Regions Bank 2011 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

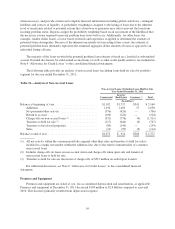

OFF-BALANCE SHEET ARRANGEMENTS

Regions has certain variable interests in unconsolidated variable interest entities (i.e., Regions is not the

primary beneficiary). Regions owns the common stock of subsidiary business trusts, which have issued

mandatorily redeemable preferred capital securities (“trust preferred securities”) in the aggregate of $1 billion at

the time of issuance. These trusts meet the definition of a variable interest entity of which Regions is not the

primary beneficiary; the trusts’ only assets are junior subordinated debentures issued by Regions, which were

acquired by the trusts using the proceeds from the issuance of the trust preferred securities and common stock.

The junior subordinated debentures are included in long-term borrowings (see Note 12 “Long-Term Borrowings”

to the consolidated financial statements), and Regions’ equity interests in the business trusts are included in other

assets. For regulatory reporting and capital adequacy purposes, the Federal Reserve Board has indicated that such

trust preferred securities currently constitute Tier 1 capital, but beginning in 2013, trust preferred securities will

be phased out as an allowable component of Tier 1 capital over a three-year period. Additional discussion

regarding the status of capital treatment for these instruments is included in the “Supervision and Regulation—

Capital Requirements” section of Item 1 of this Annual Report on Form 10-K.

Also, Regions periodically invests in various limited partnerships that sponsor affordable housing projects,

which are funded through a combination of debt and equity. Regions’ maximum exposure to loss as of

December 31, 2011 was $873 million, which included $184 million in unfunded commitments to the

partnerships. Additionally, Regions has short-term construction loans or letters of credit commitments with the

partnerships totaling $180 million as of December 31, 2011. The funded portion of these loans and letters of

credit was $59 million at December 31, 2011. The funded portion is included with loans on the consolidated

balance sheets. See Note 2 “Variable Interest Entities” to the consolidated financial statements for further

discussion.

EFFECTS OF INFLATION

The majority of assets and liabilities of a financial institution are monetary in nature; therefore, a financial

institution differs greatly from most commercial and industrial companies, which have significant investments in

fixed assets or inventories that are greatly impacted by inflation. However, inflation does have an important

impact on the growth of total assets in the banking industry and the resulting need to increase equity capital at

higher than normal rates in order to maintain an appropriate equity-to-assets ratio. Inflation also affects other

expenses that tend to rise during periods of general inflation.

Management believes the most significant potential impact of inflation on financial results is a direct result

of Regions’ ability to manage the impact of changes in interest rates. Management attempts to maintain an

essentially balanced position between rate-sensitive assets and liabilities in order to minimize the impact of

interest rate fluctuations on net interest income. However, this goal can be difficult to completely achieve in

times of rapidly changing rate structure and is one of many factors considered in determining the Company’s

interest rate positioning. The Company is asset sensitive as of December 31, 2011. Refer to Table 28 “Interest

Rate Sensitivity” for additional details on Regions’ interest rate sensitivity.

EFFECTS OF DEFLATION

A period of deflation would affect all industries, including financial institutions. Potentially, deflation could

lead to lower profits, higher unemployment, lower production and deterioration in overall economic conditions.

In addition, deflation could depress economic activity and impair bank earnings through increasing the value of

debt while decreasing the value of collateral for loans. If the economy experienced a severe period of deflation,

then it could depress loan demand, impair the ability of borrowers to repay loans and sharply reduce bank

earnings.

105