Consolidated and Separate Financial Statements’

The revised standard requires the effects of all transactions with non-

controlling interests to be recorded in equity if there is no change in

control and these transactions will no longer result in goodwill or gains

and losses. The standard also specifies the accounting when control is

lost. Any remaining interest in the entity is remeasured to fair value, and

a gain or loss is recognized in profit or loss. The Company applied IAS

27 (revised) prospectively to transactions with non-controlling

interests as from January 1, 2010.

Revision to IFRS 3, ‘Business Combinations’

The revised standard continues to apply the acquisition method to

business combinations, with some significant changes. For example, all

payments to purchase a business are to be recorded at fair value at the

acquisition date, with contingent payments classified as debt

subsequently re-measured through the Statements of income. The

definition of a business has been broadened, which likely results in more

acquisitions being treated as business combinations. There is a choice

on an acquisition-by-acquisition basis to measure the non-controlling

interest in the acquiree at fair value or at the non-controlling interest’s

proportionate share of the acquiree’s net assets. All acquisition-related

costs other than share and debt issuance costs, should be expensed.

The Company applied IFRS 3 (revised) prospectively to all business

combinations as from January 1, 2010.

IFRIC 17, ‘Distribution of Non-cash Assets to Owners’

The interpretation is part of the IASB’s annual improvements project

published in April 2009. This interpretation provides guidance on

accounting for arrangements whereby an entity distributes non-cash

assets to shareholders either as a distribution of reserves or as

dividends. IFRS 5 has also been amended to require that assets are

classified as held for distribution only when they are available for

distribution in their present condition and the distribution is highly