Philips 2010 Annual Report Download - page 197

Download and view the complete annual report

Please find page 197 of the 2010 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

13 Group financial statements 13.11 - 13.11

Annual Report 2010 197

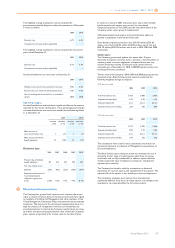

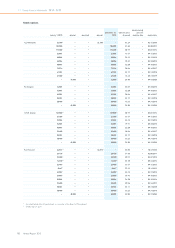

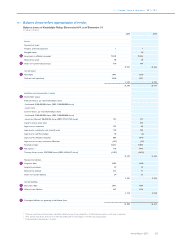

The following table outlines the estimated nominal value in millions of

euros for transaction exposure and related hedges for Philips’ most

significant currency exposures consolidated as of December 31, 2010:

Estimated transaction exposure and related hedges

in millions of euros

maturity 0-60 days maturity over 60 days

exposure hedges exposure hedges

Receivables

Functional vs

exposure

currency

EUR vs. USD 734 (712) 1,405 (955)

USD vs. EUR 173 (132) 759 (409)

EUR vs. JPY 39 (39) 164 (127)

EUR vs. GBP 44 (39) 144 (85)

USD vs. JPY 38 (26) 122 (62)

EUR vs. PLN 38 (31) 104 (56)

CNY vs. EUR 4 (2) 119 (24)

CNY vs. USD 12 (7) 107 (65)

EUR vs. SEK 38 (32) 78 (45)

Others 171 (138) 437 (227)

Payables

Functional vs

exposure

currency

EUR vs. USD (982) 972 (1,641) 946

USD vs. CNY (57) 57 (219) 118

BRL vs. USD (83) 66 (123) 59

EUR vs. PLN (48) 39 (156) 84

GBP vs. EUR (25) 20 (122) 64

CNY vs. EUR (18) 13 (106) 51

IDR vs. USD (21) 15 (98) 51

USD vs. SGD (17) 12 (84) 43

Others (290) 258 (524) 320

The derivatives related to transactions are, for hedge accounting

purposes, split into hedges of on-balance-sheet accounts receivable/

payable and forecasted sales and purchases. Changes in the value of on-

balance-sheet foreign-currency accounts receivable/payable, as well as

the changes in the fair value of the hedges related to these exposures,

are reported in the income statement under costs of sales. Hedges

related to forecasted transactions, where hedge accounting is applied,

are accounted for as cash flow hedges. The results from such hedges are

deferred in other comprehensive income within equity to the extent

that the hedge is effective. As of December 31, 2010, a gain of EUR 5

million was deferred in equity as a result of these hedges. The result

deferred in equity will be released to earnings mostly during 2011 at the

time when the related hedged transactions affect the income statement.

During 2010, a net gain of EUR 7 million was recorded in the income

statement as a result of ineffectiveness on certain anticipated cash flow

hedges.

The total net fair value of hedges related to transaction exposure as of

December 31, 2010 was an unrealized liability of EUR 29 million. An

instantaneous 10% increase in the value of the euro against all

currencies would lead to an increase of EUR 20 million in the value of

the derivatives; including a EUR 68 million increase related to foreign

exchange transactions of the euro against the US dollar, offset by a EUR

14 million decrease related to foreign exchange transactions of the euro

against the Japanese yen, and a EUR 14 million decrease related to

foreign exchange transactions of the euro against the Pound sterling.

The EUR 20 million increase includes a gain of EUR 33 million that

would impact the income statement, which would largely offset the

opposite revaluation effect on the underlying accounts receivable and

payable, and the remaining loss of EUR 13 million would be recognized

in equity to the extent that the cash flow hedges were effective.

Foreign exchange exposure also arises as a result of inter-company

loans and deposits. Where the Company enters into such arrangements

the financing is generally provided in the functional currency of the

subsidiary entity. The currency of the Company’s external funding and

liquid assets is matched with the required financing of subsidiaries either

directly through external foreign currency loans and deposits, or

synthetically by using foreign exchange derivatives. In certain cases

where group companies may also have external foreign currency debt

or liquid assets, these exposures are also hedged through the use of

foreign exchange derivatives. Changes in the fair value of hedges related

to this translation exposure are recognized within financial income and

expenses in the income statement and are largely offset by the

revaluation of the hedged items. The total net fair value of these

derivatives as of December 31, 2010, was a liability of EUR 425 million.

An instantaneous 10% increase in the value of the euro against all

currencies would lead to a increase of EUR 323 million in the value of

the derivatives, including a EUR 315 million increase related to the US

dollar.

Philips does not hedge the translation exposure of net income in foreign

entities. Translation exposure of foreign-currency equity invested in

consolidated entities may be hedged. If a hedge is entered into, it is

accounted for as a net investment hedge. As of December 31, 2010,

Philips had no outstanding derivatives accounted for as net investment

hedges. During 2010, Philips recorded a gain of EUR 9 million in other

comprehensive income under currency translation differences as a

result of net investment hedges.

Philips does not currently hedge the foreign exchange exposure arising

from equity interests in non-functional-currency investments in

associates and available-for-sale financial assets.

Interest rate risk

Interest rate risk is the risk that the fair value or future cash flows of a

financial instrument will fluctuate because of changes in market interest

rates. Philips had outstanding debt of EUR 4,658 million, which created

an inherent interest rate risk. Failure to effectively hedge this risk could

negatively impact financial results. At year-end, Philips held EUR 5,833

million in cash and cash equivalents, total gross long-term debt of EUR

2,818 million and total short-term debt of EUR 1,840 million. At

December 31, 2010, Philips had a ratio of fixed-rate gross long-term

debt to total outstanding gross debt of approximately 55%, compared

to 73% one year earlier.

A sensitivity analysis shows that if long-term interest rates were to

decrease instantaneously by 1% from their level of December 31, 2010,

with all other variables (including foreign exchange rates) held constant,

the fair value of the long-term debt would increase by approximately

EUR 226 million. If there was an increase of 1% in long-term interest

rates, this would reduce the market value of the long-term debt by

approximately EUR 226 million.

If interest rates were to increase instantaneously by 1% from their level

of December 31, 2010, with all other variables held constant, the

annualized net interest expense would decrease by approximately EUR

39 million. This impact was based on the outstanding net cash position

at December 31, 2010.

Equity price risk

Equity price risk is the risk that the fair value or future cash flows of a

financial instrument will fluctuate because of changes in equity prices.

Philips is a shareholder in several publicly listed companies, including

TCL Corporation and TPV Technology Ltd. As a result, Philips is

exposed to potential financial loss through movements in their share

prices. The aggregate equity price exposure of publicly listed

investments in its main available-for-sale financial assets amounted to

approximately EUR 270 million at year-end 2010 (2009: EUR 357

million including investments in associates shares that were sold during

2010). Philips does not hold derivatives in its own stock or in the above-

mentioned listed companies. The two options on the shares of TPV and

CBAY were matured and redeemed in September and October 2010

respectively. Philips is also a shareholder in several privately owned

companies amounting to EUR 24 million. As a result, Philips is exposed

to potential value adjustments.