Philips 2010 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

13 Group financial statements 13.11 - 13.11 12 13 14 15 16

Annual Report 2010 175

Until August 5, 2010 NXP was a privately-held company that was not

quoted in any active market and consequently carried at impaired cost

because the fair value could not be reliably determined. Until that date

Philips performed impairment reviews on the carrying value of the

investment in NXP.

According to IAS 39, if there is objective evidence that an impairment

loss has been incurred for an unquoted equity investment carried at

cost, the amount of the impairment loss is measured as the difference

between the carrying amount of the investment and the present value of

the estimated discounted future cash flows. The discounted future cash

flows for NXP were estimated using various valuation techniques

including multiplier calculations (‘EBITDA multiples’), calculations based

on the share price performance of a peer group of listed

(semiconductor) companies and discounted cash-flow models based on

unobservable inputs. The latter methodology involved estimates of

revenues, expenses, capital spending and other costs, as well as a

discount rate calculated from the risk profile of the semiconductor

industry. At the end of the first quarter of 2009, impairment charges

were recognized in the amount of EUR 48 million, which resulted in a

carrying amount of EUR 207 million, being management’s best estimate

of future cash flows for the NXP investment at that time. Based on the

impairment reviews performed between the end of the first quarter

2009 and August 5, 2010 it was concluded that no further impairments

were necessary.

On August 6, 2010 NXP completed an initial public offering (IPO) of

newly issued common shares at the NASDAQ. The consequence of this

IPO was firstly that the interest held by Philips was diluted to 17% and

secondly that a reliable measure became available in order to fair value

the NXP shares held by Philips. The difference between the fair value

determined on the basis of the initial offering price (EUR 455 million)

and the impaired cost (EUR 207 million) was recorded in equity (Other

comprehensive income) in August 2010. Subsequent changes in the fair

value until September 7, 2010 were also recognized in equity.

On September 7, 2010 Philips sold its entire holding of common shares

in NXP to Philips Pension Trustees Limited (herein after referred to as

“UK Pension Fund”) for a consideration of EUR 361 million which was

8% below the fair value determined on the stock price as of the close of

the previous business day. The transaction resulted in a gain of EUR 154

million, reported under Financial income.

The purchase agreement with the UK Pension Fund includes an

arrangement that may entitle Philips to a cash payment from the UK

Pension Fund on or after September 7, 2014 if the value of the NXP

shares has increased by this date to a level in excess of a predetermined

threshold, which at the time of the transaction was substantially above

the transaction price, and the UK Pension Fund is in a surplus (on the

regulatory funding basis) on September 7, 2014.

The arrangement qualifies as a financial instrument, which must be

accounted for at fair value, with fair value changes to be reported in

financial income and expenses. The fair value of the arrangement was

estimated to be zero at the transaction date. As of December 31, 2010,

the share price of NXP exceeded the threshold in the arrangement,

however, the UK Pension Fund was still in a regulatory deficit position

on this date. Management estimates, based on the risks, the current

progress and the long term nature of the recovery plan, that it is still

highly uncertain that the UK Pension Fund will achieve a regulatory

surplus by September 7, 2014. Therefore, the fair value of the

arrangement on December 31, 2010 is estimated to be zero.

On March 18, 2010 TPO Displays Corp. (TPO Displays) merged with

Innolux Display Corp. and Chi Mei Optoelectronics into a new

company named Chimei Innolux Corporation (Chimei Innolux). The

shares held by Philips in TPO Displays were exchanged into shares of

Chimei Innolux. Valuation differences between the shares were

recognized in Other comprehensive income.

Loans and receivables

Loans and receivables mainly relate to restricted liquid assets.

12 Other non-current assets

Other non-current assets in 2010 are comprised of prepaid pension

costs of EUR 14 million (2009: EUR 1,518 million) and prepaid expenses

of EUR 61 million (2009: EUR 25 million).

The decrease of the prepaid pension cost in 2010 is attributable to the

pension plan in the Netherlands, the surplus of which no longer is

recognized as an asset. For further details see note 28.

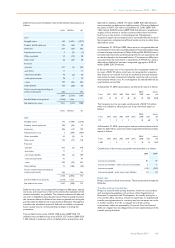

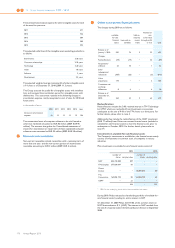

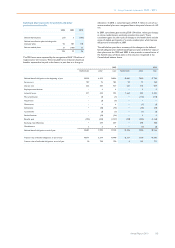

13 Inventories

Inventories are summarized as follows:

2009 2010

Raw materials and supplies 871 1,131

Work in process 408 510

Finished goods 1,634 2,224

2,913 3,865

The amounts recorded above are net of allowances for obsolescence.

In 2010, the write-down of inventories to net realizable value amounted

to EUR 228 million (2009: EUR 219 million). The write-down is included

in cost of sales.

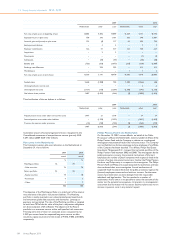

14 Current financial assets

Other current financial assets were EUR 5 million as at December 31,

2010 (2009: EUR 191 million). During 2010, two convertible bonds

previously issued to Philips by TPV Technology Limited and CBAY were

redeemed generating a total of EUR 239 million cash inflow. During

2010, a fair value loss of EUR 21 million was recognized in financial

income and expense, mainly related to these instruments.

15 Other current assets

Other current assets include prepaid expenses of EUR 348 million

(2009: EUR 334 million).

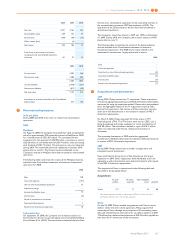

16 Current receivables

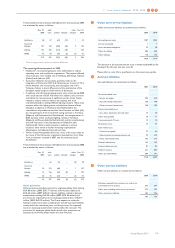

The accounts receivable, net, per sector are as follows:

2009 2010

Healthcare 1,571 1,848

Consumer Lifestyle 1,096 1,082

Lighting 909 1,072

Group Management & Services 93 102

3,669 4,104

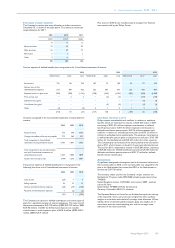

The aging analysis of accounts receivable, net, is set out below:

2009 2010

current 3,075 3,439

overdue 1-30 days 307 297

overdue 31-180 days 241 283

overdue > 180 days 46 85

3,669 4,104

A large part of overdue trade accounts receivable relates to public

sector customers with slow payment approval processes. The

allowance for doubtful accounts receivable has been primarily

established for receivables that are past due.