Regions Bank 2011 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

REGIONS 2011 ANNUAL REPORT 5

recovery, which has been slower than we would

have liked, we do expect credit costs to con-

tinue their downward trend into 2012.

Loan Growth. Refl ecting both consumers’ and

business owners’ lack of confi dence in our na-

tion’s economic recovery, overall loan demand

remains weak. In the last fi ve years, consumer

home equity loan applications have declined

75%, while loan approvals have remained

steady. Businesses and consumers who are not

confi dent in the economic outlook simply will

not take on the risk of additional debt if they

can avoid it.

In spite of this environment, Regions extended

$60 billion in new credit in 2011 and $185 bil-

lion since 2009. Our loan production included

$51 billion of business loans, of which $15 bil-

lion were new commitments. Our consumer

loan production totaled $9 billion, a 16% de-

cline over 2010.

We also made the strategic decision to re-enter

the credit card business for consumers and

small businesses as part of our effort to further

diversify our revenue streams and better serve

our customers. In just six months, we increased

our account production by 5% and generated

$1.1 billion in outstanding loans on the balance

sheet and an additional $6.7 billion in available

credit for our customers. In addition, consistent

with our strategy of expanding our loan product

offerings to meet consumer demand and mar-

ket conditions, we also re-entered the indirect

auto lending business, which generated $1 bil-

lion in volume for the year. This was one of the

primary drivers of total consumer loan volume,

which increased 36% in 2011.

Capital and Liquidity Strength. Regions’ capi-

tal levels – a key measure of a bank’s fi nancial

strength – are strong, and we are confi dent they

will remain so even as tougher capital stan-

dards are imposed. Clearly, the de-risking of

our portfolio over the last three years has paid

tremendous dividends in terms of enhancing

our portfolio.

At December 31, 2011, our capital levels also

exceeded Basel III requirements, with a Tier 1

ratio standing at 11.4% and a Tier 1 common1

ratio totaling 7.7%. Since the end of 2010,

our Tier 1 common1 capital increased 66 basis

points to end the year at 8.5%. Liquidity at both

the bank and the holding company remains

solid. We are primarily core funded and have

a loan to deposit ratio of 81%. Cash at the par-

ent holding company totaled $2.5 billion and

is above our policy minimums of maintaining

a suffi cient level of funding to meet projected

cash needs, which include all debt service,

dividends and maturities for the next two years.

As part of our process to evaluate how to best

manage our capital and increase shareholder

value, in January of this year we announced that

we entered into a stock purchase agreement

to sell Morgan Keegan & Company, Inc. and

related affi liates to Raymond James Financial

Inc., for $930 million. As part of the transaction,

Morgan Keegan is expected to pay Regions a

dividend of $250 million before closing, pending

regulatory approval, resulting in total proceeds

of approximately $1.18 billion to Regions.

Businesses and consumers who are not confi dent

in the economic outlook simply will not take on the

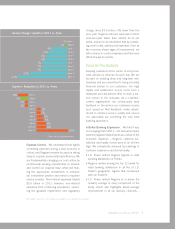

risk of additional debt if they can avoid it. Tier 1 Common1 Ratio

6.57 %

7. 1 5 %

7.85 %

8.51%

2008

2009

2010

2011

1 Non-GAAP, see Form 10-K Table 2 for GAAP to non-GAAP reconciliation