Regions Bank 2011 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

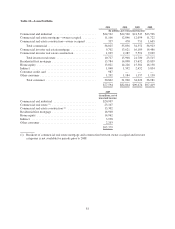

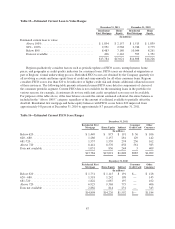

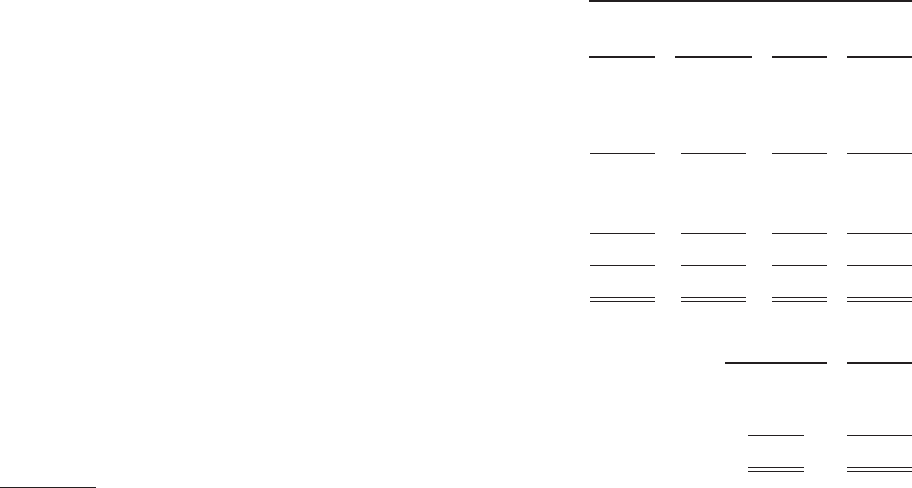

Table 11—Selected Loan Maturities

Loans Maturing as of December 31, 2011 (2)

Within

One Year

After One

But Within

Five Years

After

Five

Years Total

(In millions)

Commercial and industrial (1) ................................. $ 5,511 $14,613 $4,269 $24,393

Commercial real estate mortgage—owner-occupied ............... 1,965 5,913 3,288 11,166

Commercial real estate construction—owner-occupied ............. 39 126 172 337

Total commercial ...................................... 7,515 20,652 7,729 35,896

Commercial investor real estate mortgage ....................... 4,811 4,253 638 9,702

Commercial investor real estate construction ..................... 605 396 24 1,025

Total investor real estate ................................. 5,416 4,649 662 10,727

$12,931 $25,301 $8,391 $46,623

Predetermined

Rate

Variable

Rate

(In millions)

Due after one year but within five years ...................................... $5,894 $19,407

Due after five years ...................................................... 4,087 4,304

$9,981 $23,711

(1) Excludes $129 million of small business credit card accounts.

(2) Table 11 excludes residential first mortgage, home equity, indirect and other consumer loans.

The following sections describe the composition of the portfolio segments and classes in Table 10 and

explain variations in balances from the 2010 year-end. See Note 5 “Loans” and Note 6 “Allowance for Credit

Losses” to the consolidated financial statements for additional discussion.

Commercial—The commercial portfolio segment includes commercial and industrial loans to commercial

customers for use in normal business operations to finance working capital needs, equipment purchases and other

expansion projects. Commercial also includes owner-occupied commercial real estate loans to operating

businesses, which are loans for long-term financing of land and buildings, and are repaid by cash flow generated

by business operations. Owner-occupied construction loans are made to commercial businesses for the

development of land or construction of a building where the repayment is derived from revenues generated from

the business of the borrower. During 2011, total commercial loan balances increased $969 million, or 3 percent,

driven by growth experienced in specialized industry groups.

Investor Real Estate—Loans for real estate development are repaid through cash flow related to the

operation, sale or refinance of the property. This portfolio segment includes extensions of credit to real estate

developers or investors where repayment is dependent on the sale of real estate or income generated from the real

estate collateral. A portion of Regions’ investor real estate portfolio segment is comprised of loans secured by

residential product types (land, single-family and condominium loans) within Regions’ markets. Additionally,

this category includes loans made to finance income-producing properties such as apartment buildings, office and

industrial buildings, and retail shopping centers. The investor real estate loan segment decreased $5.2 billion

from 2010 balances primarily due to strategic decisions to reduce the concentration in investor real estate in

response to credit risk and economic pressure.

Residential First Mortgage—Residential first mortgage loans represent loans to consumers to finance a

residence. These loans are typically financed over a 15 to 30 year term and, in most cases, are extended to

borrowers to finance their primary residence. These loans experienced a $1.1 billion decline to $13.8 billion in

82