Philips 2010 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

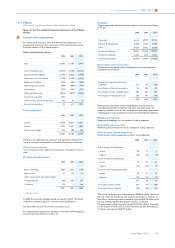

13 Group financial statements 13.10 - 13.10

158 Annual Report 2010

associates are eliminated to the extent of the Company’s interest in the

associates. Unrealized losses are also eliminated unless the transaction

provides evidence of an impairment of the asset transferred.

Investments in associates include loans from the Company to these

investees.

Accounting for capital transactions of a consolidated

subsidiary or an associate

The Company recognizes dilution gains or losses arising from the sale

or issuance of stock by a consolidated subsidiary or an associate in the

Statement of income, unless the Company or the subsidiary either has

reacquired or plans to reacquire such shares. In such instances, the

result of the transaction will be recorded directly in equity.

Dilution gains and losses arising in investments in associates are

recognized in the Consolidated statements of income under “Results

relating to investments in associates”.

Other non-current financial assets

Other non-current financial assets include held-to-maturity

investments, loans and available-for-sale financial assets and financial

assets at fair value through profit and loss.

Held-to-maturity investments are those debt securities which the

Company has the ability and intent to hold until maturity. Held-to-

maturity debt investments are recorded at amortized cost, adjusted for

the amortization or accretion of premiums or discounts using the

effective interest method.

Loans receivable are stated at amortized cost, less the related

allowance for impaired loans receivable.

Available-for-sale financial assets are non-derivatives financial assets

that are designated as available-for-sale and that are not classified in any

of the other categories of financial assets. Subsequent to initial

recognition, they are measured at fair value and changes therein, other

than impairment losses and foreign currency differences on available for

sale-debt instruments are recognized in other comprehensive income

and presented in the fair value reserve in equity. When an investment is

derecognized, the gain or loss accumulated in equity is reclassified to

the Statements of income.

Available-for-sale financial assets including investments in privately held

companies that are not associates, and do not have a quoted market

price in an active market and whose fair value could not be reliably

determined, are carried at cost.

A financial asset is classified as at fair value through profit or loss if it is

classified as held for trading or is designated as such upon initial

recognition. Financial assets are designated at fair value through profit

or loss if the Company manages such investments and makes purchase

and sale decisions based on their fair value in accordance with the

Company documented risk management or investment strategy.

Attributable transaction costs are recognized in the Statement of

income as incurred. Financial assets at fair value through the Statement

of income are measured at fair value, and changes therein are

recognized as available for sale.

Impairment of financial assets

A financial asset is considered to be impaired if objective evidence

indicates that one or more events have had a negative effect on the

estimated future cash flows of that asset. In case of available-for-sale

financial assets, a significant or prolonged decline in the fair value of the

financial assets below its cost is considered an indicator that the

financial assets are impaired. If any such evidence exists for available-

for-sale financial assets, the cumulative loss - measured as the difference

between the acquisition cost and the current fair value, less any

impairment loss on that financial asset previously recognized in the

Statement of income - is removed from equity and recognized in the

Statement of income.

If objective evidence indicates that financial assets that are carried at

cost need to be tested for impairment, calculations are based on

information derived from business plans and other information available

for estimating their fair value. Any impairment loss is charged to the

Statement of income.

An impairment loss related to financial assets is reversed if in a

subsequent period, the fair value increases and the increase can be

related objectively to an event occurring after the impairment loss was

recognized. The loss is reversed only to the extent that the asset’s

carrying amount does not exceed the carrying amount that would have

been determined, if no impairment loss had been recognized. Reversals

of impairment are recognized in the Statement of income except for

reversals of impairment of available-for-sale equity securities, which are

recognized in other comprehensive income.

Inventories

Inventories are stated at the lower of cost or net realizable value. The

cost of inventories comprises all costs of purchase, costs of conversion

and other costs incurred in bringing the inventories to their present

location and condition. The costs of conversion of inventories include

direct labor and fixed and variable production overheads, taking into

account the stage of completion and the normal capacity of production

facilities. Costs of idle facility and abnormal waste are expensed. The

cost of inventories is determined using the first-in, first-out (FIFO)

method. Inventory is reduced for the estimated losses due to

obsolescence. This reduction is determined for groups of products

based on purchases in the recent past and/or expected future demand.

Property, plant and equipment

Items of property, plant and equipment are measured at cost less

accumulated depreciation and accumulated impairment losses. The

useful lives and residual values are evaluated every year.

Assets manufactured by the Company include direct manufacturing

costs, production overheads and interest charges incurred for

qualifying assets during the construction period. Government grants

are deducted from the cost of the related asset. Depreciation is

calculated using the straight-line method over the useful life of the asset.

Depreciation of special tooling is generally also based on the straight-

line method. Gains and losses on the sale of property, plant and

equipment are included in other business income. Costs related to

repair and maintenance activities are expensed in the period in which

they are incurred unless leading to an extension of the original lifetime

or capacity.

Plant and equipment under finance leases and leasehold improvements

are amortized using the straight-line method over the shorter of the

lease term or the estimated useful life of the asset. The gain realized on

sale and operating leaseback transactions that are concluded based

upon market conditions is recognized at the time of the sale.

The Company capitalizes interest as part of the cost of assets that take a

substantial period of time to become ready for use.

Intangible assets other than goodwill

Acquired definite-lived intangible assets are amortized using the

straight-line method over their estimated useful life. The useful lives are

evaluated every year. Patents and trademarks with a definite useful live

acquired from third parties either separately or as part of the business

combination are capitalized at cost and amortized over their remaining

useful lives. Intangible assets acquired as part of a business combination

are capitalized at their acquisition-date fair value.

The Company expenses all research costs as incurred. Expenditure on

development activities, whereby research findings are applied to a plan

or design for the production of new or substantially improved products

and processes, is capitalized as an intangible asset if the product or

process is technically and commercially feasible and the Company has

sufficient resources and the intention to complete development.

The development expenditure capitalized includes the cost of materials,

direct labor and an appropriate proportion of overheads. Other

development expenditures and expenditures on research activities are

recognized in the Statement of income. Capitalized development

expenditure is stated at cost less accumulated amortization and

impairment losses. Amortization of capitalized development

expenditure is charged to the Statement of income on a straight-line

basis over the estimated useful lives of the intangible assets.

Costs relating to the development and purchase of software for both

internal use and software intended to be sold are capitalized and

subsequently amortized over the estimated useful life.

Impairment of non-financial assets other than goodwill,

inventories and deferred tax assets

Non-financial assets other than goodwill, inventories and deferred tax

assets are reviewed for impairment whenever events or changes in

circumstances indicate that the carrying amount of an asset may not be

recoverable. Recoverability of assets to be held and used is recognized