Regions Bank 2011 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

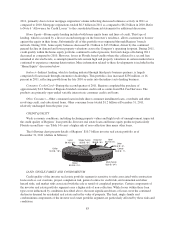

Portfolio Quality—Regions’ investment policy emphasizes credit quality and liquidity. Securities rated in

the highest category by nationally recognized rating agencies and securities backed by the U.S. Government and

government sponsored agencies, both on a direct and indirect basis, represented approximately 97 percent of the

investment portfolio at December 31, 2011. All other securities rated below AAA, not backed by the U.S.

Government or government sponsored agencies, or which are not rated represented less than 3 percent of total

securities at year-end 2011.

Loans Held for Sale

At December 31, 2011, loans held for sale totaled $1.2 billion, consisting of $844 million of residential real

estate mortgage loans and $328 million of non-performing investor real estate loans. At December 31, 2010,

loans held for sale totaled $1.5 billion, consisting of $1.2 billion of residential real estate mortgage loans and

$304 million of non-performing investor real estate loans. The level of residential real estate mortgage loans held

for sale fluctuates depending on the timing of origination and sale to third parties.

Loans

GENERAL

Average loans, net of unearned income, represented 72 percent of average interest-earning assets from

continuing operations for the year ended December 31, 2011, compared to 74 percent for the year ended

December 31, 2010. Lending at Regions is generally organized along three portfolio segments: commercial

(including commercial and industrial, and owner occupied commercial real estate mortgage and construction

loans), investor real estate loans (commercial real estate mortgage and construction loans) and consumer loans

(residential first mortgage, home equity, indirect, consumer credit card and other consumer loans).

Regions manages loan growth with a focus on risk management and risk-adjusted return on capital.

Strategic decisions to reduce the concentration in investor real estate, sales of residential mortgage loans, and

lower demand for home equity products were the primary contributors to the decrease. The decrease was partially

offset by increases in commercial and industrial loans and indirect automobile lending as well as the purchase of

Regions-branded credit card loans during the second quarter of 2011.

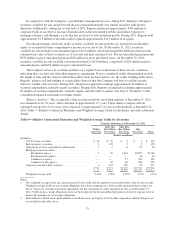

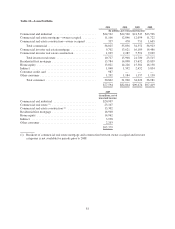

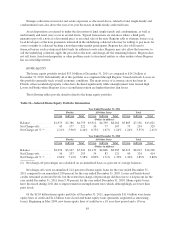

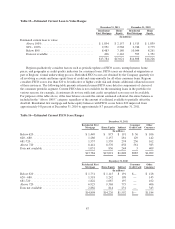

Table 10 illustrates a year-over-year comparison of loans by portfolio segment and class and Table 11

provides information on selected loan maturities.

80