Regions Bank 2011 Annual Report Download - page 131

Download and view the complete annual report

Please find page 131 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

expectations of balance sheet growth and composition, the pricing and maturity characteristics of existing

business and the characteristics of future business. Interest rate-related risks are expressly considered, such as

pricing spreads, the lag time in pricing deposit accounts, prepayments and other option risks. Regions considers

these factors, as well as the degree of certainty or uncertainty surrounding their future behavior.

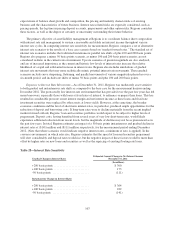

The primary objective of asset/liability management at Regions is to coordinate balance sheet composition

with interest rate risk management to sustain a reasonable and stable net interest income throughout various

interest rate cycles. In computing interest rate sensitivity for measurement, Regions compares a set of alternative

interest rate scenarios to the results of a base case scenario based on “market forward rates.” The standard set of

interest rate scenarios includes the traditional instantaneous parallel rate shifts of plus 100 and 200 basis points.

Regions also prepares a minus 50 basis points scenario, as minus 100 and 200 basis point scenarios are not

considered realistic in the current rate environment. Up-rate scenarios of greater magnitude are also analyzed,

and are of increased importance as the current and historic low levels of interest rates increase the relative

likelihood of a rapid and substantial increase in interest rates. Regions also includes simulations of gradual

interest rate movements that may more realistically mimic potential interest rate movements. These gradual

scenarios include curve steepening, flattening, and parallel movements of various magnitudes phased in over a

six-month period, and include rate shifts of minus 50 basis points and plus 100 and 200 basis points.

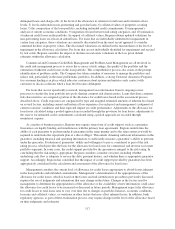

Exposure to Interest Rate Movements—As of December 31, 2011, Regions was moderately asset sensitive

to both gradual and instantaneous rate shifts as compared to the base case for the measurement horizon ending

December 2012. The protractedly low interest-rate environment that has prevailed over the past few years has led

many borrowers, especially those with loans at fixed rates of interest, to refinance or prepay their loans. This has

resulted in considerable pressure on net interest margin and net interest income as these loans and fixed rate

investment securities were replaced by other assets at lower yields. However, at the same time, the broader

economic conditions and the level of short-term interest-rates, in particular, produced ample opportunities for the

reduction of deposit and borrowing costs. If long-term rates were to decline materially from the recent implied

market-forward outlook, Regions’ loan and securities portfolios would expect to be subject to higher levels of

prepayment. Deposit costs, having benefited from several years of very low short-term rates, would likely

experience additional reduction from recent levels, but the magnitude of decline may not be as pronounced as in

the past few years. In total, Regions estimates an impact of a 50 basis points instantaneous and gradual decline in

interest rates at ($141) million and ($111) million respectively, for the measurement period ending December

2012. (Note that where scenarios would indicate negative interest rates, a minimum of zero is applied). In the

converse environment, in which rates rise, Regions estimates that the speed of loan and securities prepayment

will slow considerably and deposit rates would rise, but the negative impact of these factors would be more than

offset by higher rates on new loans and securities as well as the repricing of existing floating rate loans.

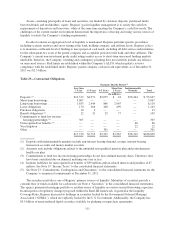

Table 28—Interest Rate Sensitivity

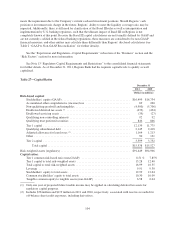

Gradual Change in Interest Rates

Estimated Annual Change in Net Interest Income

December 31, 2011

(In millions)

+200 basis points ........................ $300

+100 basis points ........................ 173

-50 basis points ......................... (111)

Instantaneous Change in Interest Rates

+200 basis points ........................ $364

+100 basis points ........................ 222

-50 basis points ......................... (141)

107