Regions Bank 2011 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

REGIONS 2011 ANNUAL REPORT6

Importantly, this transaction reduces our over-

all risk profi le, enhances liquidity and improves

Regions’ capital ratios while reducing our ex-

pense base and enhancing our focus on our core

banking business. Because we retained our asset

management and trust businesses, we remain

well positioned to continue serving the wealth

management needs of our customers. This trans-

action establishes an on-going relationship with

Raymond James, further enhancing our ability

to serve our existing customers. We also ex-

pect that we will maintain important business

relationships with Morgan Keegan associates

that were developed over many years of working

together to serve our customers’ needs.

This transaction, along with achieving continued,

sustainable profi tability and demonstrating a

material improvement in our credit quality, are

all key steps toward the eventual repayment of

the government’s investment in Regions. We

believe we have made tremendous progress in

these regards, but we remain prudent and want

to pay back the government’s investment from a

place of strength and in as shareholder-friendly

manner as possible.

Margin Improvement. This prolonged environ-

ment of low interest rates that we are currently

operating in has continued to put strains on net

interest income and the resulting net interest

margin. While we have been able to generate

low cost deposit growth and thus reduce deposit

costs to 49 basis points, low loan demand has

put stress on our loan yield. Net interest income

for the year was $3.4 billion, or 0.6% higher

than 2010. However, net interest margin for the

full year was 3.07%, a 16 basis point improve-

ment from the previous year.

We continue to forecast that interest rates will

remain low through 2012 and barring any un-

expected movement in interest rates, we ex-

pect net interest margin to grow modestly over

the balance of 2012, primarily due to high

yielding CD maturities.

Growing Non-Interest Revenue in a Challeng-

ing Environment. Non-interest revenue, which

is primarily made up of service charges and

interchange fees, was a particular focus in

2011. With the new restrictions recently im-

posed, the ability to grow fee-based revenues

has proven to be a critical aspect of our strat-

egy. New products and services not only allow

us to meet evolving customer needs, but also to

diversify and grow dependable revenue streams.

Our service charges remained steady in 2011,

while most of our industry saw declines. Contrib-

uting to this was our restructuring of checking

accounts to fee-eligible, which was a necessity

to offset lower interchange income. While we

have seen an increase in the volume of transac-

tions due to the number of new accounts that we

opened, total spending among consumers has

decreased due to the sluggish economy. In ad-

dition, over the last two years we have seen our

second and third best years in mortgage income

and production.

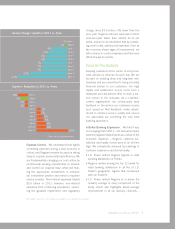

2008

2009

2010

2011

3.23 %

2.68%

2.91%

3.07%

Net Interest Margin*

*From continuing operations