Philips 2010 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

6 Sector performance 6.3.5 - 6.3.6

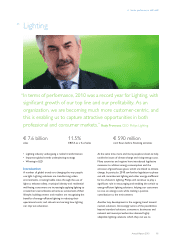

Annual Report 2010 99

Key data

in millions of euros

2008 2009 2010

Sales 7,362 6,546 7,552

Sales growth

% increase, nominal 16 (11) 15

% increase, comparable1) 3 (13) 9

EBITA1) 480 145 869

as a % of sales 6.5 2.2 11.5

EBIT1) 24 (16) 695

as a % of sales 0.3 (0.2) 9.2

Net operating capital (NOC)1) 5,712 5,104 5,561

Cash flows before financing

activities1,2) (1,181) 624 590

Employees (FTEs) 57,367 51,653 53,888

1) For a reconciliation to the most directly comparable GAAP measures, see

chapter 16, Reconciliation of non-GAAP information, of this Annual Report

2) Prior period amounts have been revised to reflect an adjusted sector allocation

Sales per market cluster

in millions of euros

■-Western Europe--■-North America--■-other mature--■-emerging

9,000

6,000

3,000

0

2006

2,096

1,274

347

1,943

5,660

2007

2,524

1,219

308

2,270

6,321

2008

2,665

2,041

276

2,380

7,362

2009

2,271

1,811

253

2,211

6,546

2010

2,297

1,989

367

2,899

7,552

Sales and net operating capital

in billions of euros ■-Sales----NOC

9

6

3

0

9

6

3

0

2.8

5.7

2006

4.1

6.3

2007

5.7

7.4

2008

5.1

6.5

2009

5.6

7.6

2010

EBIT and EBITA1)

in millions of euros

■-EBIT in value--■

■-EBITA in value----EBITA as a % of sales

1,200

800

400

0

(400)

30

20

10

0

(10)

564 71

635

11.6

2006

66474

738

11.7

2007

24

456

480

6.5

2008

(16)

161

145

2.2

2009

695

174

869

11.5

2010

161

1) For a reconciliation to the most directly comparable GAAP measures, see

chapter 16, Reconciliation of non-GAAP information, of this Annual Report

6.3.6 Strategy and 2011 objectives

Philips Lighting will continue to play an important role in

the realization of Philips’ strategic ambitions in the domain

of health and well-being.

Lighting has defined the following key business objectives

for 2011:

Drive performance

• Accelerate growth and gain market share in:

- LED lighting

- Segment-specific solutions

- Emerging markets

• Enhance customer service levels

• Increase outright NPS leadership positions and brand

preference

• Continue to optimize profit, minimize cost, maximize

cash

Improve capabilities

• Reinforce a growth culture based on:

- Speed

- Customer responsiveness

- Empowerment

• Improve market impact through integral business

models and end-to-end value chain execution

• Drive innovation effectiveness

- Faster innovation cycles

- Better time-to-market

- Seamless strategy/design/marketing/technology

cooperation

• “Resource to win” through strategic workforce

planning and by enhancing diversity, talent and

competency management