Philips 2010 Annual Report Download - page 196

Download and view the complete annual report

Please find page 196 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

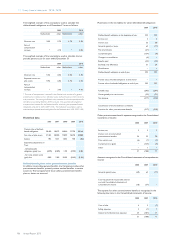

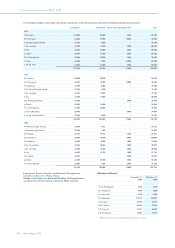

33 13 Group financial statements 13.11 - 13.11

196 Annual Report 2010

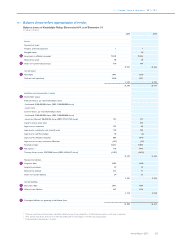

The table below analyses financial instruments carried at fair value, by

different hierarchy levels:

Fair value hierarchy

level 1 level 2 level 3 total

December 31, 2010

Available-for-sale financial

assets - non-current 298 298

Available-for-sale financial

assets - current − −

Financial assets designated at

fair value through profit and

loss - non-current 62 62

Financial asses designated at

fair value through profit and

loss - current − −

Derivative financial

instruments - assets 112 112

Total financial assets carried at

fair value 360 112 − 472

Derivative financial

instruments - liabilities (564) − (564)

December 31, 2009

Available-for-sale financial

assets - non-current 244 61 − 305

Available-for-sale financial

assets - current 145 145

Financial assets designated at

fair value through profit and

loss - non-current 30 2 32

Financial assets designated at

fair value through profit and

loss - current 25 25

Derivative financial

instruments - assets 102 102

Total financial assets carried at

fair value 274 335 − 609

Derivative financial

instruments - liabilities (276) (276)

Specific valuation techniques used to value financial instruments include:

Level 1

Instruments included in level 1 are comprised primarily of listed equity

investments classified as available-for-sale financial assets, investees and

financial assets designated at fair value through profit and loss.

The fair value of financial instruments traded in active markets is based

on quoted market prices at the balance sheet date. A market is

regarded as active if quoted prices are readily and regularly available

from an exchange, dealer, broker, industry group, pricing service, or

regulatory agency, and those prices represent actual and regularly

occurring market transactions on an arm’s length basis.

Level 2

The fair value of financial instruments that are not traded in an active

market (for example, over-the-counter derivatives or convertible bond

instruments) are determined by using valuation techniques. These

valuation techniques maximize the use of observable market data

where it is available and rely as little as possible on entity-specific

estimates. If all significant inputs required to fair value an instrument are

based on observable market data, the instrument is included in level 2.

The fair value of derivatives is calculated as the present value of the

estimated future cash flows based on observable interest yield curves

and foreign exchange rates.

The valuation of convertible bond instruments uses observable market

quoted data for the options and present value calculations using

observable yield curves for the fair value of the bonds.

Level 3

If one or more of the significant inputs are not based on observable

market data, the instrument is included in level 3. The arrangement with

the UK Pension Fund in conjunction with the sale of NXP is a financial

instrument carried at fair value classified as level 3. At the end of 2010,

the fair value of this instrument is estimated to be zero. Please refer to

note 11 for more details.

33 Details of treasury risks

Philips is exposed to several types of financial risk. This note further

analyzes financial risks. Philips does not purchase or hold derivative

financial instruments for speculative purposes. Information regarding

financial instruments is included in note 32.

Liquidity risk

Liquidity risk is the risk that an entity will encounter difficulty in meeting

obligations associated with financial liabilities.

Liquidity risk for the group is monitored through the Treasury liquidity

committee which tracks the development of the actual cash flow

position for the group and uses input from a number of sources in order

to forecast the overall liquidity position both on a short and long-term

basis. Corporate treasury invests surplus cash in money market

deposits with appropriate maturities to ensure sufficient liquidity is

available to meet liabilities when due.

The rating of the Company’s debt by major rating services may improve

or deteriorate. As a result, Philips’ future borrowing capacity may be

influenced and its financing costs may fluctuate. Philips has various

sources to mitigate the liquidity risk for the group. At the reporting

date, Philips had EUR 5,833 million in cash and cash equivalents (2009:

EUR 4,386 million), within which short-term deposits of EUR 5,229

million (2009: EUR 3,740 million) and other liquid assets of EUR 104

million (2009: EUR 155 million). Philips pools cash from subsidiaries to

the extent legally and economically feasible; cash not pooled remains

available for local operational or investment needs.

Furthermore, Philips had a USD 2.5 billion Commercial Paper Program;

a EUR1.8 billion committed revolving facility that can be used for

general corporate purpose and a committed bilateral loan of EUR 200

million. As of December 31, 2010, Philips did not have any loans

outstanding under any of these facilities. Additionally Philips also held a

EUR 270 million of equity investments in available-for-sale financial

assets (fair value at December 31, 2010).

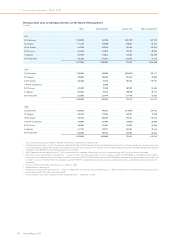

Currency risk

Currency risk is the risk that the fair value or future cash flows of a

financial instrument will fluctuate because of changes in foreign

exchange rates. Currency fluctuations may impact Philips’ financial

results. Philips is exposed to currency risk in the following areas:

• Transaction exposures, related to forecasted sales and purchases

and on-balance-sheet receivables/payables resulting from such

transactions

• Translation exposure of net income in foreign entities

• Translation exposure of foreign-currency intercompany and

external debt and deposits

• Translation exposure of foreign-currency-denominated equity

invested in consolidated companies

• Translation exposure to equity interests in non-functional-currency

investments in associates and available-for-sale financial assets.

It is Philips’ policy that significant transaction exposures are hedged by

the businesses. Accordingly, all businesses are required to identify and

measure their exposures resulting from material transactions

denominated in currencies other than their own functional currency.

Philips’ policy generally requires committed foreign currency exposures

to be fully hedged using forwards. Anticipated transactions may be

hedged using forwards or options or a combination thereof. The

amount hedged as a proportion of the total exposure identified varies

per business and is a function of the ability to project cash flows, the

time horizon for the cash flows and the way in which the businesses can

adapt to changed levels of foreign-currency exchange rates. As a result,

hedging activities will not eliminate all currency risks for these

anticipated transaction exposures. Generally, the maximum tenor of

these hedges is 18 months.