Regions Bank 2011 Annual Report Download - page 182

Download and view the complete annual report

Please find page 182 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

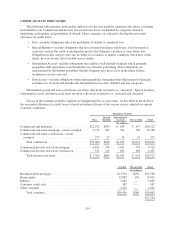

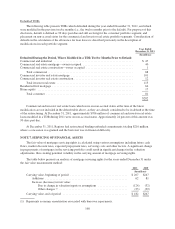

An analysis of the allowance for credit losses in the aggregate for the years ended December 31, 2010 and

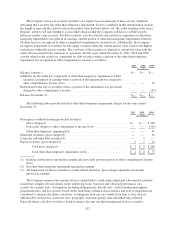

2009 follows:

2010 2009

(In millions)

Allowance for loan losses at beginning of year ..................................... $3,114 $ 1,826

Provision for loan losses ....................................................... 2,863 3,541

Loan losses:

Charge-offs ......................................................... (2,912) (2,369)

Recoveries ......................................................... 120 116

Net loan losses ...................................................... (2,792) (2,253)

Allowance for loan losses at end of year .......................................... $3,185 $ 3,114

Reserve for unfunded credit commitments at beginning of year ........................ $ 74 $ 74

Provision for unfunded credit commitments ................................... (3) —

Reserve for unfunded credit commitments at end of year ............................. 71 74

Allowance for credit losses at end of year ......................................... $3,256 $ 3,188

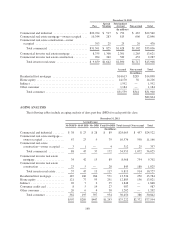

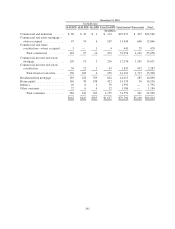

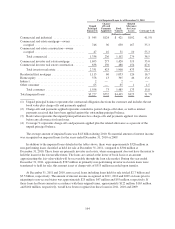

PORTFOLIO SEGMENT RISK FACTORS

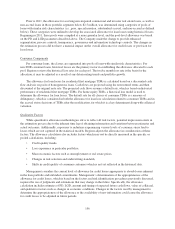

The following describe the risk characteristics relevant to each of the portfolio segments.

Commercial—The commercial loan portfolio segment includes commercial and industrial loans to

commercial customers for use in normal business operations to finance working capital needs, equipment

purchases or other expansion projects. Commercial also includes owner-occupied commercial real estate loans to

operating businesses, which are loans for long-term financing of land and buildings, and are repaid by cash flow

generated by business operations. Owner-occupied construction loans are made to commercial businesses for the

development of land or construction of a building where the repayment is derived from revenues generated from

the business of the borrower. Collection risk in this portfolio is driven by the creditworthiness of underlying

borrowers, particularly cash flow from customers’ business operations.

Investor Real Estate—Loans for real estate development are repaid through cash flow related to the

operation, sale or refinance of the property. This portfolio segment includes extensions of credit to real estate

developers or investors where repayment is dependent on the sale of real estate or income generated from the real

estate collateral. A portion of Regions’ investor real estate portfolio segment is comprised of loans secured by

residential product types (land, single-family and condominium loans) within Regions’ markets. Additionally,

these loans are made to finance income-producing properties such as apartment buildings, office and industrial

buildings, and retail shopping centers. Loans in this portfolio segment are particularly sensitive to valuation of

real estate.

Consumer—The consumer loan portfolio segment includes residential first mortgage, home equity, indirect,

consumer credit card, and other consumer loans. Residential first mortgage loans represent loans to consumers to

finance a residence. These loans are typically financed over a 15 to 30 year term and, in most cases, are extended

to borrowers to finance their primary residence. Home equity lending includes both home equity loans and lines

of credit. This type of lending, which is secured by a first or second mortgage on the borrower’s residence,

allows customers to borrow against the equity in their home. Real estate market values as of the time the loan or

line is secured directly affect the amount of credit extended and, in addition, changes in these values impact the

depth of potential losses. Indirect lending, which is lending initiated through third-party business partners, is

largely comprised of loans made through automotive dealerships. Consumer credit card includes approximately

500,000 Regions branded consumer credit card accounts purchased during 2011 from FIA Card Services. Other

consumer loans include direct consumer installment loans and overdrafts. Loans in this portfolio segment are

sensitive to unemployment and other key consumer economic measures.

158