Regions Bank 2011 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

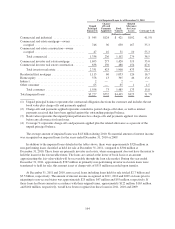

Prior to 2011, the allowance for accruing non-impaired commercial and investor real estate loans, as well as

non-accrual loans in those portfolio segments below $2.5 million, was determined using categories of pools of

loans with similar risk characteristics (i.e., pass, special mention, substandard accrual, and non-accrual as defined

below). These categories were utilized to develop the associated allowance for loan losses using historical losses.

Beginning in 2011, these pools were compiled at a more granular level, and the pool-level allowance was based

on the PD and LGD parameters described above. The Company made the change to provide enhanced

segmentation, process controls, transparency, governance and information technology controls. The changes in

the estimation process did not have a material impact on the overall allowance for credit losses or provision for

loan losses.

Consumer Components

For consumer loans, the classes are segmented into pools of loans with similar risk characteristics. For

non-TDR consumer loans, historical losses are the primary factor in establishing the allowance allocated to each

pool. Regions reviews the historical loss rates for each pool. The twelve month loss rate is the basis for the

allocation; it may be adjusted as a result of any deteriorating trends and portfolio growth.

The allowance for loan losses for residential first mortgage TDRs is calculated based on a discounted cash

flow analysis on pools of homogeneous loans. Cash flows are projected using the restructured terms and then

discounted at the original note rate. The projected cash flows assume a default rate, which is based on historical

performance of residential first mortgage TDRs. For home equity TDRs, a historical loss model is used to

determine the allowance for loan losses. The default rate for all classes of consumer TDRs is a measure of

delinquency, which is considered in both the allowance for loan loss calculation related to consumer TDRs and in

the accrual status decisions of TDRs after the modification, for which it is a key determinant along with collateral

valuation.

Qualitative Factors

While quantitative allowance methodologies strive to reflect all risk factors, potential imprecision exists in

the estimation process due to the inherent time lag of obtaining information and variations between estimates and

actual outcomes. Additionally, exposures to industries experiencing various levels of economic stress lead to

losses which are not captured in the statistical models. Regions adjusts the allowance in consideration of these

factors. The allowance calculation also includes factors which may not be directly measured in the specific or

pooled calculations, including:

• Credit quality trends,

• Loss experience in particular portfolios,

• Macroeconomic factors such as unemployment or real estate prices,

• Changes in risk selection and underwriting standards,

• Shifts in credit quality of consumer customers which is not yet reflected in the historical data.

Management considers the current level of allowance for credit losses appropriate to absorb losses inherent

in the loan portfolio and unfunded commitments. Management’s determination of the appropriateness of the

allowance for credit losses, which is based on the factors and risk identification procedures previously discussed,

requires the use of judgments and estimations that may change in the future. Specifically, the allowance

calculation includes estimates of PD, LGD, amount and timing of expected future cash flows, value of collateral,

and qualitative factors such as changes in economic conditions. Changes in the factors used by management to

determine the appropriateness of the allowance or the availability of new information could cause the allowance

for credit losses to be adjusted in future periods.

156