Regions Bank 2011 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

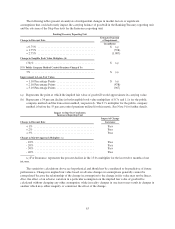

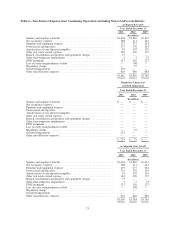

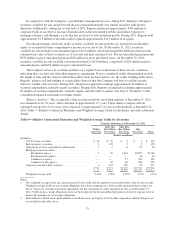

Table 5—Non-Interest Income from Continuing Operations

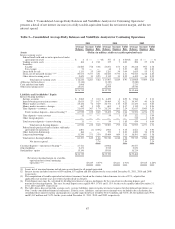

Year Ended December 31

2011 2010 2009

(In millions)

Service charges on deposit accounts ....................................... $1,168 $1,174 $1,156

Capital markets and investment income .................................... 64 69 39

Mortgage income ...................................................... 220 247 259

Trust department income ................................................ 199 196 191

Securities gains, net .................................................... 112 394 69

Insurance commissions and fees .......................................... 106 104 105

Leveraged lease termination gains ......................................... 8 78 587

Commercial credit fee income ............................................ 80 76 70

Bank-owned life insurance ............................................... 83 88 74

Net revenue (loss) from affordable housing .................................. (69) (72) (53)

Visa-related gains ...................................................... — — 80

Other miscellaneous income ............................................. 172 135 188

$2,143 $2,489 $2,765

Service Charges on Deposit Accounts

Income from service charges on deposit accounts decreased less than 1 percent in 2011 and totaled $1.2

billion in both 2011 and 2010. This modest decrease was driven by policy changes related to Regulation E, as

well as a decline in interchange income as a result of debit interchange price controls implemented in the fourth

quarter of 2011. These factors were offset by the restructuring of checking accounts from free to fee-eligible and

a higher level of customer transactions.

Interchange income, which is included in service charges on deposit accounts, was impacted by the Federal

Reserve’s rulemaking required by section 1075 of the Dodd-Frank Act. The Federal Reserve Board of Governors

announced its final rule on debit card interchange fees mandated by the Durbin Amendment to the Dodd-Frank

Act effective October 1, 2011. The final proposal included an allowable interchange fee of 21 cents per

transaction plus a 5 basis points allowance for fraud mitigation expenses, which was higher than the original

proposal, but below the 44 cents per transaction which was the average amount charged for debit transactions

according to the Federal Reserve’s study on interchange transactions. Total revenues from debit card income at

Regions were $335 million in 2011, which included one full quarter under the final rules. Based on the final

ruling, the Company estimates that the reduction to annual debit interchange revenue will be approximately $180

million before any mitigation efforts. However, the Company believes it will be able to mitigate this impact over

time through fee changes, introduction of new products and services and expense management.

Capital Markets, Investment and Trust Department Income

Total capital markets and investment income decreased 7 percent to $64 million in 2011 from $69 million in

2010. Trust department income increased 2 percent to $199 million in 2011, driven by a higher amount of fees

from commissions. Trust assets under management were approximately $76.1 billion at year-end 2011 compared

to approximately $76.6 billion at year-end 2010.

Mortgage Income

Mortgage income is generated through the origination and servicing of mortgage loans for long-term

investors and sales of mortgage loans in the secondary market. Mortgage income decreased $27 million or 11

percent to $220 million in 2011. The decrease was primarily driven by lower benefit from mortgage servicing

70