Regions Bank 2011 Annual Report Download - page 179

Download and view the complete annual report

Please find page 179 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

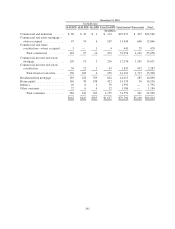

respectively, of home equity loans held by Regions were pledged to secure borrowings from the FHLB (see Note

12 for further discussion). At December 31, 2011, approximately $9.0 billion of commercial and industrial loans,

$9.7 billion of owner-occupied commercial real estate and investor real estate loans and $709 million of other

consumer loans held by Regions were pledged to the Federal Reserve Bank. At December 31, 2010,

approximately $9.8 billion of commercial and industrial loans, $15.9 billion of owner-occupied commercial real

estate and investor real estate loans and $1.1 billion of other consumer loans held by Regions were pledged to the

Federal Reserve Bank.

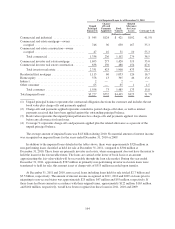

Directors and executive officers of Regions and its principal subsidiaries, including the directors’ and

officers’ families and affiliated companies, are loan and deposit customers and have other transactions with

Regions in the ordinary course of business. Total loans to these persons (excluding loans which in the aggregate

do not exceed $60,000 to any such person) at December 31, 2011 and 2010 were approximately $154 million and

$156 million, respectively. These loans were made in the ordinary course of business and on substantially the

same terms, including interest rates and collateral, as those prevailing at the same time for comparable

transactions with other persons and involve no unusual risk of collectability.

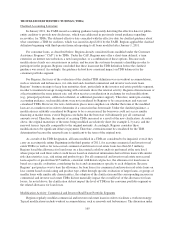

NOTE 6. ALLOWANCE FOR CREDIT LOSSES

The allowance for credit losses represents management’s estimate of credit losses inherent in the loan and

credit commitment portfolios as of year-end. The allowance for credit losses consists of two components: the

allowance for loan and lease losses and the reserve for unfunded credit commitments. Management’s assessment

of the appropriateness of the allowance for credit losses is based on a combination of both of these components.

Regions determines its allowance for credit losses in accordance with applicable accounting literature as well as

regulatory guidance related to receivables and contingencies. Binding unfunded credit commitments include

items such as letters of credit, financial guarantees and binding unfunded loan commitments.

CALCULATION OF ALLOWANCE FOR CREDIT LOSSES

Commercial and Investor Real Estate Components

Impaired Loans

For non-accrual commercial and investor real estate loans (including TDRs) equal to or greater than $2.5

million, the allowance for loan losses is based on specific evaluation considering the facts and circumstances

specific to each borrower. Beginning in the third quarter of 2011, for commercial and investor real estate

accruing TDRs and non-accruing TDRs less than $2.5 million, the allowance for loan losses is based on a

discounted cash flow analysis performed at the note level, where projected cash flows reflect credit losses based

on statistical information (including historical default information) derived from loans with similar risk

characteristics (e.g., credit quality indicator and product type) using probability of default (“PD”) and loss-given

default (“LGD”) as described in the following paragraph. Prior to this change, accruing TDRs equal to or greater

than $2.5 million were evaluated using the specific identification method, and all TDRs less than $2.5 million

were evaluated in the pooled methodology described below. This change in the estimation process did not have a

material impact to the overall level of the allowance for loan losses or the provision for loan losses.

Non-Impaired Loans

For all other commercial and investor real estate loans, the allowance for loan losses is calculated at a pool

level based on credit quality indicators and product type. A statistically determined PD and LGD are calculated.

Historical default information for similar loans is used as an input for the statistical model. Additionally, LGD

estimates for certain commercial and investor real estate properties are updated within the allowance calculation

quarterly using historical loss information that incorporates standard discount factors applied when those

properties are transferred into foreclosed properties. The standard discount factor is based on historical amounts

realized upon ultimate disposition of these properties. The pool level allowance is calculated using the PD and

LGD estimates.

155