Philips 2010 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

4 13 Group financial statements 13.11 - 13.11

166 Annual Report 2010

Tax uncertainties on general service agreements and specific

allocation contracts

Due to the centralization of certain activities in a limited number of

countries (such as research and development, centralized IT, corporate

functions and head office), costs are also centralized. As a consequence,

for tax reasons these costs and/or revenues must be allocated to the

beneficiaries, i.e. the various Philips entities. For that purpose, apart

from specific allocation contracts for costs and revenues, general

service agreements (GSAs) are signed with a large number of entities.

Tax authorities review the implementation of GSAs, apply benefit tests

for particular countries or audit the use of tax credits attached to GSAs

and royalty payments, and may reject the implemented procedures.

Furthermore, buy in/out situations in the case of (de)mergers could

affect the tax allocation of GSAs between countries. The same applies

to the specific allocation contracts.

Tax uncertainties due to disentanglements and acquisitions

When a subsidiary of Philips is disentangled, or a new company is

acquired, related tax uncertainties arise. Philips creates merger and

acquisition (M&A) teams for these disentanglements or acquisitions. In

addition to representatives from the involved sector, these teams

consist of specialists from various corporate functions and are formed,

amongst other things, to identify hidden tax uncertainties that could

subsequently surface when companies are acquired and to reduce tax

claims related to disentangled entities. These tax uncertainties are

investigated and assessed to mitigate tax uncertainties in the future as

much as possible. Several tax uncertainties may surface from M&A

activities. Examples of uncertainties are: applicability of the participation

exemption, allocation issues, and non-deductibility of parts of the

purchase price.

Tax uncertainties due to permanent establishments

In countries where e.g. Philips starts new operations or alters business

models, the issue of permanent establishment may arise. This is because

when operations in a country are led from another country, there is a

risk that tax claims will arise in the former country as well as in the latter

country.

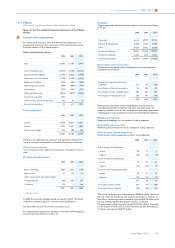

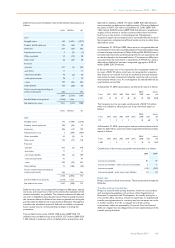

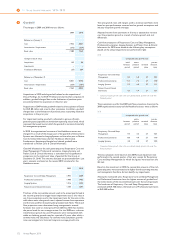

4Investments in associates

Results relating to investments in associates

2008 2009 2010

Company’s participation in income 81 23 14

Results on sales of shares (2) − 5

Gains from dilution effects 12 − −

Investment impairment / other charges (72) 53 (1)

19 76 18

Detailed information on the aforementioned individual line items is

provided below.

Company’s participation in income

2008 2009 2010

LG Display 66 − −

Others 15 23 14

81 23 14

Philips’ influence on LG Display’s operating and financial policies

including representation on the LG Display board was reduced in

February 2008. Consequently, the investment in LG Display (at that

date 19.9%) was transferred from Investments in associates to Other

non-current financial assets, as Philips was no longer able to exercise

significant influence.

Results on sales of shares

2008 2009 2010

TPV Technology Ltd. − − 5

Others (2) − −

(2) − 5

Investment impairment/other income and expenses

2008 2009 2010

LG.Philips Displays (9) − −

TPV Technology Ltd. (59) 55 −

Others (4) (2) (1)

(72) 53 (1)

In 2009, the TPV Technology Ltd. impairment charge of 2008 was

reversed (EUR 55 million) based on the 2009 stock price.

In 2008, Philips performed impairment reviews on the book value of the

investment in TPV resulting in an impairment charge of EUR 59 million.

The impairment reviews were triggered by the deteriorating economic

environment of the flat panel industry, the weakening financial

performance of TPV and the stock price performance of TPV. The

valuation as per December 31, 2008 was based on the stock price of

TPV as of that date on the Hong Kong Stock Exchange.

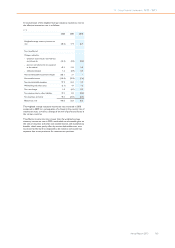

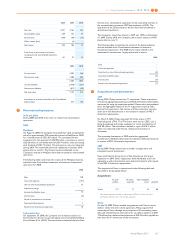

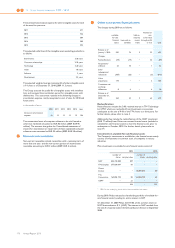

Investments in associates

The changes during 2010 are as follows:

Investments in associates

loans investments total

Balance as of January 1, 2010 7 274 281

Changes:

Acquisitions/additions − 18 18

Sales − (89) (89)

Reclassifications (4) (34) (38)

Share in income/value

adjustments − 18 18

Impairments − (5) (5)

Dividends received − (19) (19)

Translation and exchange rate

differences − 15 15

Balance as of December 31,

2010 3 178 181

Reclassifications mainly relate to the accounting of TPV Technology Ltd.

(TPV). On March 9, 2010 Philips sold 9.4% of the shares in TPV to a third

party for a cash consideration of EUR 98 million. Philips retained 3.0% of

the TPV shares, which were transferred to Other non-current financial

assets, because Philips was no longer able to exercise significant

influence with respect to TPV. The transaction resulted in a gain of EUR

5 million, which was recognized under Results relating to investments in

associates.

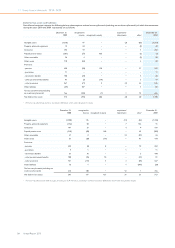

Summarized information of investments in associates

(unaudited)

Summarized financial information on the Company’s investments in

associates, on a combined basis, is presented below.

The gradual decline of the amounts stated in the table is due to the

accounting for the investments in LG Display in February 2008 and TPV

in March 2010 as other non-current financial assets. This is based on the

most recent available financial information.