Regions Bank 2011 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

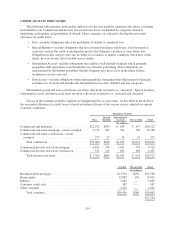

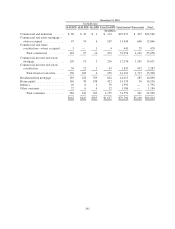

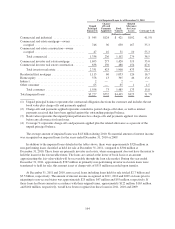

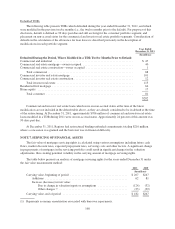

TROUBLED DEBT RESTRUCTURINGS (TDRs)

Clarified Accounting Literature

In January 2011, the FASB issued accounting guidance temporarily deferring the effective date for public-

entity creditors to provide new disclosures, which were addressed in previously issued guidance regarding

receivables, for TDRs. The deferred effective date coincided with the effective date for clarified guidance about

what constitutes a TDR for creditors, which was issued in April 2011 by the FASB. Regions applied the clarified

definition beginning with third quarter financial reporting to all loans modified after January 1, 2011.

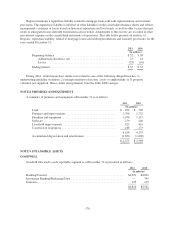

For consumer loans, as described below, Regions already considered loans modified under the Customer

Assistance Program (“CAP”) to be TDRs. Under the CAP, Regions may offer a short-term deferral, a term

extension, an interest rate reduction, a new loan product, or a combination of these options. Because such

modifications clearly are concessionary in nature, and because the customer documents a hardship in order to

participate in the program, Regions concluded that these loans met the TDR definition before the clarified

guidance was issued. Accordingly, the guidance did not have a material impact on TDR balances for the

consumer portfolio segment.

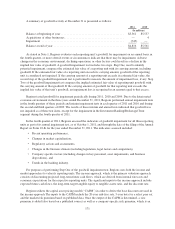

For Regions, the focus of the evaluation of the clarified TDR definition was on workout accommodations,

such as renewals and forbearances, for criticized and classified commercial and investor real estate loans.

Regions’ business strategy to keep loan maturities short, particularly in the investor real estate portfolio segment,

in order to maintain leverage in negotiating with customers drove the renewal activity. Regions often increases or

at least maintains the same interest rate, and often receives consideration in exchange for such modifications

(e.g., principal paydowns, additional collateral, or additional guarantor support). Therefore, under pre-existing

accounting guidance, such modifications were not considered by Regions to be concessionary and were not

considered TDRs. However, the new clarification places more emphasis on whether the terms of the modified

loan are at a market rate in order to determine if a concession has been made. Under the clarified guidance, a

modification is refutably considered by Regions to be a concession if the borrower could not access similar

financing at market terms, even if Regions concludes that the borrower will ultimately pay all contractual

amounts owed. Therefore, the amount of accruing TDRs increased as a result of the new clarification. As noted

above, the original maturities of the notes being modified are relatively short (for example 2-3 years), and the

renewed term is typically comparable to the original maturity. Accordingly, Regions considers these

modifications to be significant delays in payment. Therefore, extensions must be considered for the TDR

determination because the renewed term is significant to the term of the original note.

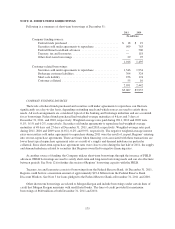

As a result of the TDR designation, all loans modified in a TDR are considered to be impaired, even if they

carry an accruing risk rating. Beginning in the third quarter of 2011, for accruing commercial and investor real

estate TDRs (as well as for non-accrual commercial and investor real estate loans less than $2.5 million),

Regions based the allowance for loan losses on a discounted cash flow analysis performed at the note level,

where projected cash flows reflect credit losses based on statistical information derived from loans with similar

risk characteristics (e.g., risk rating and product type). For all commercial and investor real estate non-accrual

loans equal to or greater than $2.5 million, consistent with historical practice, the allowance for loan losses is

based on a specific evaluation, considering the facts and circumstances specific to each obligation. Because

Regions’ past practice was to base the allowance for loan losses for commercial and investor real estate loans on

loss content based on risk rating and product type, either through specific evaluation of larger loans, or groups of

smaller loans with similar risk characteristics, the adoption of the clarification and the corresponding increase in

commercial and investor real estate TDRs did not materially impact the overall level of the allowance for loan

losses. As noted above, the clarification did not impact the level of TDRs in the consumer portfolio segment or

the related allowance for loan losses.

Modification Activity: Commercial and Investor Real Estate Portfolio Segments

Regions regularly modifies commercial and investor real estate loans in order to facilitate a workout strategy.

Typical modifications include workout accommodations, such as renewals and forbearances. The discussion under

165