Regions Bank 2011 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

such, the contract amounts do not necessarily represent future cash requirements. Settlement of the transactions

relating to such commitments is not expected to have a material effect on Regions’ consolidated financial

position. Transactions involving future settlement give rise to market risk, which represents the potential gain or

loss that can be caused by a change in the market value of a particular financial instrument. Regions’ exposure to

market risk is determined by a number of factors, including the size, composition and diversification of positions

held, the absolute and relative levels of interest rates, and market volatility.

Additionally, in the normal course of business, Morgan Keegan enters into transactions for delayed delivery,

to-be-announced securities, which are recorded in trading account assets on the consolidated balance sheets at

fair value. Risks arise from the possible inability of counterparties to meet the terms of their contracts and from

unfavorable changes in interest rates or the market values of the securities underlying the instruments. The credit

risk associated with these contracts is typically limited to the cost of replacing all contracts on which Morgan

Keegan has recorded an unrealized gain. For exchange-traded contracts, the clearing organization acts as the

counterparty to specific transactions and, therefore, bears the risk of delivery to and from counterparties.

Interest rate risk at Morgan Keegan arises from the exposure of holding interest-sensitive financial instruments

such as government, corporate and municipal bonds, and certain preferred equities. Morgan Keegan manages its

exposure to interest rate risk by setting and monitoring limits and, where feasible, entering into offsetting positions

in securities with similar interest rate risk characteristics. Securities inventories recorded in trading account assets

on the consolidated balance sheet, are marked to market, and, accordingly, there are no unrecorded gains or losses in

value. While a significant portion of the securities inventories have contractual maturities in excess of five years,

these inventories, on average, turn over in excess of twelve times per year. Accordingly, the exposure to interest rate

risk inherent in Morgan Keegan’s securities inventories is less than that of similar financial instruments held by

firms in other industries. Morgan Keegan’s equity securities inventories are exposed to risk of loss in the event of

unfavorable price movements. Also, Morgan Keegan is subject to credit risk arising from non-performance by

trading counterparties, customers and issuers of debt securities owned. This risk is managed by imposing and

monitoring position limits, monitoring trading counterparties, reviewing security concentrations, holding and

marking to market collateral, and conducting business through clearing organizations that guarantee performance.

Morgan Keegan regularly participates in the trading of some derivative securities for its customers; however, this

activity does not involve Morgan Keegan acquiring a position or commitment in these products and this trading is

not a significant portion of Morgan Keegan’s business.

Morgan Keegan has been an underwriter and dealer in auction rate securities. See Note 23 “Commitments,

Contingencies and Guarantees” to the consolidated financial statements for more details regarding regulatory

action related to Morgan Keegan auction rate securities. As of December 31, 2011, customers of Morgan Keegan

owned approximately $675 thousand of auction rate securities, and Morgan Keegan held approximately $135

million of auction rate securities on the balance sheet.

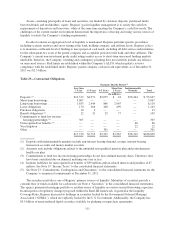

To manage trading risks arising from interest rate and equity price risks, Regions uses a Value at Risk

(“VAR”) model along with other risk management methods to measure the potential fair value the Company

could lose on its trading positions given a specified statistical confidence level and time-to-liquidate time

horizon. The end-of-period VAR was approximately $423 thousand at December 31, 2011 and $805 thousand at

December 31, 2010. Maximum daily VAR utilization during 2011 was $1.7 million and average daily VAR

during the same period was $782 thousand.

LIQUIDITY RISK

Liquidity is an important factor in the financial condition of Regions and affects Regions’ ability to meet the

borrowing needs and deposit withdrawal requirements of its customers. Regions intends to fund obligations

primarily through cash generated from normal operations. In addition to these obligations, Regions has

obligations related to potential litigation contingencies. See Note 23 “Commitments, Contingencies and

Guarantees” to the consolidated financial statements for additional discussion of the Company’s funding

requirements.

110