Regions Bank 2011 Annual Report Download - page 62

Download and view the complete annual report

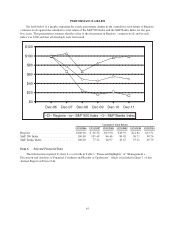

Please find page 62 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

the FDIC’s bank resolution model. The Secretary of the U.S. Treasury may trigger a liquidation under this

authority only after consultation with the President of the United States and after receiving a recommendation

from the boards of the FDIC and the Federal Reserve upon a two-thirds vote. Liquidation proceedings will be

funded by the Orderly Liquidation Fund, which will borrow from the U.S. Treasury and impose risk-based

assessments on covered financial companies. Risk-based assessments would be made, first, on entities that

received more in the resolution than they would have received in the liquidation to the extent of such excess, and

second, if necessary, on, among others, bank holding companies with total consolidated assets of $50 billion or

more, such as Regions. Any such assessments may adversely affect our business, financial condition or results of

operations.

Rules regulating the imposition of debit card income may adversely affect our operations.

The Dodd-Frank Act gave the Federal Reserve the authority to establish rules regarding interchange fees

charged by payment card issuers for transactions in which a person uses certain types of debit cards, requiring

that such fees be reasonable and proportional to the cost incurred by the issuer with respect to such transaction,

subject to a possible adjustment to account for costs incurred in connection with the issuer’s fraud prevention

policies. On June 29, 2011, the Federal Reserve approved its final rule on debit interchange fees. The final rule

caps the maximum debit interchange fee at 21 cents, plus 5 basis points (multiplied by the amount of the

transaction) to reflect a portion of fraud losses. The restrictions on interchange fees contained in the final rule are

applicable to all debit card issuers who, together with their affiliates, possess more than $10 billion in assets,

such as Regions Bank. The debit interchange fee provision took effect on October 1, 2011.

The Federal Reserve estimates that covered issuers, such as Regions Bank, may experience a decline in

debit interchange fee revenue by more than 40 percent under the final rule. In 2011, Regions Bank collected $335

million in debit card income. We estimate that our debit card income will likely be reduced by approximately

$180 million annually under the final rule before mitigation efforts.

In addition to the final rule on debit interchange fees, the Federal Reserve issued an interim final rule that

provides an upward adjustment of a maximum of 1 cent to an issuer’s debit card interchange fee if the issuer

establishes and implements procedures that meet specified fraud-prevention standards set forth under the interim

final rule. In order to receive the adjustment, qualifying issuers must certify their eligibility to the payment card

networks in which they participate. The fraud-prevention adjustment provision took effect on October 1, 2011,

but may be revised by the Federal Reserve at a later date based on comments received through September 30,

2011. Regions is currently eligible for this adjustment. Since this rule is not yet final, the effects of this provision

in its final form on our business, financial condition or results of operation are not yet known at this time.

The final rule also prohibits issuers and payment card networks from restricting the number of payment card

networks on which an electronic debit transaction may be processed to fewer than two unaffiliated networks,

regardless of the means by which a transaction may be authorized. This network exclusivity provision is

applicable to all issuers, even those exempt from the debit interchange fees. Issuers will be subject to the network

exclusivity rule beginning on April 1, 2012.

The Federal Reserve predicts that this network exclusivity provision may result in higher costs for some

issuers and may place downward pressure on interchange fees because merchants may opt to route transactions

over less expensive networks. The effects of this rule on our business, financial condition or results of operation

are not yet known at this time.

Risks Related to the Sale of Morgan Keegan

The sale of Morgan Keegan may have an adverse impact on our business.

Pursuant to a stock purchase agreement entered into on January 11, 2012 (the “Stock Purchase Agreement”),

Regions agreed to sell Morgan Keegan and certain related companies to Raymond James Financial, Inc. for

38